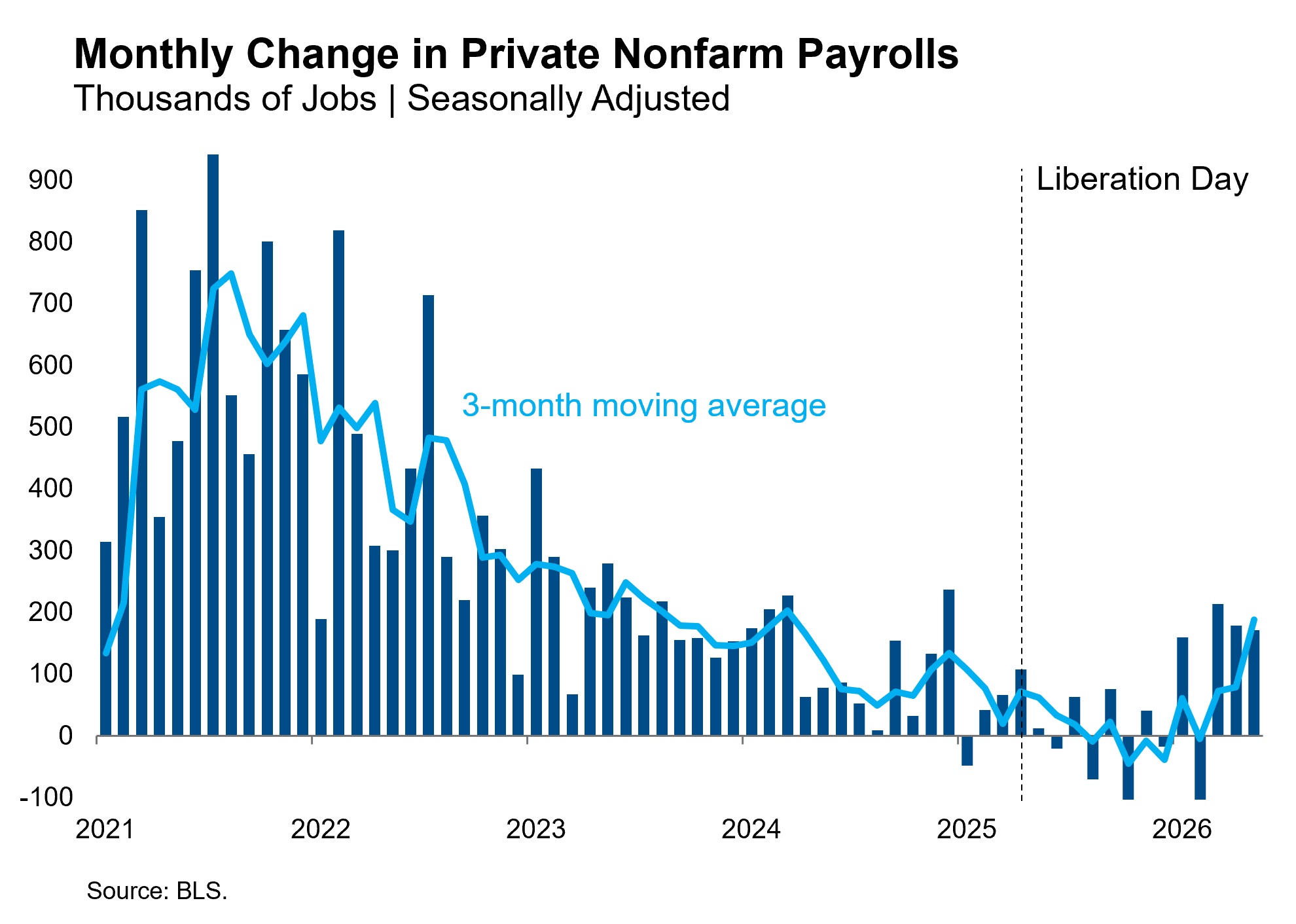

Nonfarm payroll employment surged by 172,000 in a blowout May jobs report, while the prior two months were revised higher by an additional 93,000. The only blemish is that breadth is still a bit narrow. Leisure and hospitality and local government accounted for 125,000 of the job creation in the month. That said, the 1-month diffusion index rose to 54.4% and has remained above 50% every month this year, indicating positive job creation in a majority of the 250 industries in the sample. The upward revisions to job creation (and, by extension, aggregate labor income) in prior months may prompt upward revisions to the low savings rates that have caused us some concern. The 3-month moving average of payroll growth rose to 188,000, which is starting to look like a breakout rather than a stabilization. Job creation appears to have bottomed in the middle of 2025 when trade policy uncertainty peaked.

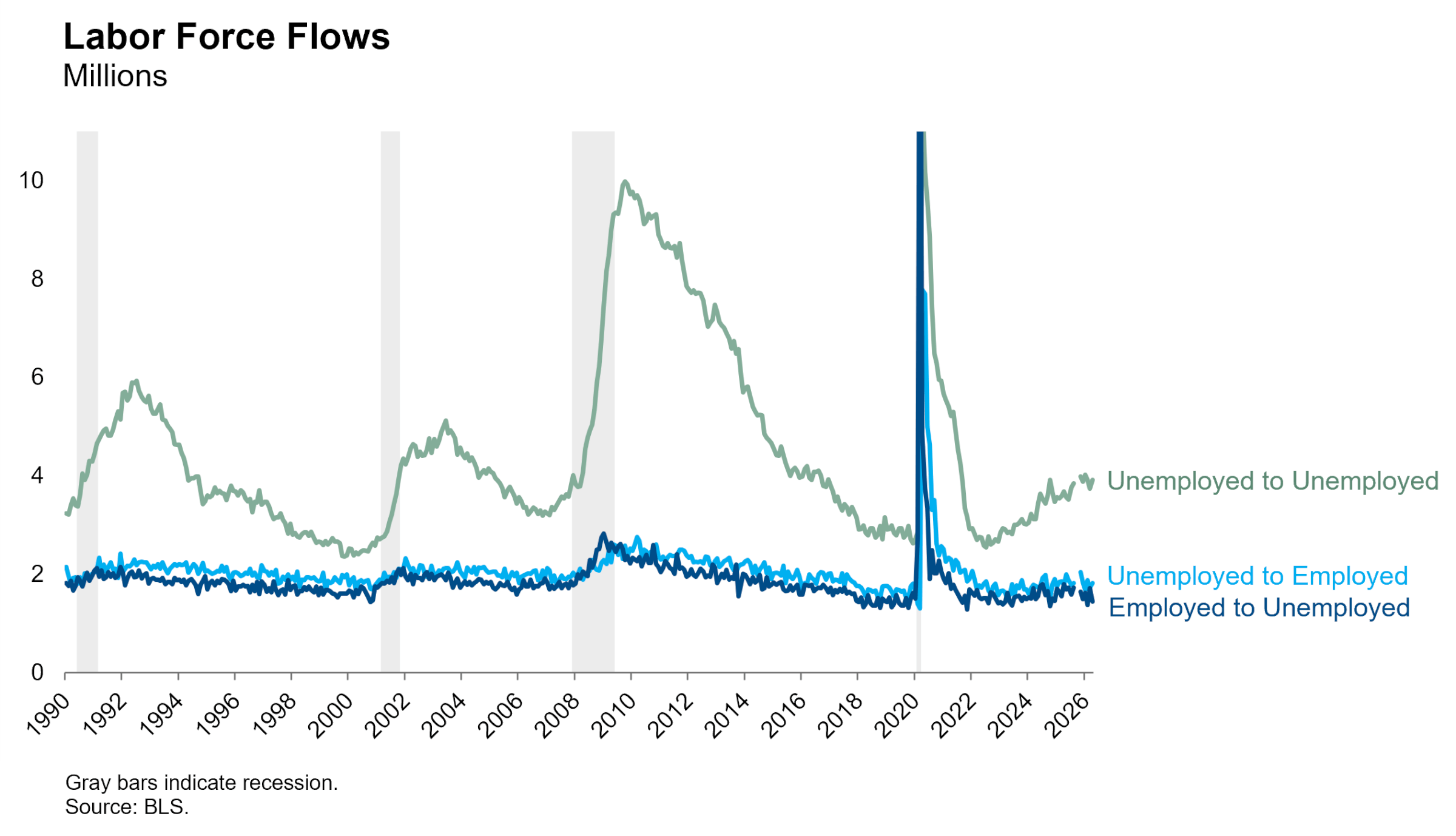

The household survey was also strong: employment in that survey increased by 149,000, the unemployment rate fell by almost half a percentage point to 4.296%, and the participation rate held steady. The number of unemployed persons declined, entirely due to a decline in the number of newly unemployed (<5 weeks). The number of unemployed for more than five weeks rose, so the duration of unemployment increased in the month. The labor force flows and JOLTS data suggest this is still a low-hire, low-fire labor market, but the balance is shifting slightly to allow for faster employment growth. Recall that the U.S. labor market exhibits significant churn underneath the relatively calm surface, with 2-5 million workers transitioning between employment, unemployment and labor force exit in a typical month. Small changes in the rates of these flows can easily translate to a few hundred thousand additional jobs.

Cuts Delayed Further

This report is clearly hawkish for the Fed. Short rate markets added half a hike to the 12-month monetary policy path after the release, now pricing one full hike by December and nearly two by June. We revise our modal expectation from three cuts in December, March and June to two cuts in January and April. Today’s report suggests little urgency to ease monetary policy and argues for a higher neutral rate. It does not, however, suggest a need to tighten policy. The unemployment rate has improved slightly in the last few months but remains nearly a full percentage point above its cycle low. Wage inflation remains well within bounds in this report and in the Employment Cost Index. The labor market is not overheating. We continue to believe that the willingness of some FOMC participants to publicly consider hikes is motivated by a desire to anchor inflation expectations. If the war ends and energy prices decline, that motivation will fade away.