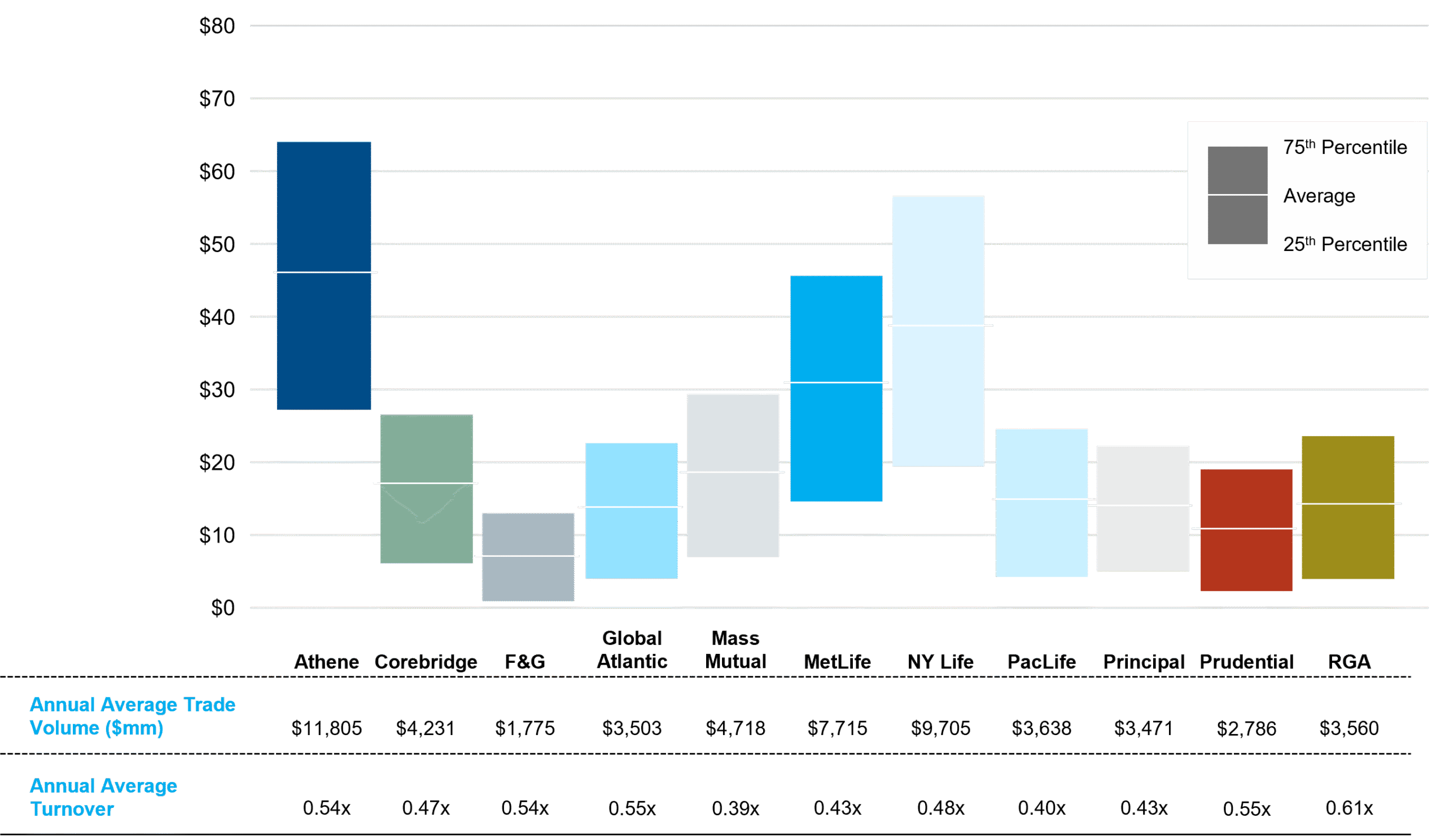

One limitation of using the market spreads of specific reference bonds is the episodic issuing patterns of each issuer. This can lead to differences in durations and maturity dates of the bonds in the analysis.

To provide a more robust measure of each issuer’s credit quality, the Average Issuer Spread dataset fits a spread curve to the entire universe of outstanding bonds for each issuer. Comparing the average issuer spread curve of PRT providers allows for a more like-for-like comparison across PRT providers by controlling for PRT variables such as maturity, issue date, dollar price, etc. The Average Issuer Spread ELB dataset re-calculates the ELB using this approach.

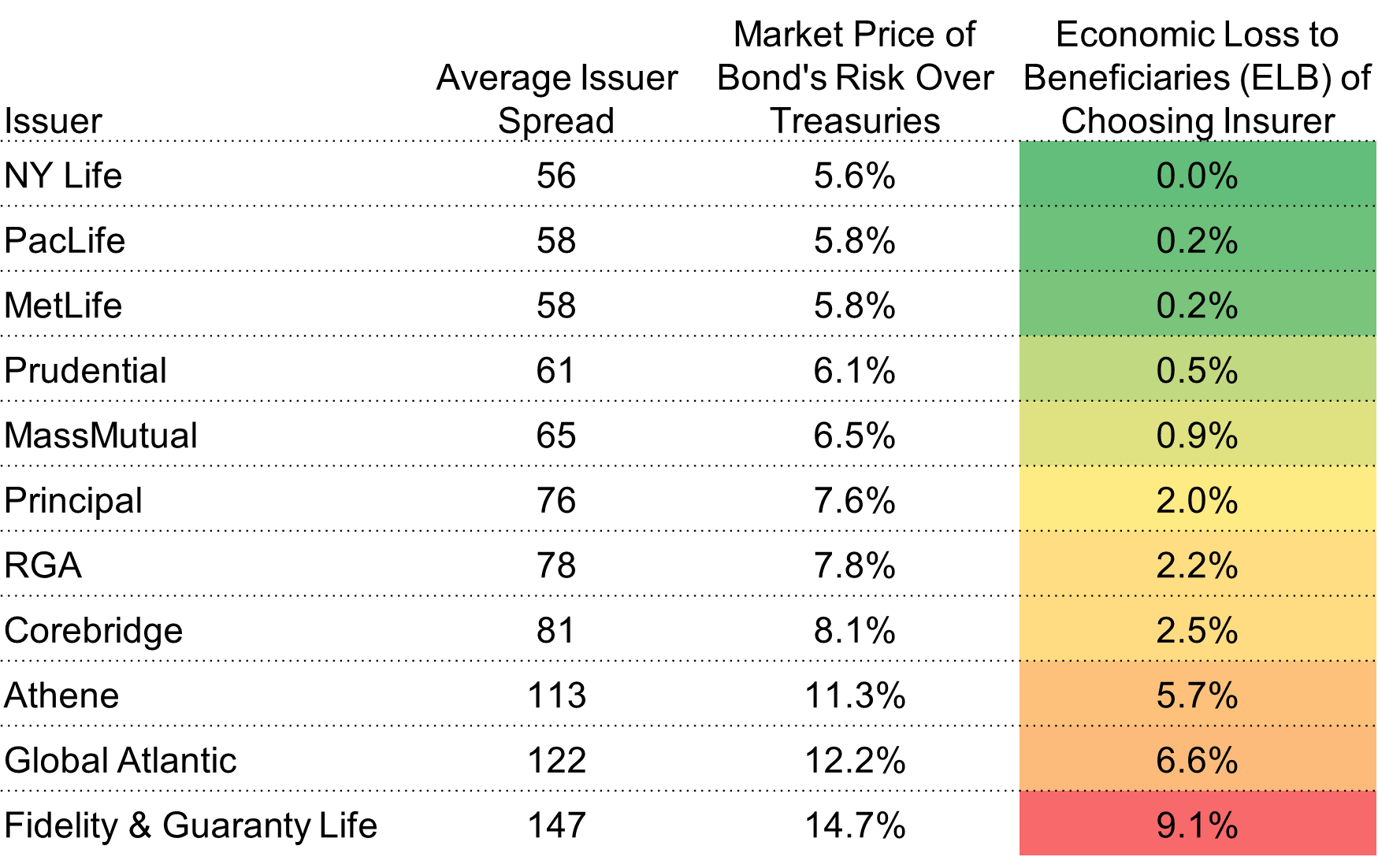

Average Issuer Spread ELB

Sources: Bloomberg, NISA calculations. As of 6/30/2026.

Reported issuer spreads are 5-year, option-adjusted spreads implied from the spread curve fitted through the universe of FABN bonds, respective to each issuer.

Insurers chosen are based on “U.S. Pension Risk Transfer Update: 2024 Year In Review and Future Expectations,” AON, February 2025, who were identified as Mid-size/Large or Large/Jumbo participants and have issued securities at the policy level for the institutional fixed income market.

The ELB methodology uses readily available market spreads on bonds issued by PRT providers that are pari passu with policy holders, specifically, spreads on Funding Agreement Backed Notes (FABNs). Our measure utilizes the market’s ability, and incentive, to incorporate all other risk assessments (e.g., published ratings, capital ratios, etc.) into the FABN pricing and thus, more holistically assess risk.

We believe that reviewing market pricing for comparable investments/policies clearly aligns with ERISA’s prudent expert standard – i.e., the market is a competitive environment with a multitude of experts seeking to maximize their risk-adjusted outcomes. In fact, one could argue that market price is singularly sufficient for assessing the credit risk of a PRT provider, as all other information (rating, capital structure, portfolio quality, etc.) is available to all market participants, and therefore presumably embedded in the price.