The December payrolls report released this morning represents the first clean view of the labor market since September. The BLS stated that the December figures were not impacted by the shutdown. The results suggest that the labor market is stabilizing, though not rebounding strongly. The establishment survey showed an increase of 50,000 jobs in December, of which 2,000 were federal government jobs. The 179,000 decline in federal government payrolls from the DOGE deferred layoff program was entirely concentrated in the month of October. Private payrolls increased by 37,000 in December. Diffusion was still narrow, with job creation limited to healthcare and hospitality sectors while employment declined in goods sectors like manufacturing, transportation, warehousing and retail.

The household survey was stronger, with a 232,000 increase in employment and a one-tenth decline in the unemployment rate to 4.4%. The unemployment rate for November was also revised down one tenth, confirming that the 4.6% figure reported originally was distorted by shutdown effects. Given the decline in labor supply and falling rate of breakeven employment growth, the Fed has focused more on the unemployment rate than the level of payroll job growth. The decline in the unemployment rate should therefore give the Fed some comfort that downside risk to employment has dissipated, supporting their decision to signal a pause in January. We maintain the view that the Fed will remain on hold through the end of Chairman Powell’s term in late May and only resume cutting in the second half of this year when tariff pass-through concludes and inflation resumes its deceleration towards 2%.

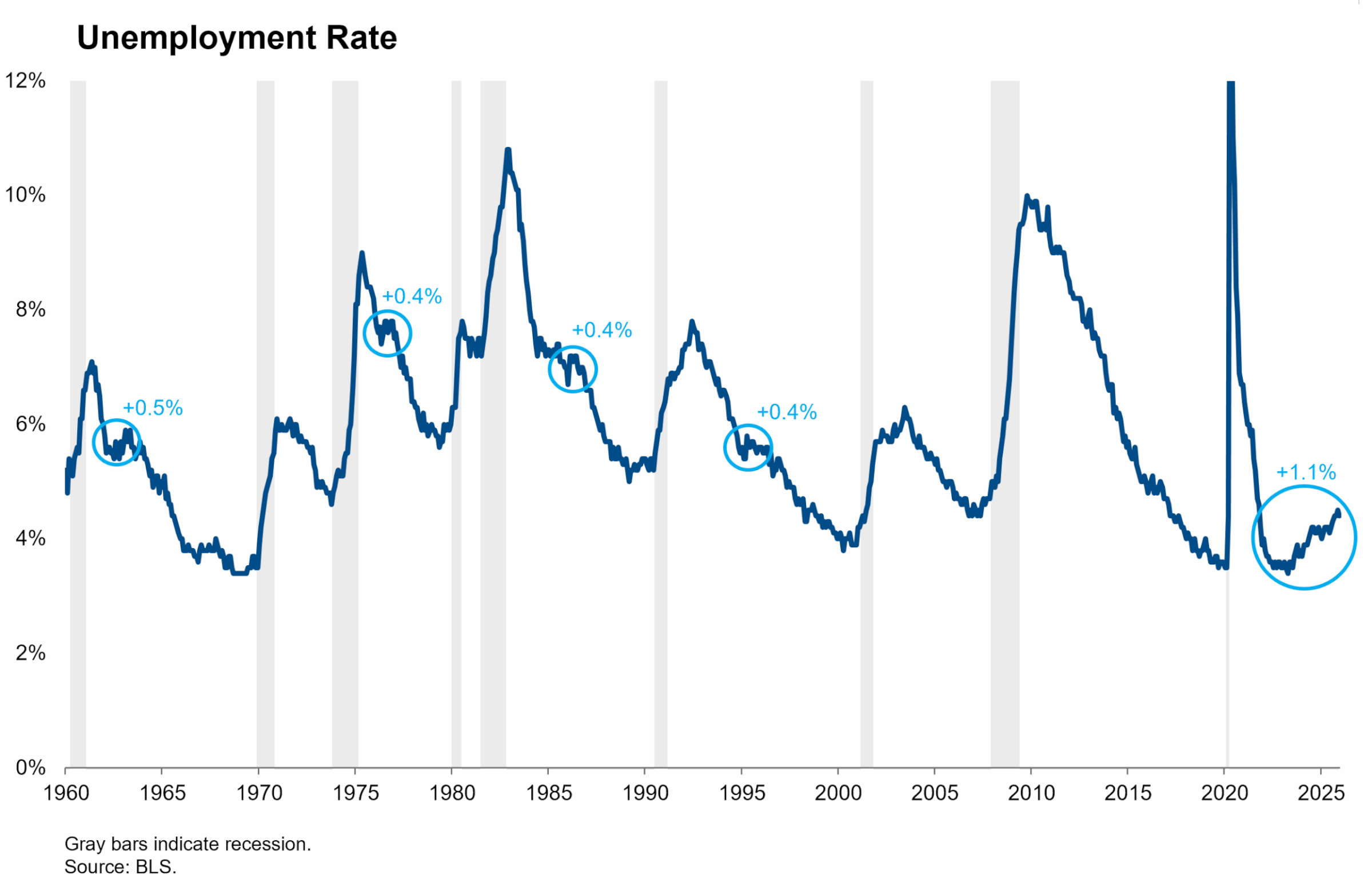

The labor market appears to be stabilizing but we are not out of the woods yet. Job creation remains narrow and uncomfortably close to zero. The unemployment rate remains on a gradual uptrend despite the improvement in the latest month. One of the key questions for the 2026 economic outlook is how much inertia is contained within this labor market slowdown that began in early 2022. That slowdown has steered the labor market into uncharted waters: the unemployment rate has never risen this much above the cycle low outside of a recession. The 1.1% trough-to-peak increase has happened slowly enough that the Sahm Rule has not been triggered.

It seems possible that this is payback for labor hoarding during 2021-2022 rather than an inertial decline in labor demand. If that’s true, then the unemployment rate could stabilize or decline and allow the Fed to cut in response to disinflation rather than employment risk. But it’s also possible that the rising unemployment rate contains self-perpetuating inertia through the consumer spending channel. We’ll need more data to confirm which path we are on. We are also mindful that trade policy uncertainty might continue to recede in the new year and boost employers’ confidence to resume hiring.