As often happens when there is an unexplained rise in interest rates, some market participants recently speculated that China has been dumping their Treasury holdings. We continue to believe that any threat by China to weaponize their Treasury holdings as a tactic in the trade war would not be credible. The logic is the same as we’ve stated: any disorderly sales by China would quickly be offset by Fed purchases. For a Chinese liquidation to have its desired effect, China would have to disrupt the functioning of the Treasury market. We do not believe the Fed will allow that to happen. The Fed Put on Treasury market functioning is always close to the money (as distinct from the Fed Put on the broader U.S. economy, which may be out of the money for a time as inflation rises this summer).

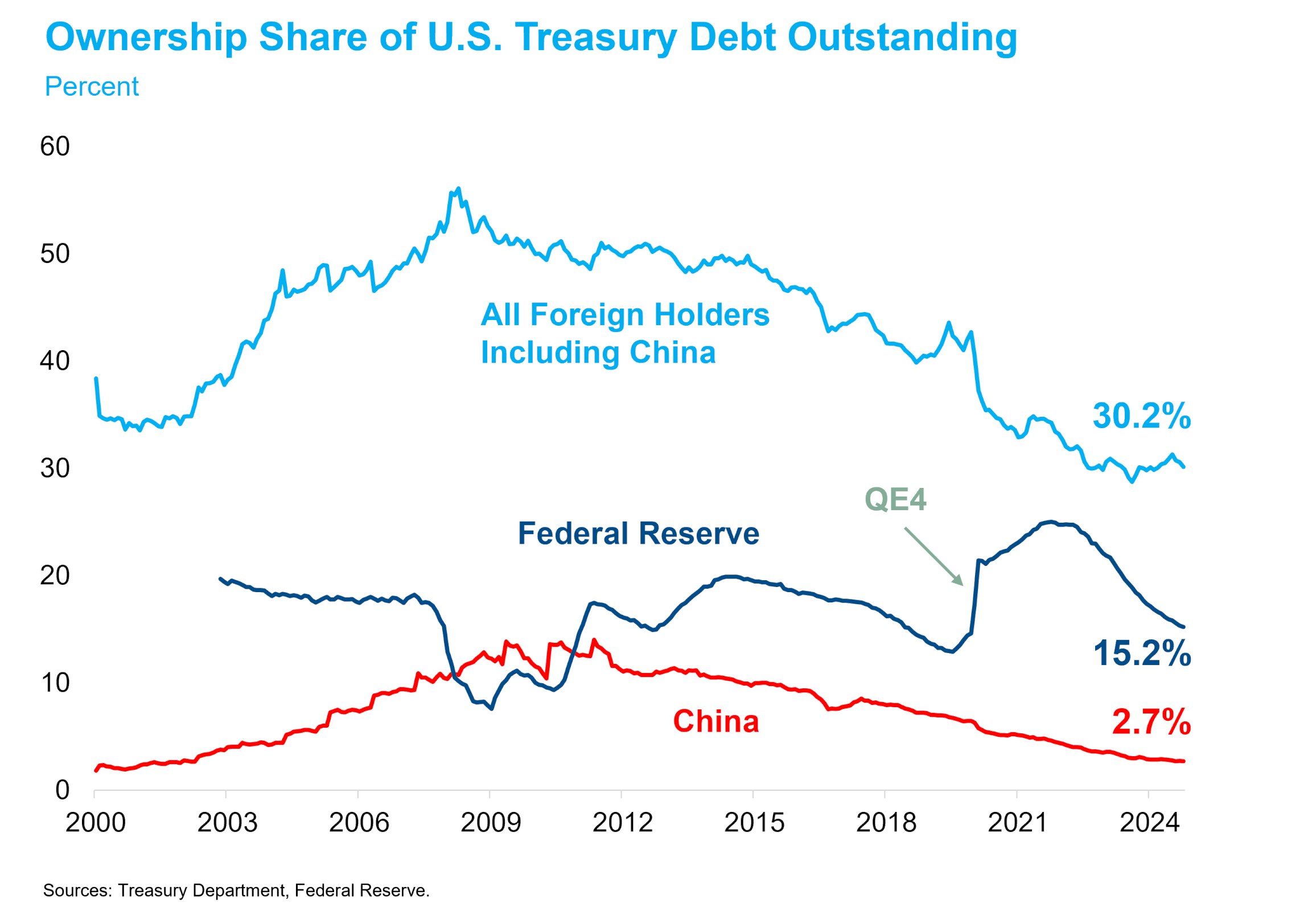

The case is even stronger now as China continues to fade in importance as a funding source for the U.S. government. China’s officially reported Treasury holdings are $784 billion, less than 3% of marketable Treasury debt outstanding. That’s down from a peak above 13% before the Global Financial Crisis. As the Treasury Department has increasingly turned to domestic investors in the last decade, China’s importance has declined even faster than other foreign investors. China accounted for one quarter of all foreign holdings before the GFC vs. about 10% today.

It is widely suspected that China owns an additional $100-200 billion of Treasuries that are not captured in the official data, but even that larger war chest wouldn’t allow them to challenge the Fed. The Fed’s nearly limitless firepower was demonstrated in March 2020 when they purchased $915 billion of Treasuries in the first three weeks of QE4. For perspective, if the Fed were forced to intervene and purchased all of the Treasuries thought to be owned by China, its balance sheet would grow by an amount equivalent to just over a year’s worth of current QT runoff. While this activity would not be consistent with the Fed’s near-term focus on taming inflation, it is hardly a cause for alarm.

We are not dismissing the importance of foreign investors. Treasury has a lot of bonds to sell, and should be courting buyers around the globe. Note that foreign investors have increased their holdings by over $6 trillion since 2007 — all of their decline in ownership share is explained by the substantial growth in Treasury debt outstanding. If foreign buyers turned away from U.S. debt en masse, Treasury would likely face higher borrowing costs. But we think that risk is low, and even if it did occur, it would play out over many years. The more acute risk of a fire sale by China is less of a concern, in large part because of the Fed’s powerful backstop.