The Federal Reserve left their policy rate unchanged today as expected, embracing the wait-and-see attitude that they have adopted since President Trump escalated the trade war in March and April. Today’s events disappointed those market participants who expected a signal that rate cuts would begin at the June or July FOMC meetings. While today’s FOMC statement highlighted the elevated uncertainty and stagflationary risks emanating from the trade war, nobody, including the Fed, knows how that trade war will evolve in the weeks and months ahead. Chairman Powell reiterated at the press conference that the cost of waiting for further clarity is low.

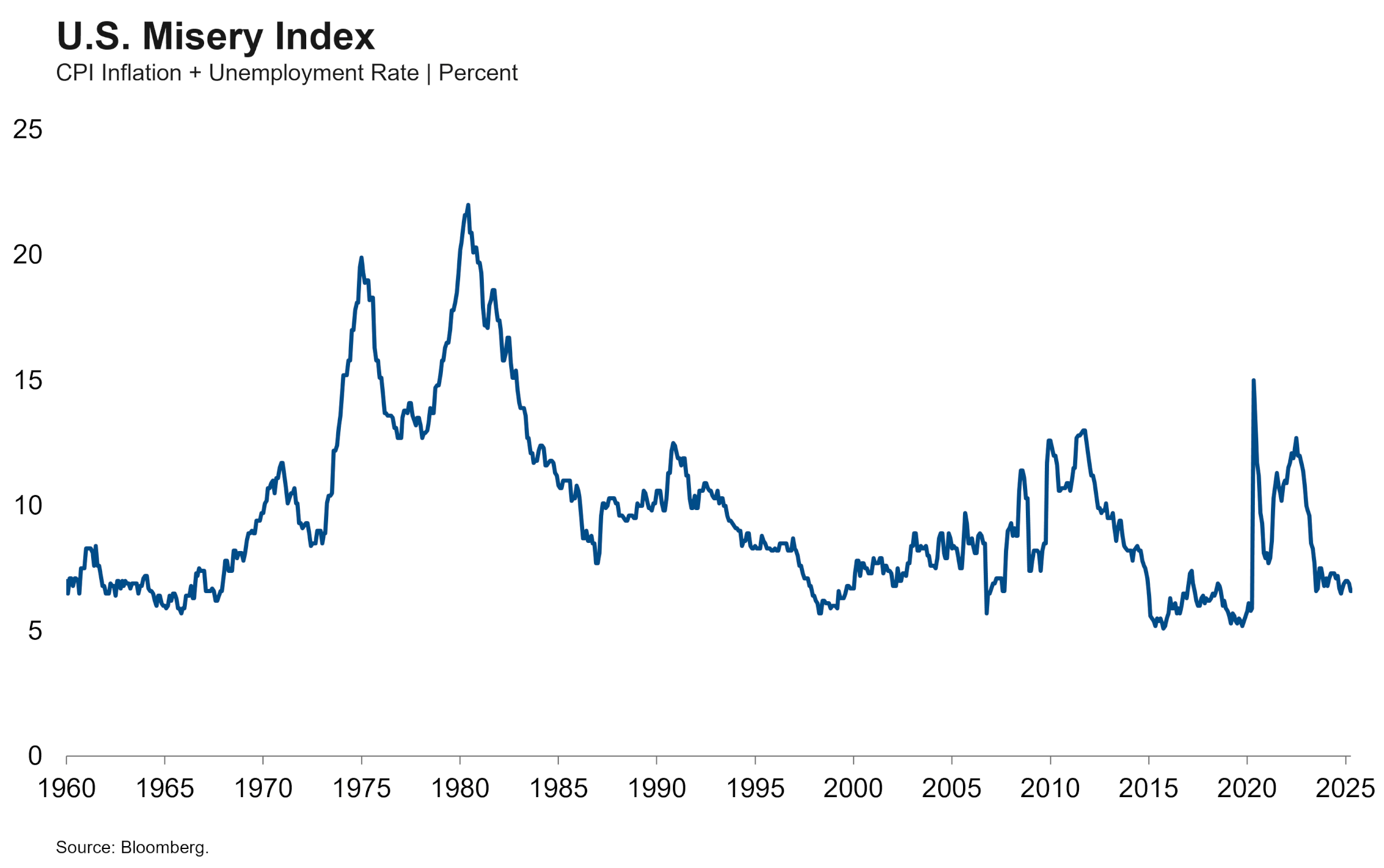

Growth remains solid despite the distortions from imports in Q1. The unemployment rate remains low. While inflation remains above target, it has eased significantly since its post-pandemic peak. In quantitative terms, the misery index is very low! Powell actually repeated the word “wait” 25 times on Wednesday. With apologies to Tom Petty, it seems the waiting is – in fact – the easiest part.

We continue to believe the Fed will remain on hold at their June and July meetings while they assess the nature of any tariff-induced inflation that may arise and ensure that inflation expectations remain well anchored. Short rate markets have repeatedly implied earlier cuts, pricing at least 1-2 cuts this summer throughout the month of April. The most likely path to those earlier cuts, in our opinion, is for President Trump to reduce tariffs early enough that the tariff-induced inflation never materializes. Confidence among market participants is fading on that score, and short rate markets are currently pricing just 82% odds of a single rate cut across the two summer meetings.