Like most financial markets, interest rate markets have experienced pronounced volatility over the last 18 months (ending in April of 2009). Many pension liability hedge strategies that relied heavily on derivatives (most notably interest rate swaps) and Treasury bonds significantly outperformed changes in the plan’s reported liability. The question that naturally arises is: Are strategies that utilize interest rate swaps still effective at reducing the plan’s funded status risk?

The evidence below argues for a resounding yes: Recent experience actually confirms the effectiveness of swaps in reducing interest rate risk for pension plans. In this paper, we analyze a representative hedge strategy in terms of the market-related determinants of pension liability volatility. We find that while Aa spreads were not effectively hedged by swaps over this period, the general level of rates was. As a consequence, plans with hedged liabilities experienced less funded status volatility than those with unhedged liabilities. This is despite the fact that Aa spreads were more volatile than those in prior years.

It is worth noting at the outset that our treatment of the liability’s exposure to corporate bonds is very generous. While conventional liability assessments (FAS, PPA, etc.) use corporate bond yields, the liability is not a corporate bond. A substantial portion of corporate bond spreads is compensation for the possibility of default – and such default risk is not present in the liability. It is conceivable that a purely economic proxy of the liability actually has little or no corporate spread sensitivity. As the case can be made for an interest rate hedge program even with this complication, we discount the liability at corporate yields throughout this paper for a more compelling conclusion.

Two Market-related Components of Liability Risk

The “pension liability” is the present value of the projected benefit payments generally based upon a corporate discount curve. Fluctuations in reported pension liability values can be attributed to two distinct market risks: (i) general interest rates (which are represented here by Treasury yields); and (ii) corporate bond spreads (which are represented here by Aa spreads). Both of these components have experienced high levels of volatility by historical standards over the last 18 months.

The pension liability has identical sensitivity to a basis point change in either component. Of course, that doesn’t mean that the liability’s volatility is comprised equally of general interest rate volatility and credit spread volatility. The relative importance of these components is an empirical question, and has varied substantially over time.

While swap spreads and credit spreads have, at times, been correlated, interest rate swaps have no direct connection to the credit markets. A hedge strategy relying primarily on interest rate swaps will likely not track liability changes due to credit spread changes. When credit spread movements are relatively large (which was the case in 2008), a smaller proportion of the liability’s fluctuations may be offset by the interest rate swap hedge strategy. In other words, although the interest rate swap hedge is working as intended to offset variations in general interest rates, its effect may be difficult to discern due to the large fluctuations in spreads.

What Has Changed?

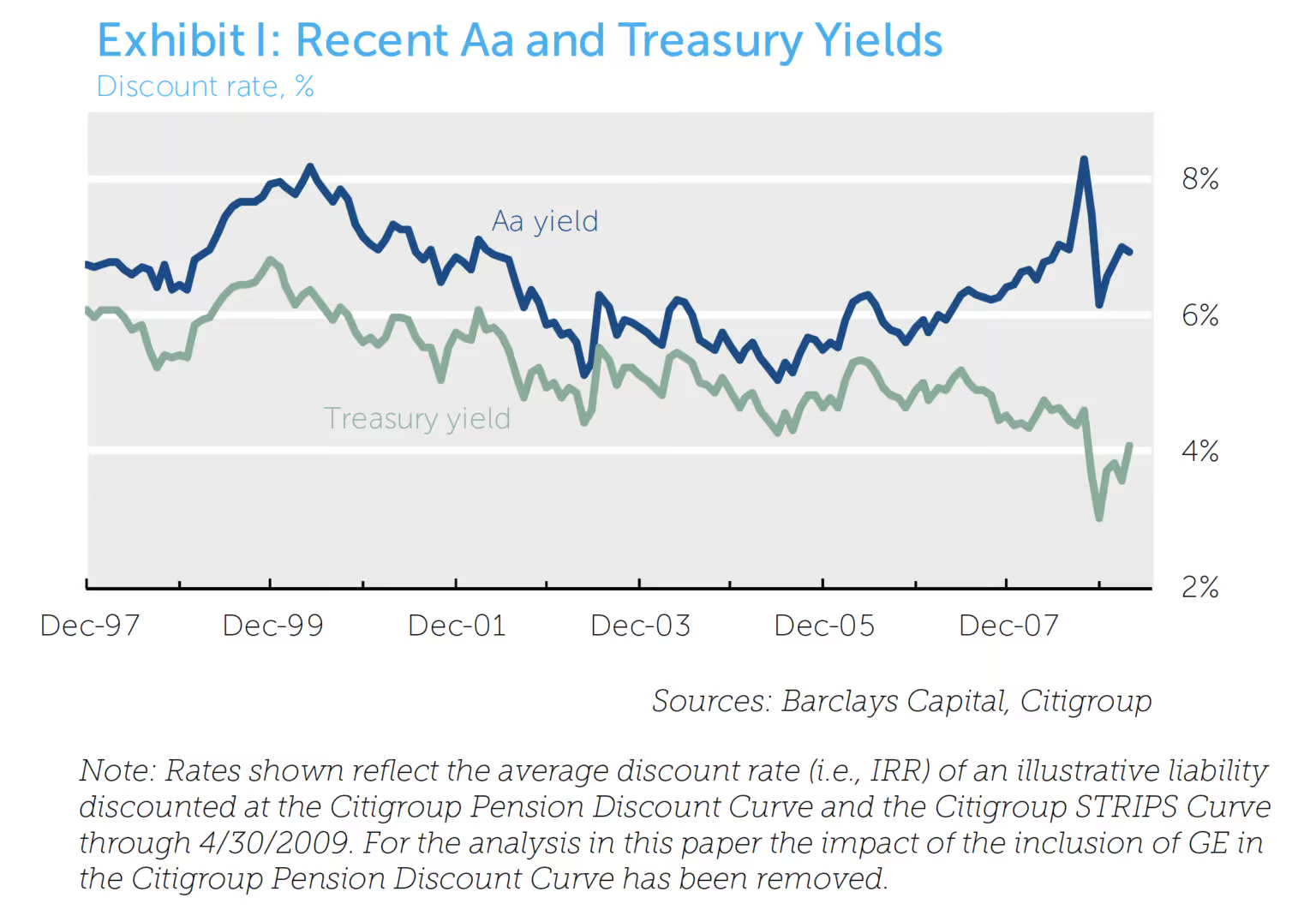

Historically, the yields of corporate bonds and Treasuries have moved relatively in tandem. Since mid-2007, however, corporate bond yields have diverged from Treasury yields (See Exhibit I). Specifically, corporate bonds have experienced dramatic spread widening. Further, spreads have been remarkably volatile over this period. These two facts combine to suggest that one component of the liability’s discount rate – credit spreads – has become an increasingly larger driver of changes in the liability’s value.

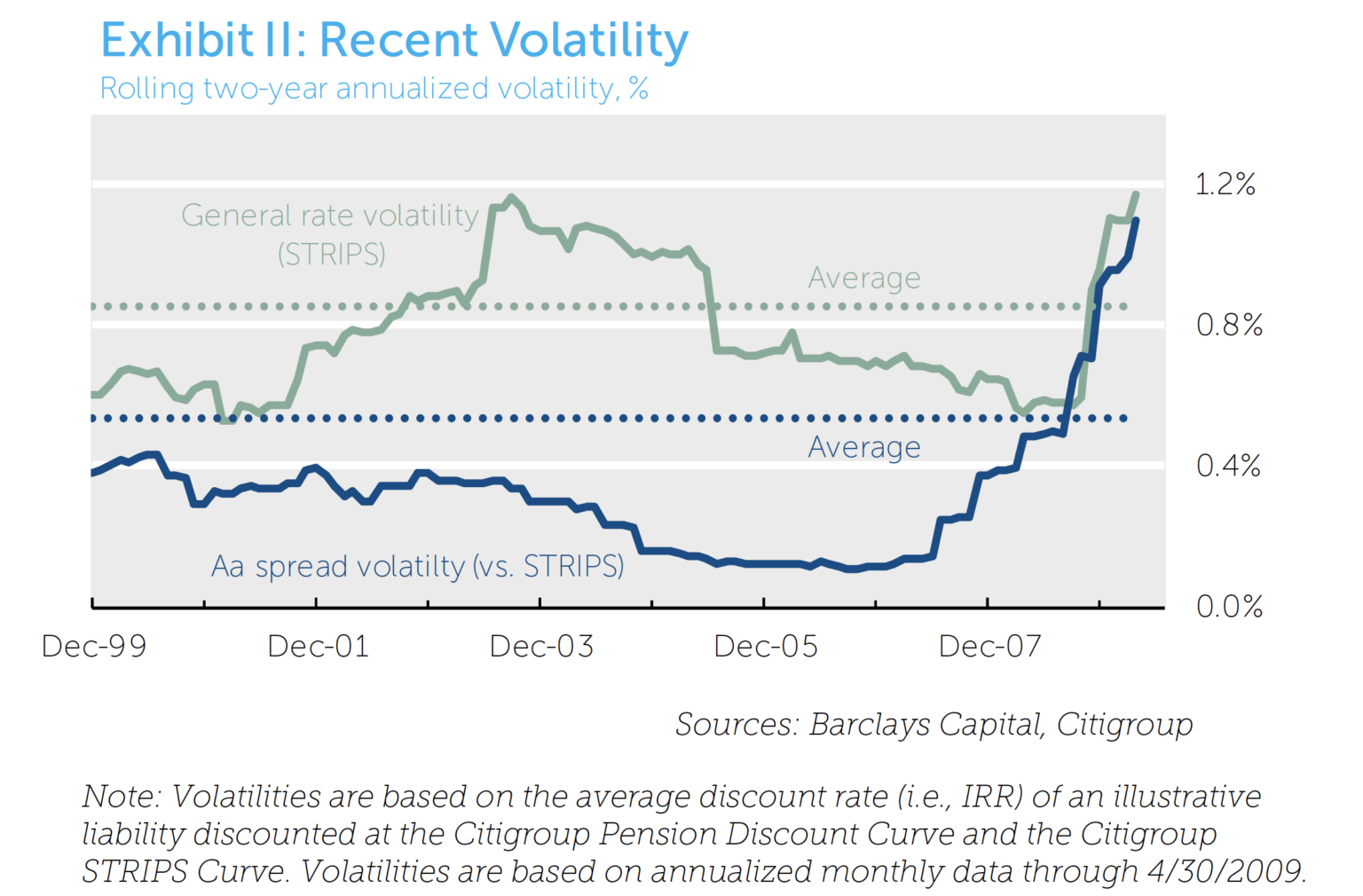

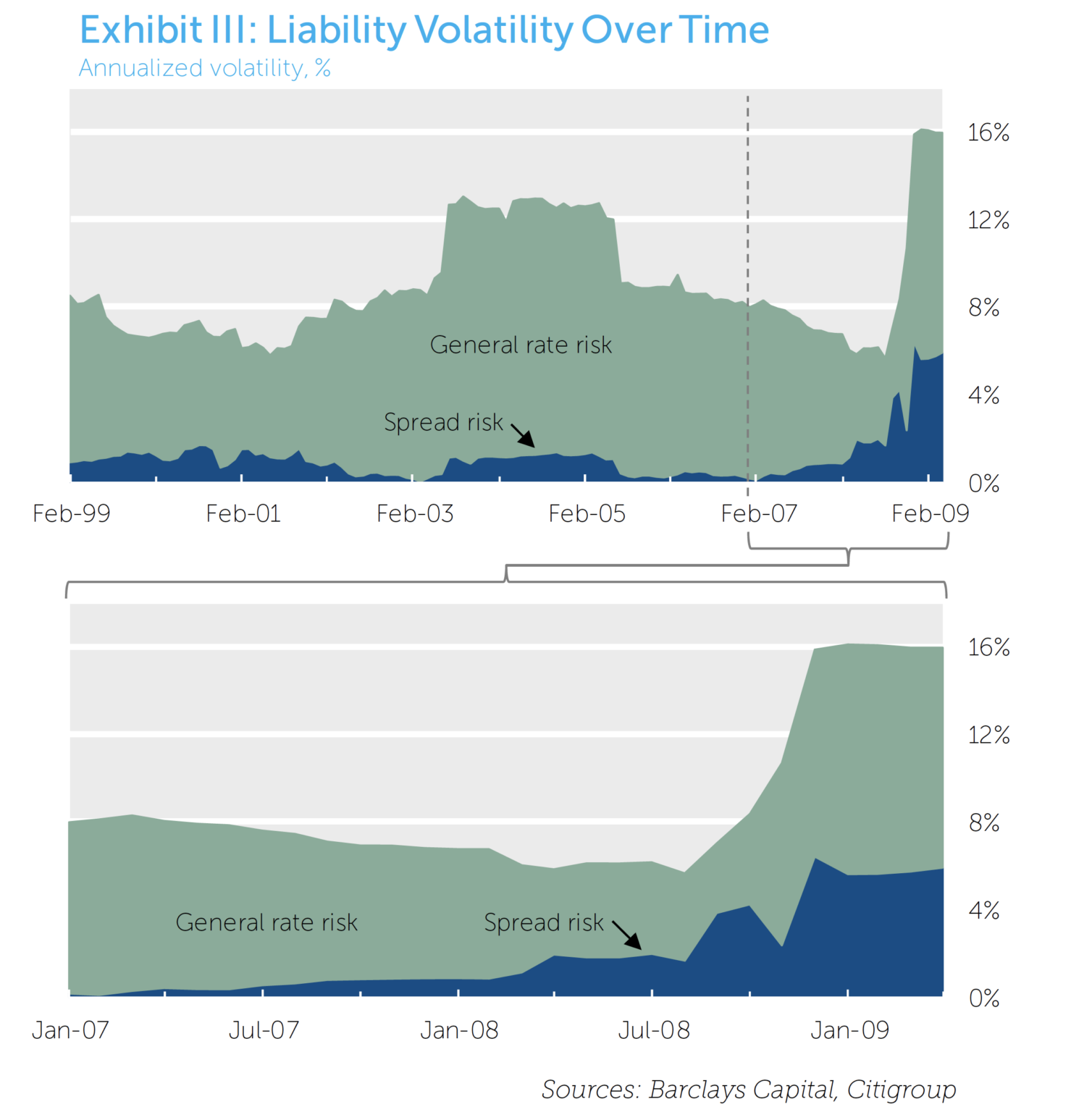

Exhibit II depicts the magnitude of this increase in volatility. Historical spread volatility has increased nearly ten-fold since June 2007 to its highest level in at least the last 20 years. Although general rate volatility has also increased and is at the high end of its 10-year range, the increase has not been as dramatic relative to that of spread volatility. Thus, while both spread volatility and general rate volatility are important, Exhibit III illustrates that an increasing proportion of corporate yield volatility is due to changes in credit spreads. As a consequence, the effectiveness of swaps in hedging the pension liability over this period has been masked by the tracking error attributable to spread volatility. It should be noted however that the absolute sensitivity of the liability to changes in general interest rates remains at the high end of its historical range.

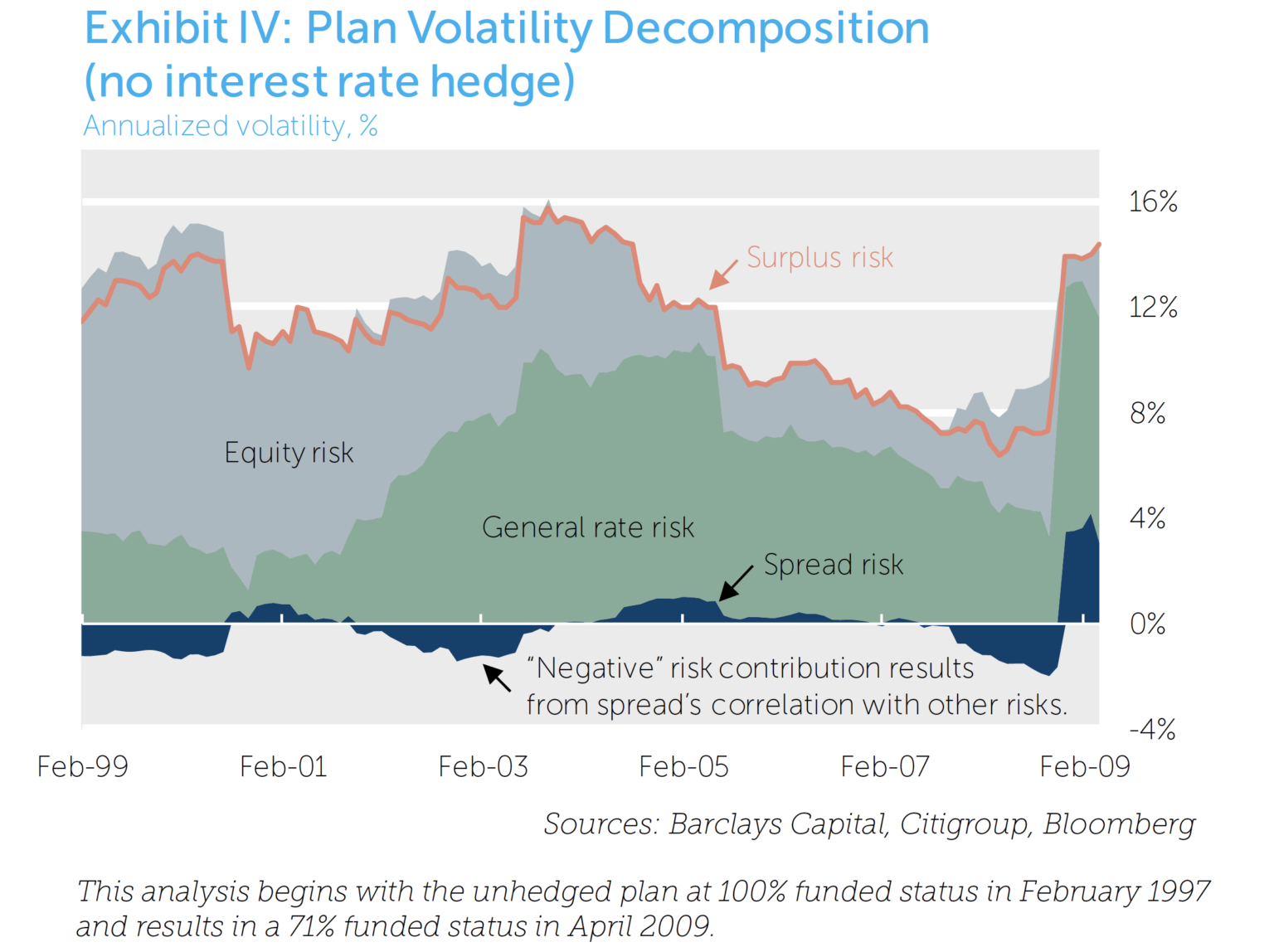

The Impact of Spread Volatility on the ‘Typical’ Plan

The previous section is at best an incomplete summary of the relative importance of general interest risk and spread risk. Only when we include the typical plan’s allocation to risk assets can we begin to understand the drivers of a plan’s funded status risk. The figure below shows the composition of a “typical” plan’s risk among risk assets, liability spread risk and liability general interest rate risk. For expository ease, we have simplified this plan’s asset allocation to 40% S&P 500, 20% EAFE unhedged and 40% Barclays Capital Aggregate.

In the presence of a typical allocation to risk assets, the importance of the liability’s spread sensitivity is considerably diminished. Because corporate spreads are highly correlated with equity returns, these sources of volatility partially offset one another (the long position in equities is directionally offset by the short position in liability spread exposure)1. Currently, general rate risk contributes approximately twice as much risk as either spread risk or equity risk when this offset is taken into account.

Are Swap-based Hedges Still Effective?

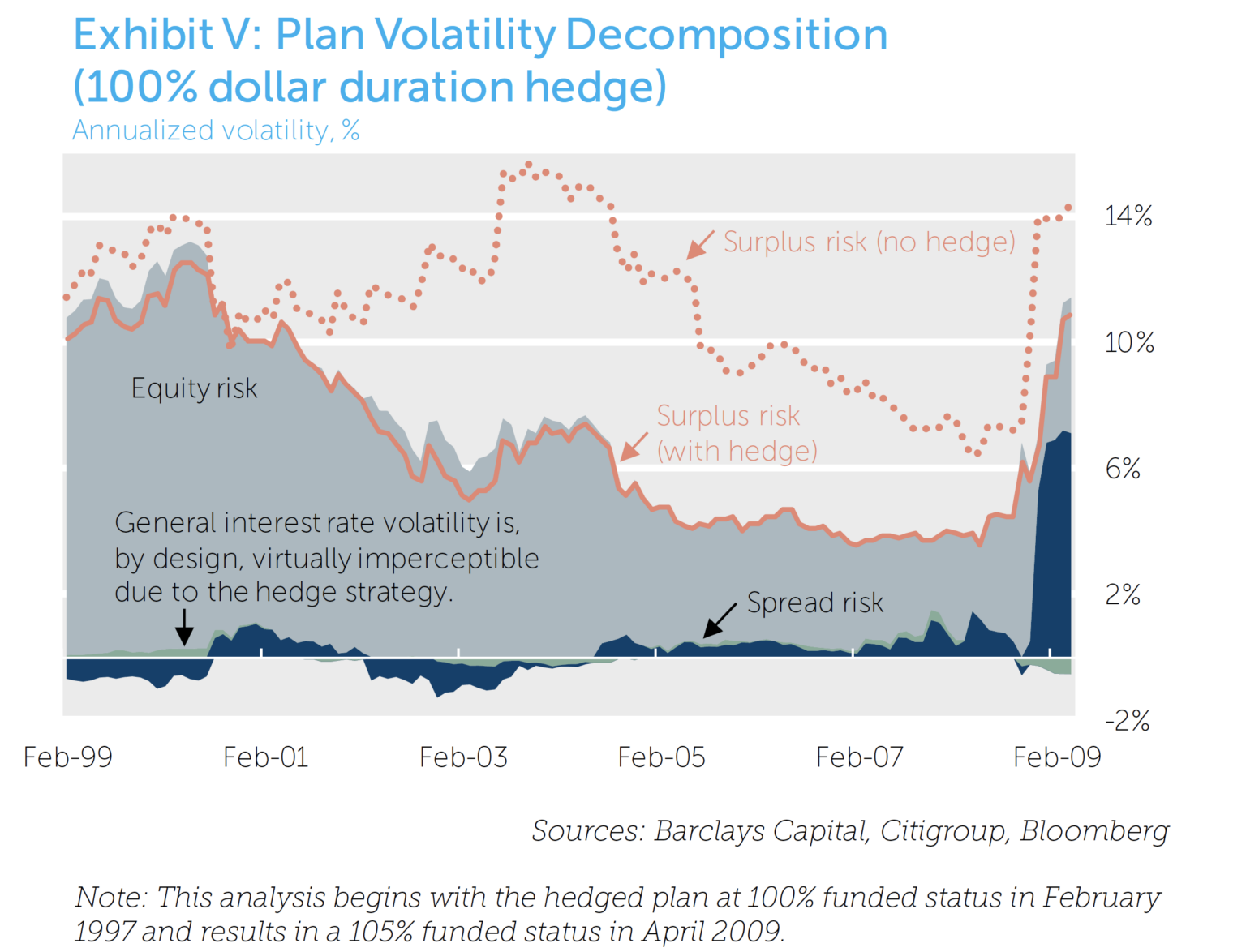

Since an interest rate overlay strategy based on swaps is typically designed to hedge general interest rate risk and not spread risk, it may appear that the hedge is not working when spread volatility is a relatively large driver of liability volatility, as has recently been the case. One way to evaluate the ongoing effectiveness of a swap-based general interest rate hedge is to examine the risk reduction associated with the strategy in the context of the plan’s total funded status volatility.

As shown in Exhibit V, the funded status risk of our illustrative plan is significantly reduced by hedging general interest rate risk throughout the last decade; most recently, funded status volatility is reduced from approximately 14% to 11%. This estimate likely understates the potential benefit of a sophisticated hedge as it is based on a simple dollar duration hedge. More robust strategies that utilize empirical duration estimates, partial durations, etc. would likely improve this result, but are outside the scope of this paper.

Our analysis demonstrates that a material portion of a plan’s funded status risk derives from general interest rate volatility, even during periods of extreme credit spread volatility. In addition, even when a swap-based hedge strategy does little to address spread risk, it significantly reduces overall funded status volatility. Indeed, in recent periods, the reduction in surplus risk due to an interest rate hedge program has been comparable in size to the total risk contribution from equities!

Our analysis does not suggest that adjustments to general interest rate hedge strategies are never warranted. Reasons for adjustments might include tactical views on general rates (given adequate risk tolerance), changes to hedge ratios due to the “effective” duration of various hedge vehicles, etc. Further, it is likely that the composition of a hedge strategy could change to emphasize instruments that can address both general interest rate movements and spread movements (e.g., corporate bonds).

Conclusion: One Hedging Program, Two Distinct Hedges

Although there may be a natural tendency to question the effectiveness of a hedge strategy that produced significant gains vis-à-vis the reported liability, our analysis demonstrates that even during such a period an interest rate hedge program effectively offsets one component of a pension liability’s volatility. The unprecedented market performance of the last 18 months was, however, a useful reminder that spread volatility, while largely dormant during the tranquil market period that preceded it, can be a meaningful determinant of a plan’s funded status performance.

Since volatility in spread markets may persist for some time, it may be reasonable to divide a hedge program going forward into two components; the general interest rate hedge and the spread exposure hedge. The general interest rate hedge is likely to be implemented using Treasuries and interest rate swaps, etc., while the spread hedge would be comprised of spread-sensitive assets – some that also contain general interest rate exposure (e.g., corporate bonds) and, perhaps, some that likely do not contain general interest rate exposure (e.g., equities, high yield bonds, etc.). This bifurcation will help avoid the pitfall of allowing higher spread volatility to obscure the effectiveness of general interest rate hedges. In so doing, it will be clear that interest rate hedging remains an important tool to manage overall plan funded status risk.