Nonfarm payrolls declined by 92,000 in February, the largest monthly decline of the cycle if we look past the government layoffs from October. The unemployment rate rose by a tenth of a percent to 4.4% despite a decrease in the labor force participation rate. The payrolls figure was biased lower by something like 30,000-50,000 because of nursing strikes and cold weather, but the overall report was still very weak even after accounting for these distortions. If we adjust for these distortions in February and account for the very strong report in January, the 3-month moving average of payroll growth is 19,000. That figure is quite low by the standards of the post-pandemic era but only modestly below the breakeven payroll growth rate of roughly 50,000.

Long story short: this was a weak report, but it does not fundamentally alter our view formed as the economic data fog lifted after the government shutdown. The labor market has stabilized in a low-hire, low-fire equilibrium, but is not yet out of the woods. We would need to see several more weak prints, and some indication of rising layoffs, before we would start to worry about the labor market tipping over into a recession.

The jobs report was a second-order concern for Treasury market participants, who remained focused on the war in Iran, the impact on global energy markets, and the implications for monetary and fiscal policy. The rise in global energy prices represents the third major stagflationary shock for the global economy in recent years, following the pandemic and the Russia/Ukraine war. The key questions at the moment are the magnitude and duration of the shock. We are not in any position to predict the course of the war or the navigability of the Strait of Hormuz, but we can say that the oil futures market is pricing the impact to be fairly short-lived. While front-month WTI futures have risen by $24 this week, the September contract is higher by a comparatively modest $7.

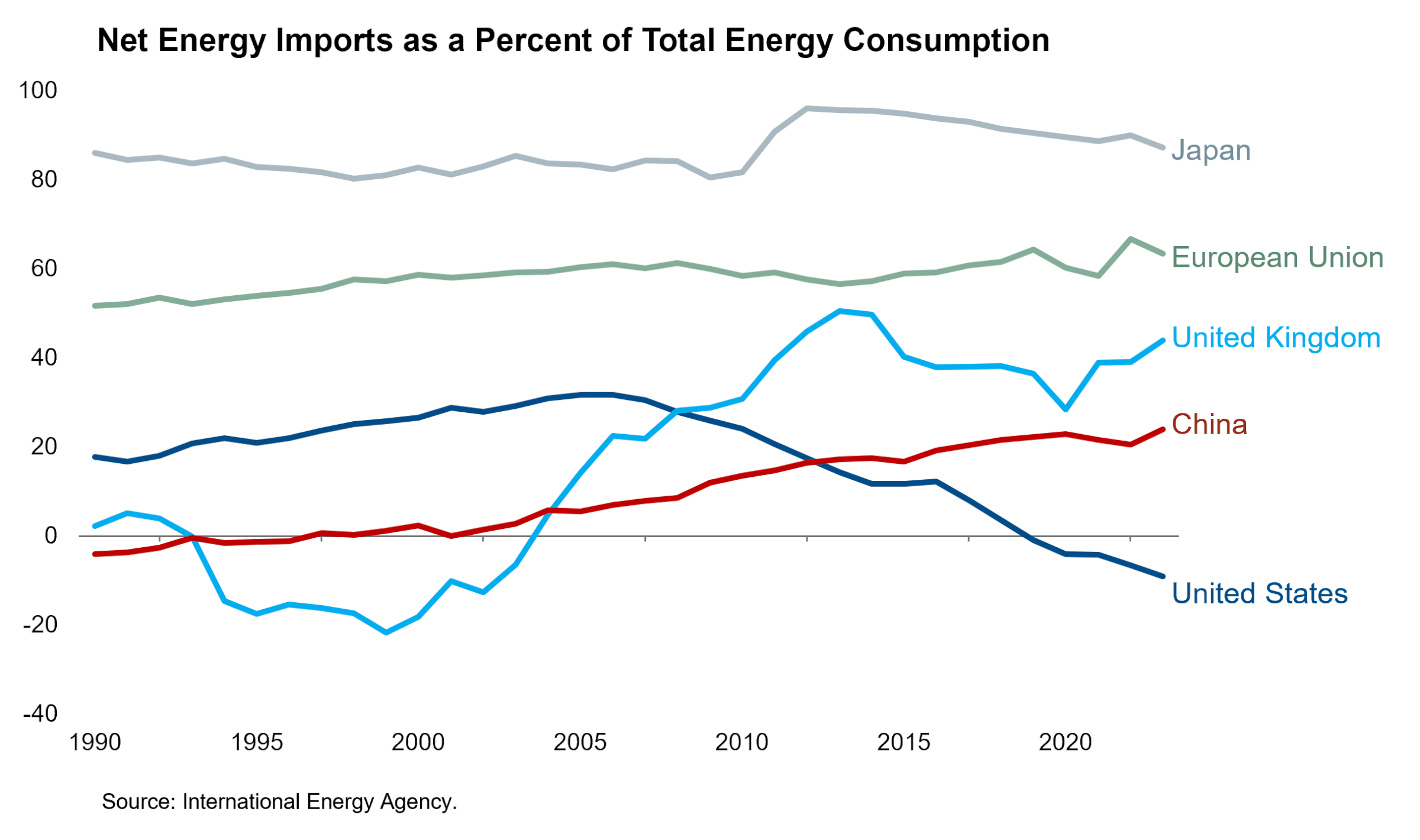

One thing that we can say with confidence is that the U.S. economy is far less exposed to this energy price increase than most other advanced economies. While the U.S. has achieved energy independence in the last two decades, the U.K. has taken the opposite path: reducing domestic production and increasing their reliance on imported energy. Europe and Japan consistently import most of their energy. While China has surged their domestic production of renewable electricity in recent years, their energy needs are growing so fast that they still import nearly a quarter of their energy.

Europe will bear the brunt of the stagflationary shock from this energy price spike, in an echo of the energy crisis following the outbreak of the Ukraine war in 2022. Natural gas futures prices at the regional hub in the Netherlands have risen this week by 65% in the front month and more than 30% in all contract months through July 2027. If this level of energy inflation is maintained, it will likely require monetary tightening and fiscal easing by European governments. In 2022-2023, many European nations spent 3-6% of GDP in fiscal support to shield consumers from energy inflation. This would come on top of Europe’s intention to massively increase defense spending, at a time when global government bond investors are increasingly nervous about fiscal sustainability.

Market participants are also expecting a monetary policy response to energy inflation in Europe. Market pricing has flipped this week from cuts to hikes for the European Central Bank, the Swiss National Bank, and the Riksbank. The odds of a cut at the March 19 Bank of England meeting have declined from 86% to 11%. The expected fiscal and monetary response has led to a 30-50 bp increase in European government bond yields this week, led by intermediate tenors.

We have been surprised by the degree to which Treasury yields have followed European government bond yields higher. Treasury yields have risen by as much as 19 bps this week, also led by intermediate tenors. A third significant stagflationary shock is indeed most unwelcome for the U.S. economy, as the soft landing had just come back into our sights. We ultimately expect the magnitude of the economic shock—and consequently the impact on government bond yields—to differ greatly across the Atlantic.