In one of the most economically consequential rulings in its history, the Supreme Court today held in a 6-3 decision that “IEEPA does not authorize the President to impose tariffs.” This decision invalidates around $175 billion in revenue raised last year, which is more than half of the total revenue raised by new tariffs issued by the second Trump administration. Tariffs issued under other statutes beyond IEEPA will remain in place. The court did not issue any guidance regarding refunds of IEEPA tariffs, leaving that question to lower courts. We assume those lower courts will insist on refunds to the importers who paid the tax to Customs and Border Protection. The refund process will likely involve years of litigation between importers, wholesalers, retailers, and consumers as to who bore the incidence of the tariffs.

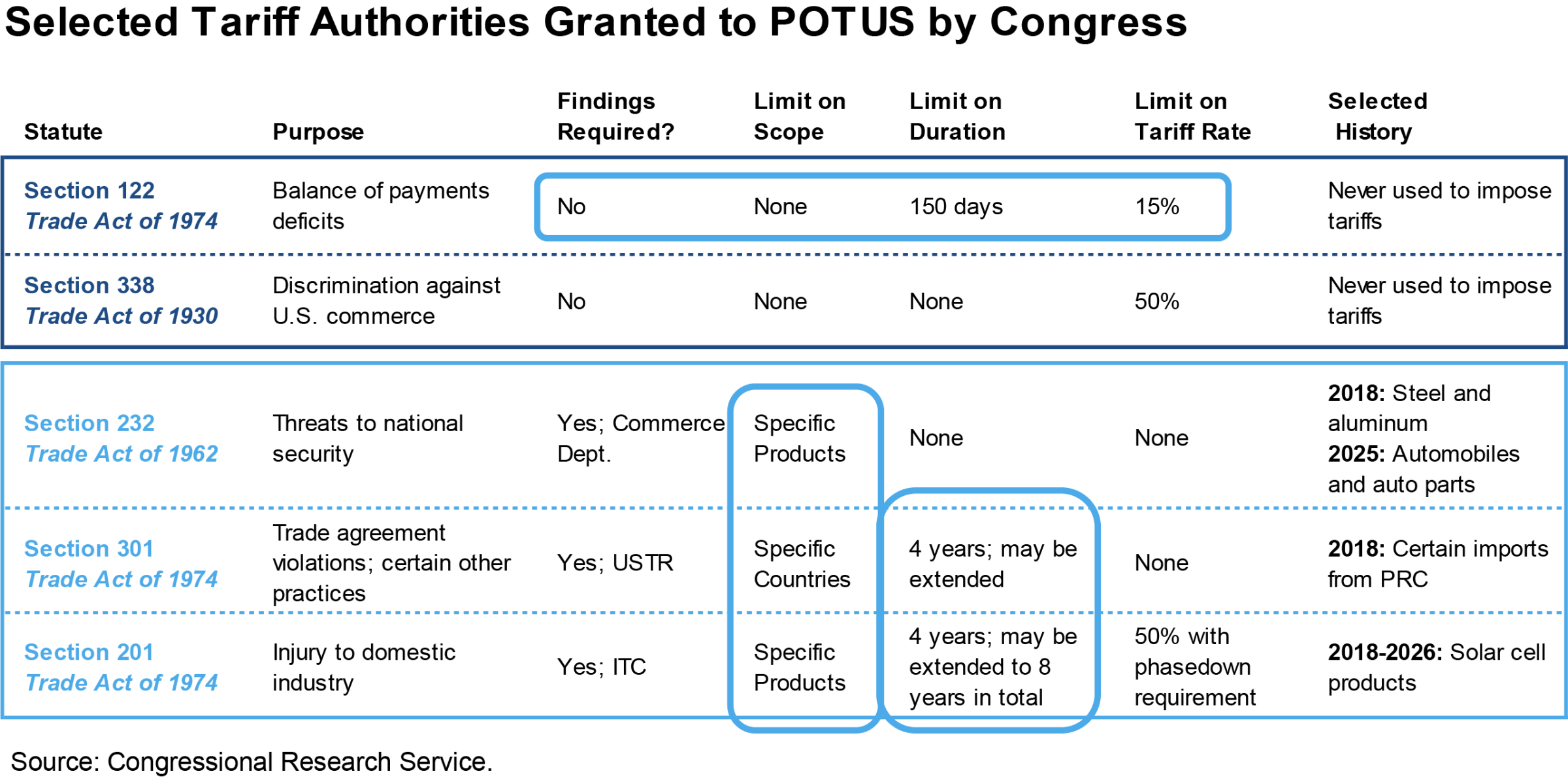

As we explained in our quarterly economic webinar last month, the removal of IEEPA authority is only a minor inconvenience for the president’s efforts to impose tariffs and restrict foreign trade. Congress has granted the executive branch ample tariff authority under other statutes. President Trump has already announced this afternoon that he will respond just as we described in the webinar by immediately imposing a 10% global tariff under Section 122. We expect that the tariff authority will expire after 150 days because we do not think the president has the votes in Congress to extend it. That temporary tariff will be used as a bridge to longer-lasting tariffs under Sections 232, 301 and 201, which are targeted at specific products or countries where the U.S. suffers from unfair trading practices, of which there are many genuine cases. That is why these other statutes have been used many times in the past, in contrast to IEEPA, which has never been used to impose tariffs.

A Final Spurt of Uncertainty Before Some Relief

Trade policy uncertainty was the most important factor in the U.S. economy in 2025 in our opinion. That uncertainty spiked on April 2 but has been receding ever since April 9. Trade data released this week show that the realized tariff rate actually declined from a high of 10.9% in October to 9.4% in December. This is less than half of the roughly 22% rate that would have resulted from the April 2 announcement, and even far below the existing statutory tariff rate because the administration has exempted more than half of all imports from the new tariffs. The moderation of trade policy has reduced uncertainty and allowed for a rebound in business confidence that has stabilized the labor market and economic growth more broadly.

We expect that the 10% global 122 tariff will result in a realized rate that is at or below this 9.4% figure once it is established, though it will depend on how the current exemptions are transferred to the new regime. This transition from IEEPA to other authorities will raise uncertainty for businesses and consumers for the next six months, and it will create winners and losers among companies and countries. But the end result will be a tariff rate that is fairly similar to the current level. The uncertainty may cause a temporary drag on business investment and hiring, but we don’t expect that impact to knock the economy off its path back towards a soft landing. Once the new regime is in place later this year, trade policy will be more grounded in familiar procedures and less subject to the president’s whims.

Fiscal Impact

If $175 billion of the tariff revenue raised last year was an illusion, so too was that portion of the deficit reduction. The deficit had improved from 6.9% in calendar year 2024 to 5.6% in calendar year 2025. A $175 billion refund would worsen the 2025 deficit back to 6.1%. However, this will only be a temporary hit until a roughly 9-10% realized tariff rate is reimposed under other authorities. The bigger question is what this means for the long-run outlook for tariff revenue. Some market participants were expecting that tariffs would raise $2 to $3 trillion in revenue over the next decade, which would be a significant contribution to deficit reduction.

We have always been more skeptical that tariffs would be a big part of the solution to restoring fiscal sustainability, in part because we doubted their political viability over the medium-term. The removal of IEEPA authority supports our conviction on that point. Under IEEPA, high tariffs would remain as the default case beyond President Trump’s term. Future presidents would have to take affirmative action to remove them. The new tariff regime authorized under Sections 232, 301 and 201 is more limited in scope and duration. These tariffs must be supported by findings of executive branch trade agencies, and most of them expire after four years unless extended. Under this new regime, we believe the default case is for tariffs to decline unless future administrations take affirmative action to extend them. If the American electorate continues to prioritize affordability, future administrations may be less willing to extend tariffs even if it means sacrificing revenue. The midterm elections will provide the first test of this hypothesis.