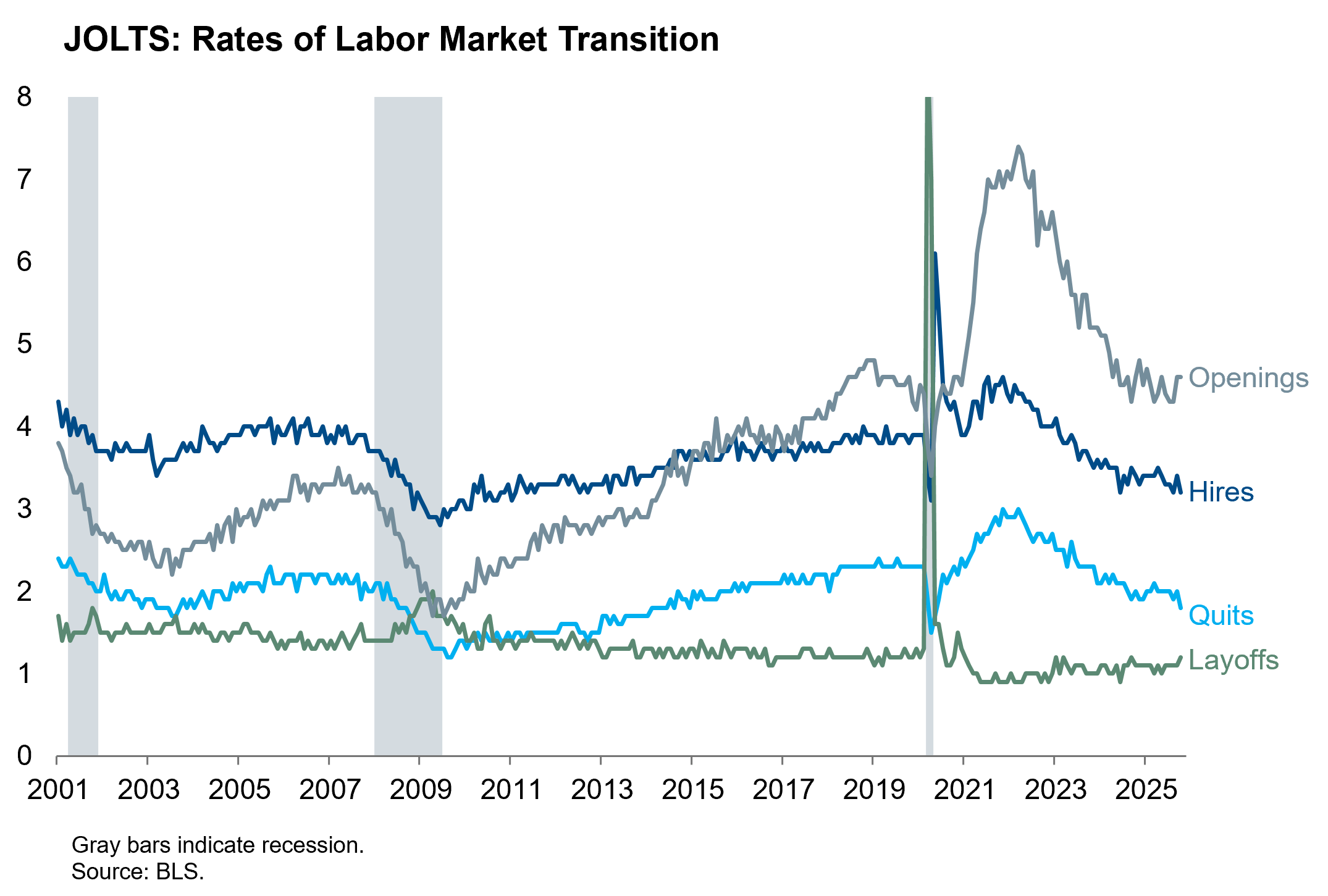

The BLS today released JOLTS data for September and October. These are the most recent high-quality labor market data we have received ahead of tomorrow’s FOMC decision. These latest JOLTS data continue to reflect a labor market that is soft but has not tipped over into a layoff cycle. The openings rate rose from August, but we think this is the least reliable measure in JOLTS. The hiring decision is when employers have to put their money on the line. The hires rate ticked up in September but then retraced in October to match the previous cycle low. The layoffs rate rose in October to match the previous cycle high. The layoffs rate remains low by historical standards, but regaining a cycle high on data that is now five weeks old will not dispel concerns raised by anecdotal reports in recent weeks.

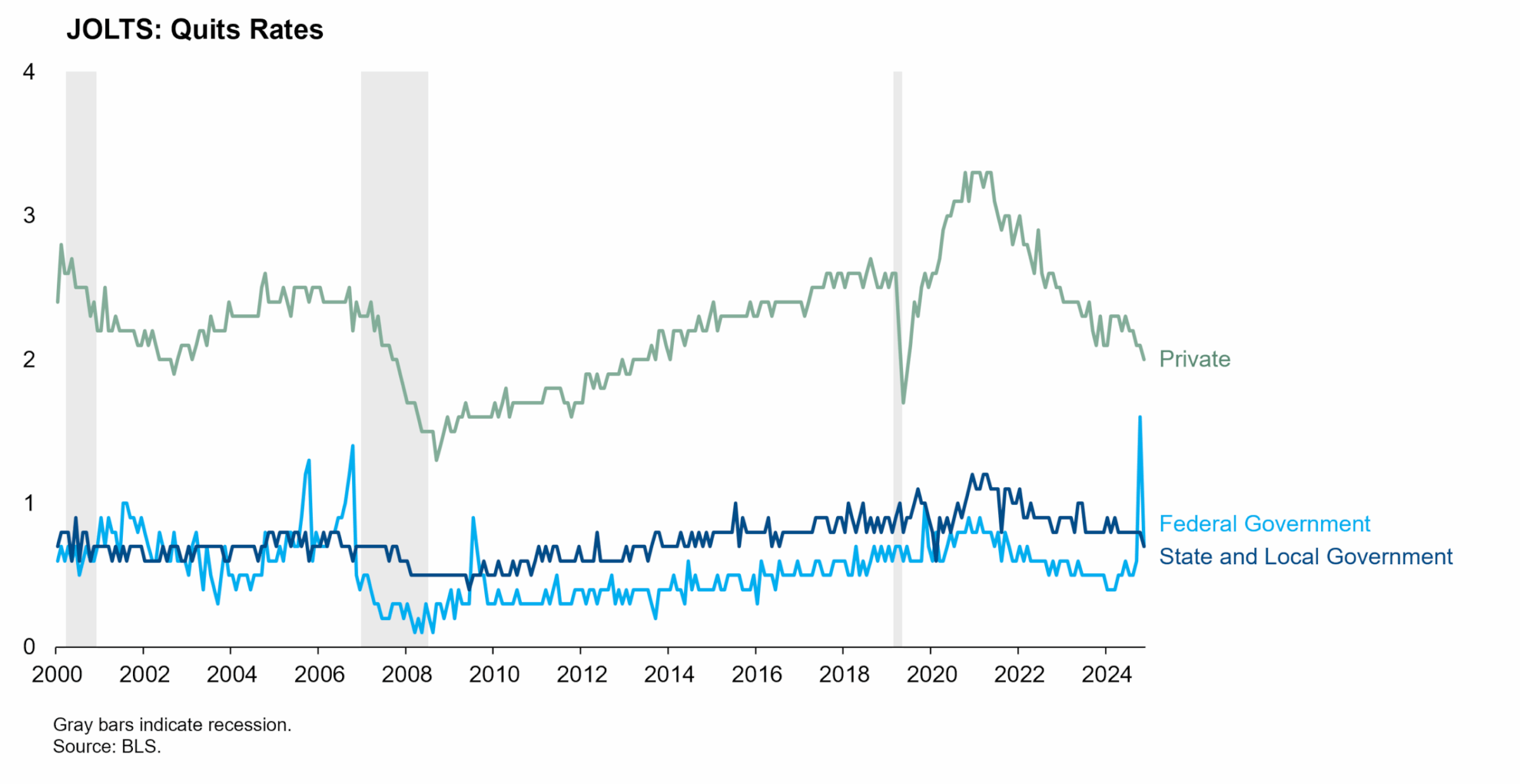

The quits rate slid further to a fresh cycle low, the only of these four headline measures that set a new post-pandemic extreme. The underlying components are worse than the headline figure. A low quits rate suggests elevated slack in the labor market, where employers are not poaching from their competitors and workers lack the confidence to try their luck on a job search. The headline quits rate was distorted in September and October by the deferred resignation program that was initially implemented by DOGE in the spring and took effect with a six-month deferral. This impact was widely anticipated.

As a result, the quits rate among federal employees spiked to an all-time high in September and only partially retraced in October. This is a real economic outcome, but it was a policy choice rather than an indication of the degree of cyclical slack in the broader labor market. The quits rate for state and local government employees fell to a cycle low in October. The private quits rate – which runs structurally higher in the more dynamic private sector – has exhibited a steeper cyclical decline in recent months. Private sector workers are voting with their feet and telling the Fed that the labor market remained slack through October even as the supply of immigrant labor has declined. Short rate markets are now pricing a 90% chance of a rate cut tomorrow, and the Fed won’t be willing to disappoint those expectations. While we wait for the delayed payrolls report next week, today’s JOLTS data reinforce the case for delivering that rate cut.