The May jobs report showed little change in the stable-but-vulnerable labor market dynamics we have highlighted in recent months. This report does not meaningfully change our outlook for the economy or monetary policy. We maintain our view that the first rate cut will not arrive until January 2026. We did not expect to see much impact from the trade policy shock in this report, and, in general, expect the inflationary impact of that shock to arrive sooner than the growth and labor market effects.

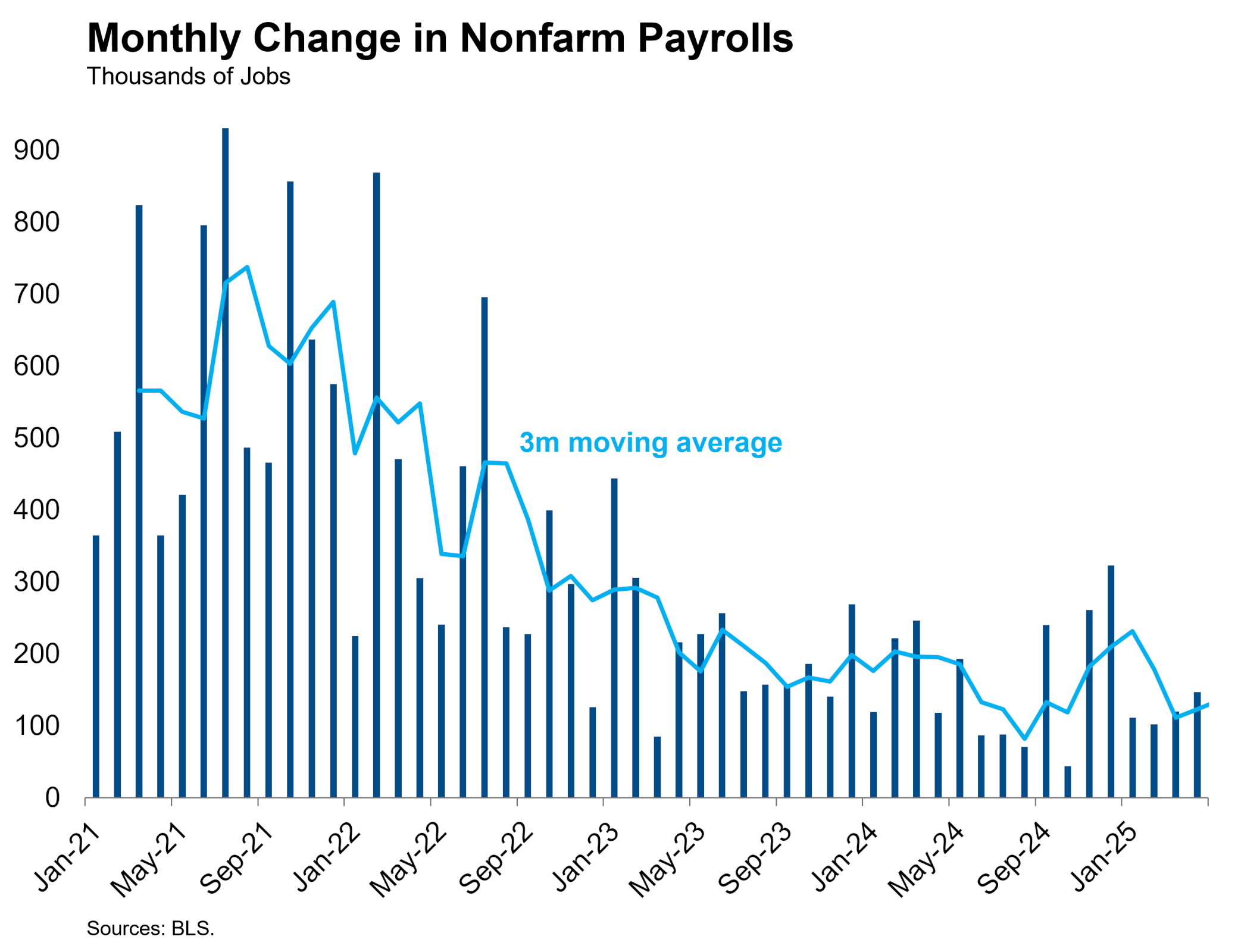

The establishment survey showed the U.S. economy creating 139,000 jobs in the month, which was slightly higher than expected, but the prior two months were revised lower by 95,000 jobs total. Diffusion was narrow — 90% of the job creation was in two sectors: Healthcare and Social Assistance, and Leisure and Hospitality. Federal government employment declined by 22,000 in the month, the fourth consecutive monthly decline since inauguration day. The monthly diffusion index declined from 51.8 to 50.0, showing that job growth was positive in half of the 250 industries tracked by the Bureau of Labor Statistics (BLS).

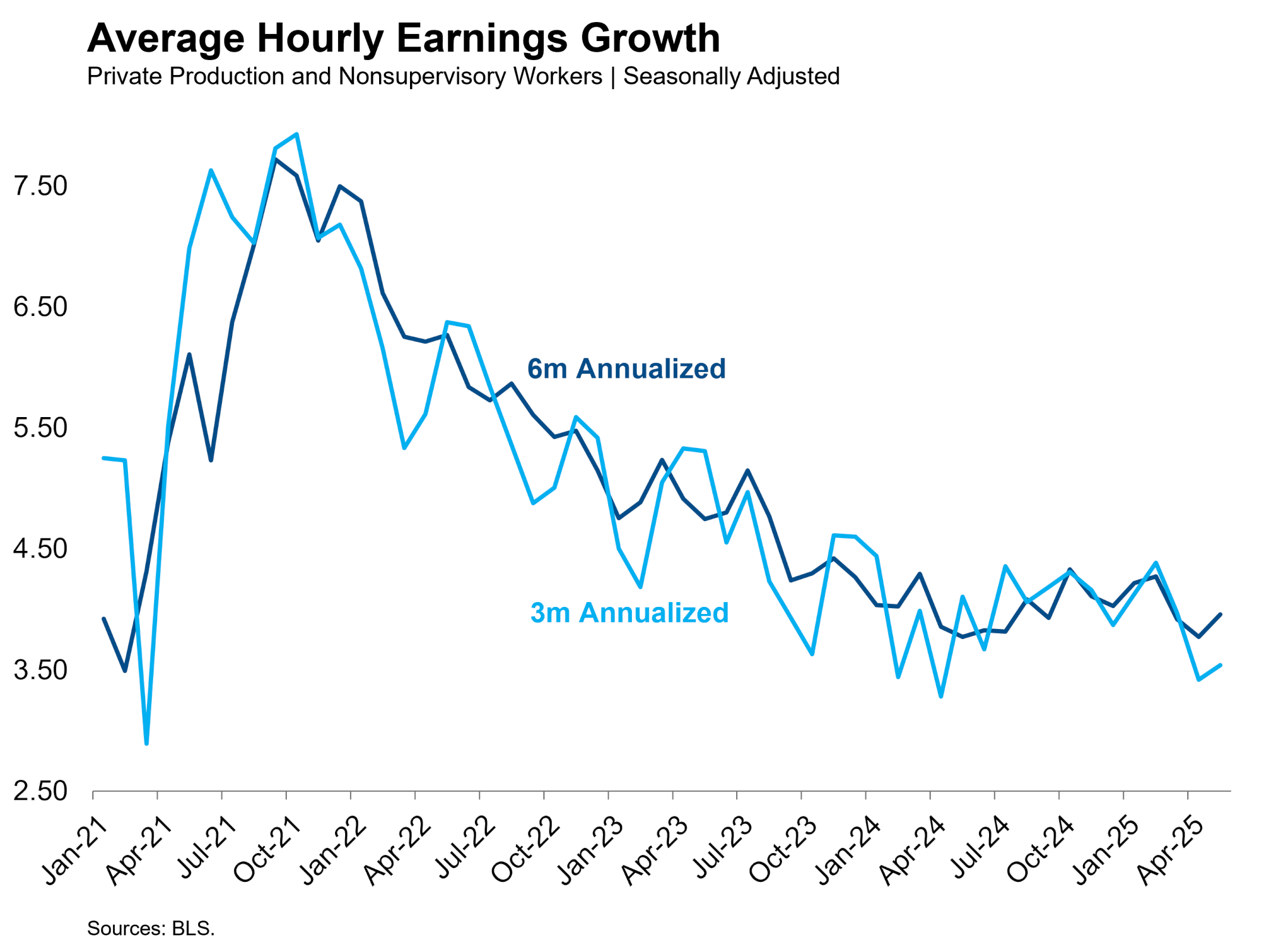

Average hourly earnings (AHE) increased by 0.4% in May, which was a bit hotter than expected. All of the acceleration in wage inflation came from goods-producing sectors, as services wage growth decelerated. The Fed will certainly be keeping an eye on wage inflation, but a single elevated month probably won’t cause them much concern. AHE is the noisiest of all the wage inflation measures, and lower frequency measures do not yet suggest a reacceleration. Remember that the Fed considers wage inflation in the 3.0-3.5% range consistent with their 2.0% price inflation objective, with expected productivity growth allowing for the difference.

The household survey showed much greater volatility and had some more concerning details. Within the household survey, employment declined by 696,000 in May. The 835,000 job difference between the two surveys is large but not unprecedented and is partly explained by methodological differences. Recall that the household survey uses a smaller sample size and therefore has wider error bands – this is the third month since January 2024 in which household survey employment declined by more than 500,000. Despite the large drop in employment, the unemployment rate increased by less than one tenth of a percent because the labor force declined by 625,000 workers in the month. That is the third largest monthly decline of this economic cycle and the ninth largest on record, excluding March-April 2020.

Immigrants accounted for 40% of that 625,000 decline in the labor force in May despite only representing 19% of the labor force. We are asking a lot of the household survey to track the monthly impact of reduced immigration. The BLS only surveys 60,000 households. Response rates have been in secular decline for years, and we expect them to decline even faster among immigrant households in the current environment. The statistical agencies are increasingly resource constrained. That said, this month’s results are consistent with our expectation that reduced immigration inflows will lead to a reduction in labor supply.

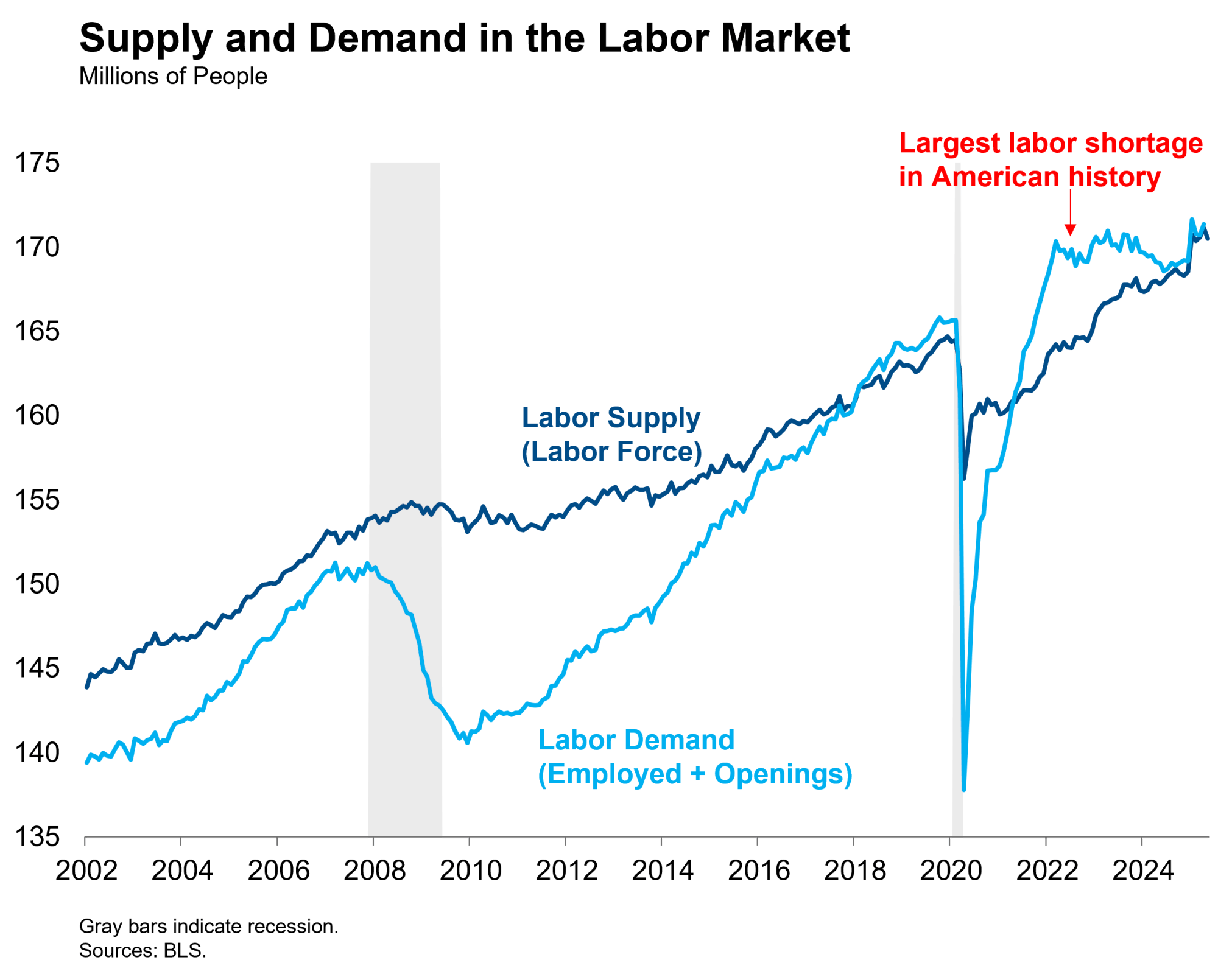

The Fed will be closely watching the balance of labor demand and supply for indications of reaccelerating wage pressure. The post-pandemic immigration surge, leaving aside its political and societal effects, did help resolve the largest labor shortage in American history and assisted the Fed’s pursuit of a soft landing. While we expect labor supply to continue softening in the quarters ahead, we do not expect a renewed imbalance in the labor market to reignite wage inflation. That’s because we expect labor demand to continue softening or at least remain subdued. If labor demand grows more quickly than we expect, employers may find a smaller pool of available workers and bid wages higher. Just like protectionist trade policy, reduced immigration is a negative supply shock that increases the risk of stagflation.