The April Employment Situation Report was stronger than expected but not unblemished. The U.S. economy created 115,000 jobs in the month. Government employment declined again, so private sector job creation was 123,000. Healthcare accounted for a bit less than half of total private job creation, still the strongest sector, but no longer as dominant as in prior years. Several topline industries saw net job losses in the month, including manufacturing, information and finance, but the diffusion index only declined slightly and remained above 50%. The three-month moving average of private nonfarm payroll growth clocked in at 55,000, which is low but comfortably above the near-zero estimates of breakeven job creation.

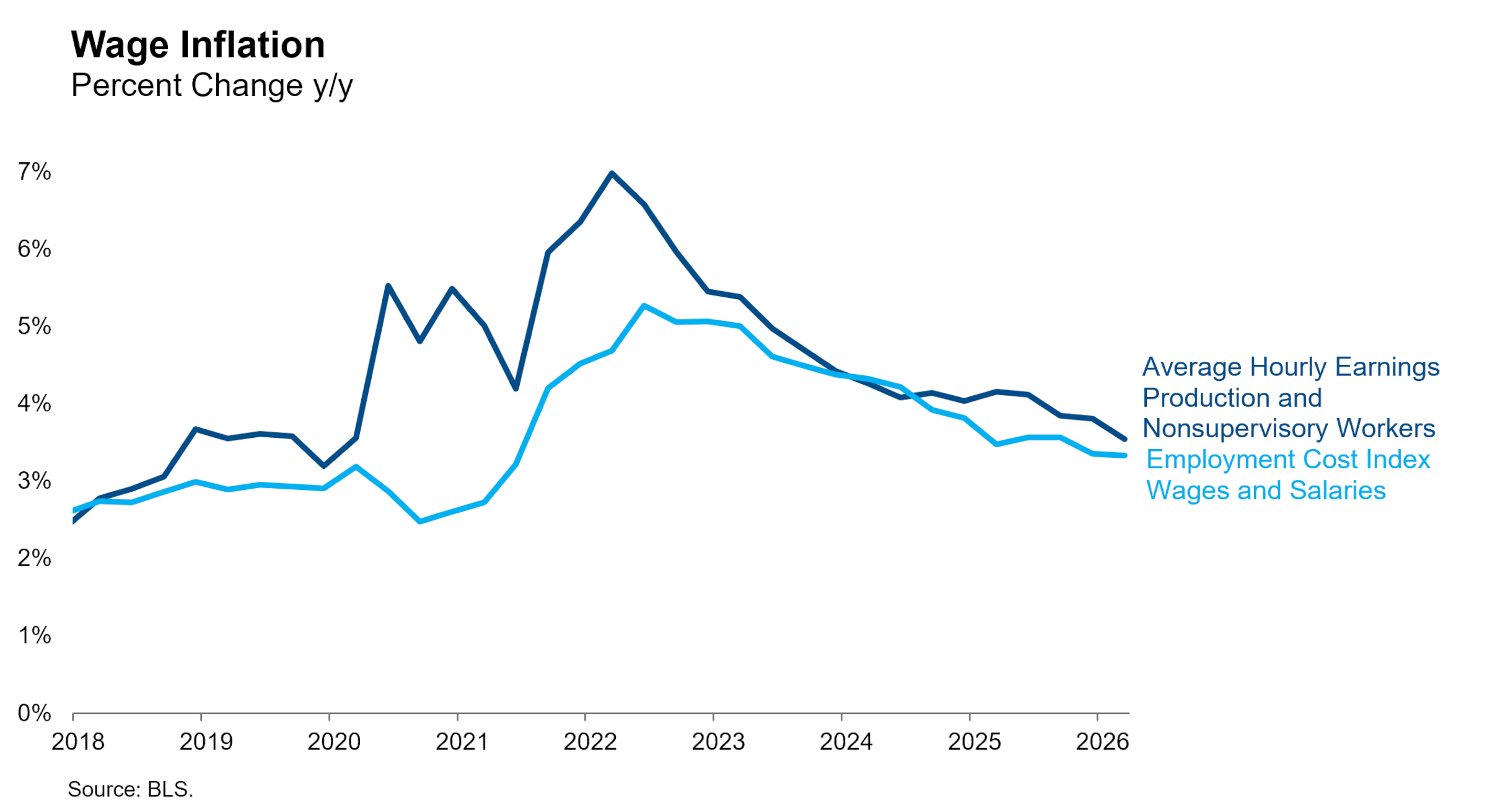

Average hourly earnings rose just 0.16% in April, continuing the trend of soft wage inflation. A better measure of average hourly earnings, the production and nonsupervisory worker figure, has risen 3.67% over the past year. Our favorite wage inflation measure, the wages and salaries component of the Employment Cost Index, is up 3.34% over the past year through March. Wage inflation around 3.5% is entirely consistent with 2% price inflation, given elevated productivity growth, and neither of these wage inflation measures shows any indication of upside acceleration.

The household survey was a bit weaker, but mostly on the supply side. Employment declined by 226,000, but the labor force contracted as well due to a decline in the participation rate. This caused the unemployment rate to rise by eight hundredths from 4.26% in March to 4.34% in April, though the officially reported measure rounded to 4.3% in both months.

Fed Impact

This report had something for both sides of the monetary policy debate. Hawks can point to +123,000 in private job creation, well above the breakeven level. There is little evidence that the labor market needs any further support from monetary policy, even in the midst of the Iran war. Doves can counter that the unemployment rate and wage inflation show no sign that the labor market is tightening in a manner that would introduce upside risk to the Fed’s inflation objectives. We think they are both right! The labor market appears to be in a holding pattern. The downside risk that motivated the insurance cuts last year has faded, but recent data suggest merely a stabilization rather than an acceleration that might complicate our disinflation outlook.

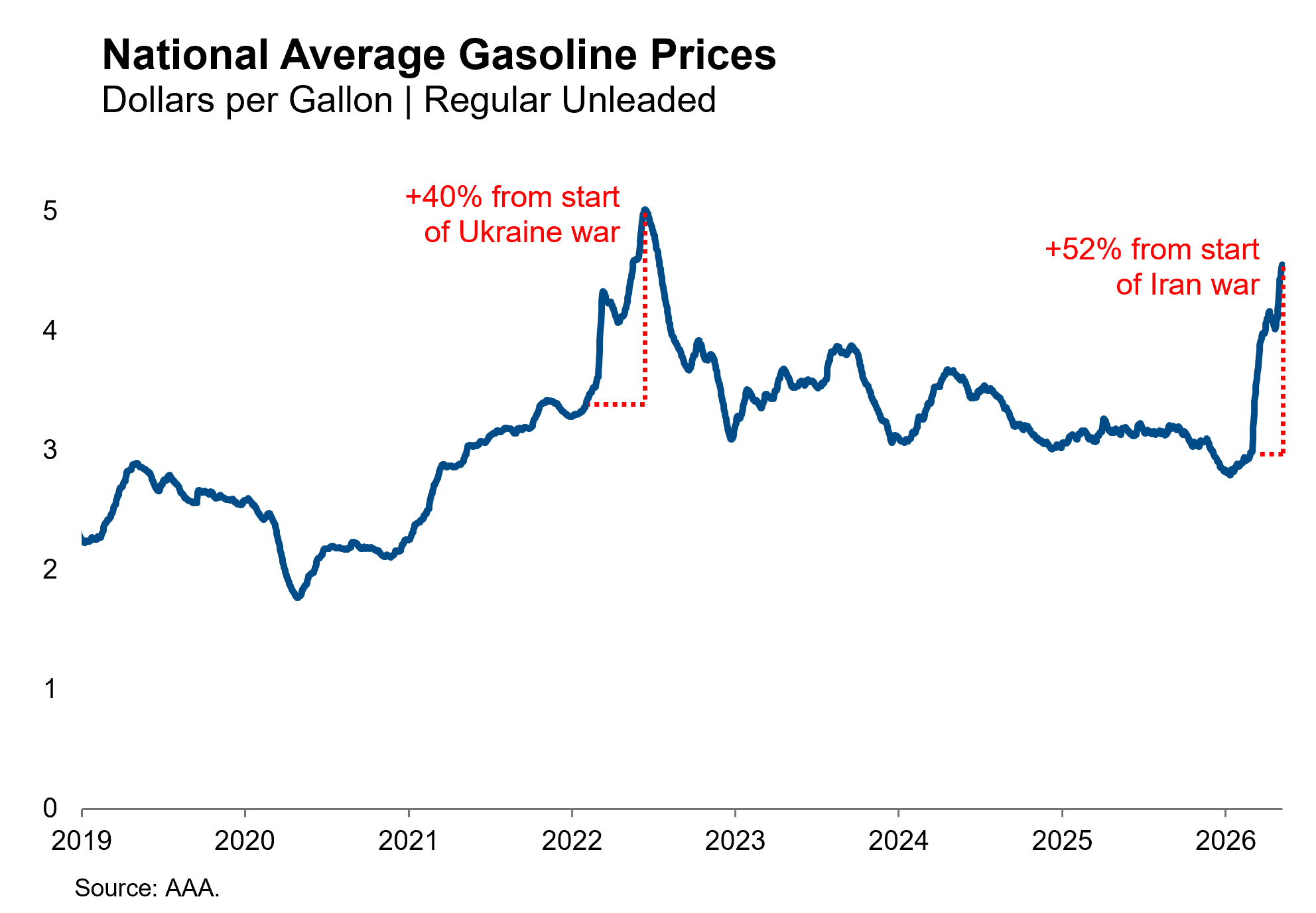

In response to that stabilization and the energy price shock from the war, the Fed’s focus has rightly shifted back to the inflation side of its mandate this year. While two-sided risks remain elevated, we continue to believe that the odds favor two to three rate cuts after the war is concluded. But first, we need to get past the war and the peak of energy prices. Then we can get back to regularly scheduled programming and confirm that the one-time price level increase from tariffs is complete. The former is the greater concern and the source of greater uncertainty. In percentage terms, the retail gasoline price shock since the start of the Iran war now exceeds the peak shock following the start of the Ukraine war.

We continue to believe that both conditions will ultimately be met and allow the Fed to resume easing, but not in time for the September cut we had previously expected. We push back our modal expectation for the first rate cut to December, primarily because the energy price shock has been larger and lasted longer than we had hoped. We expect the December cut to be followed by two additional cuts in March and June to a terminal range of 2.75-3.00%. As of this writing, short-rate markets are pricing no cuts over the next 12 months, so we see attractive valuations at the front end of the Treasury yield curve for those willing to bear the ongoing volatility of the war.