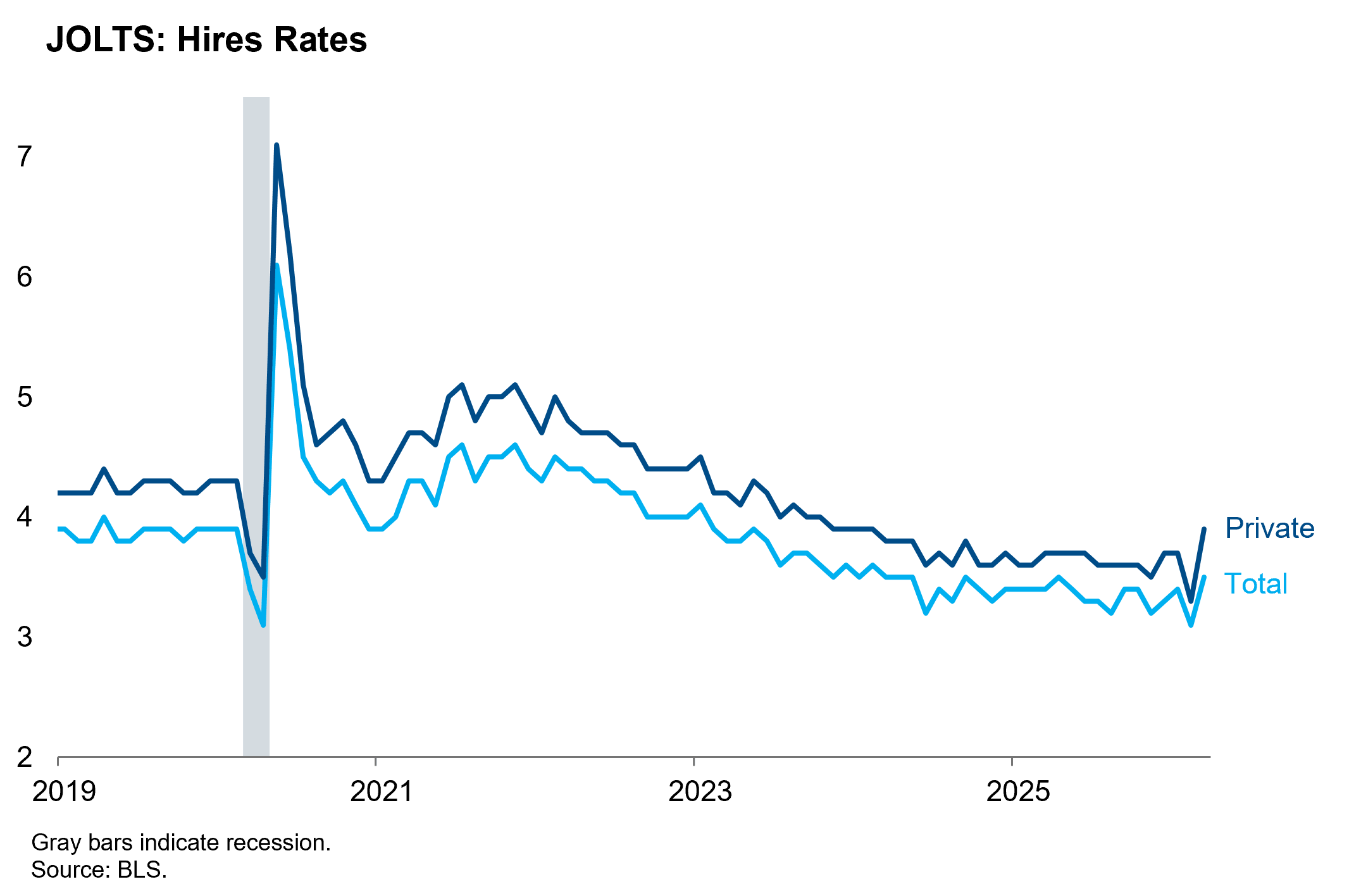

Hiring rebounded strongly in March, easing the concerns we had expressed about the low reading in February. The private sector hires rate rose from a cycle low to a two-year high. This volatility matches a similar pattern in nonfarm payroll growth, which swung from -133,000 in February to +178,000 in March.

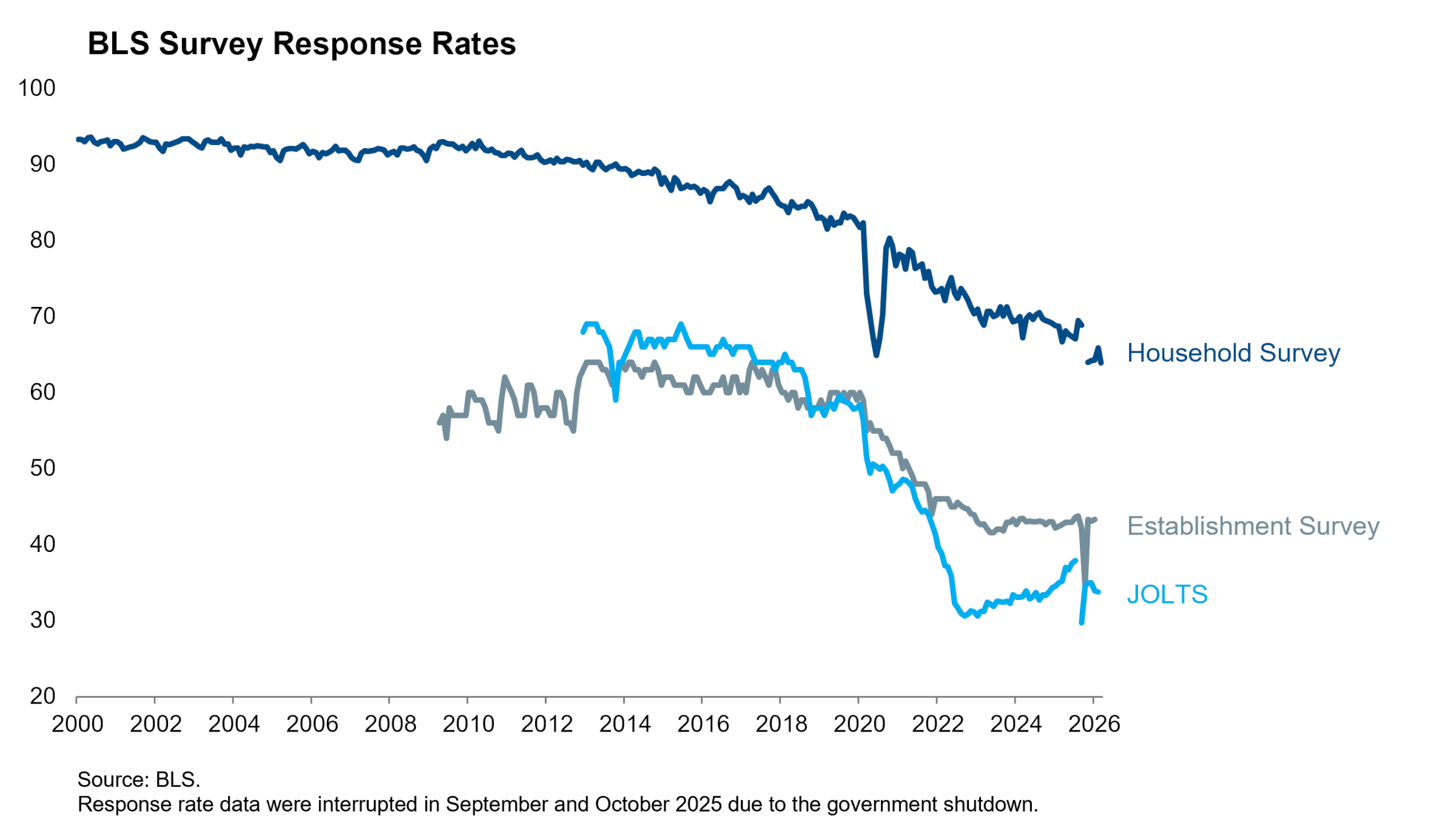

We’ll need the fog of war to clear before we can have conviction in the labor market outlook, but the two-month volatility in these data underscores another point of caution. The pandemic accelerated a decline in survey response rates that has confounded statistical agencies around the world for more than a decade. The response rate for JOLTS has fallen from a 66% average in 2012-14 to 34% average in the six months since the government shutdown ended.

The BLS is well aware of the problem and initiated a modernization plan in 2023 designed to increase response rates. Until those efforts bear fruit, economists and investors need to use caution when interpreting a single monthly reading in these data series. Lower response rates translate to smaller sample sizes, larger standard errors, and higher volatility in monthly results. The fog of both war uncertainty and data unreliability demand a higher bar of evidence before drawing labor market conclusions.