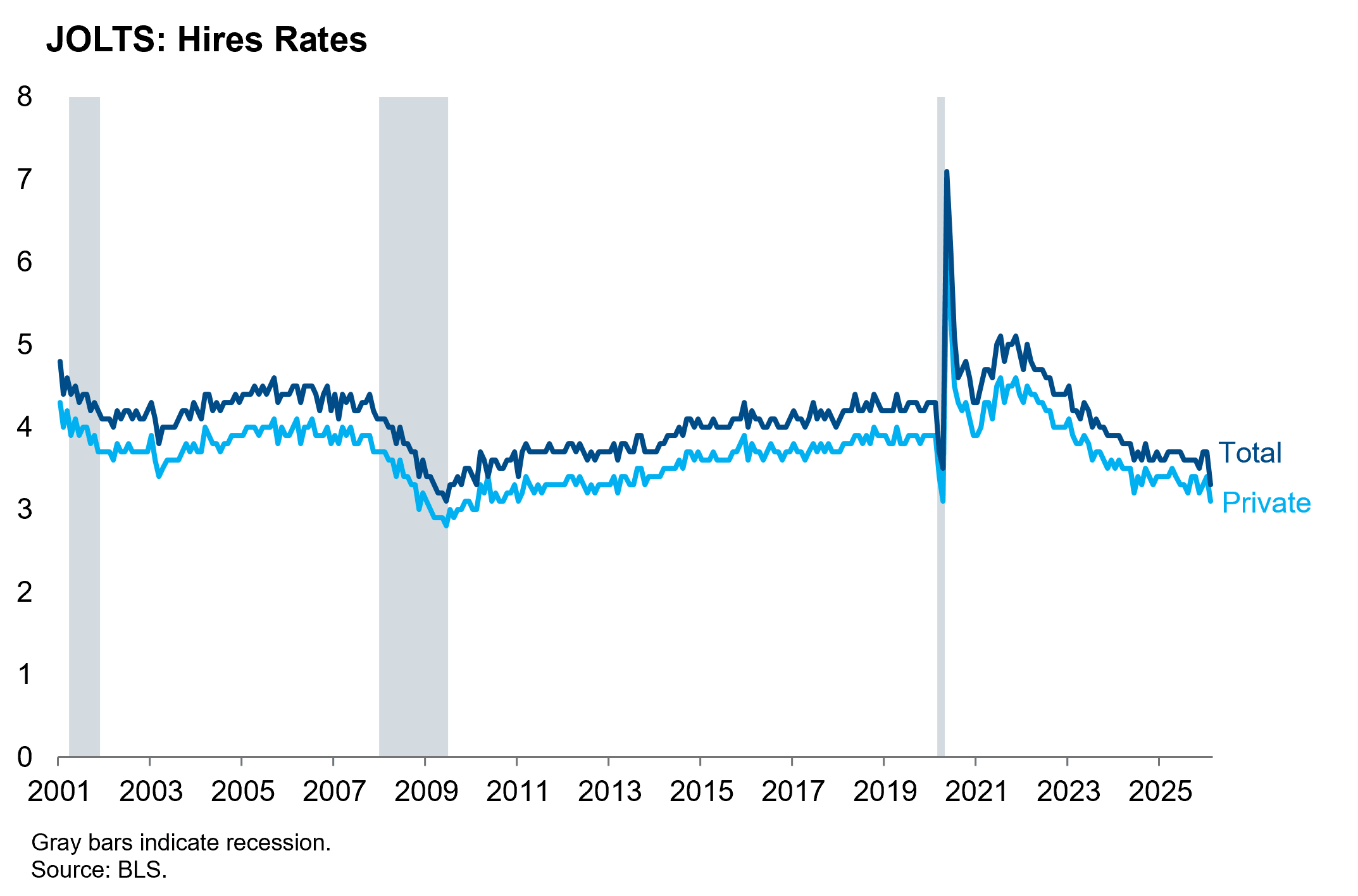

February JOLTS data show that the hires rate fell to a fresh cycle low ahead of the war. The total hires rate dropped three tenths to 3.1%, which matches the pandemic low. The private sector hires rate, which tends to be a better cyclical indicator because it excludes the very stable government hires rate, fell four tenths to 3.3%, which is the lowest reading since February 2010.

This is a troubling sign of the state of the labor market heading into the war. Central to our thesis that the economy was back on track towards a soft landing was that fading trade policy uncertainty and rising business confidence would at least stabilize labor demand, if not cause a rebound. A continued decline in the hires rate would cause us to question that thesis. The war will likely reduce business confidence and labor demand, at least temporarily. Even if the war is short enough that we are able to return approximately to the status quo ante of the labor market, the Fed may feel the need to deliver a few more rate cuts to support employment.

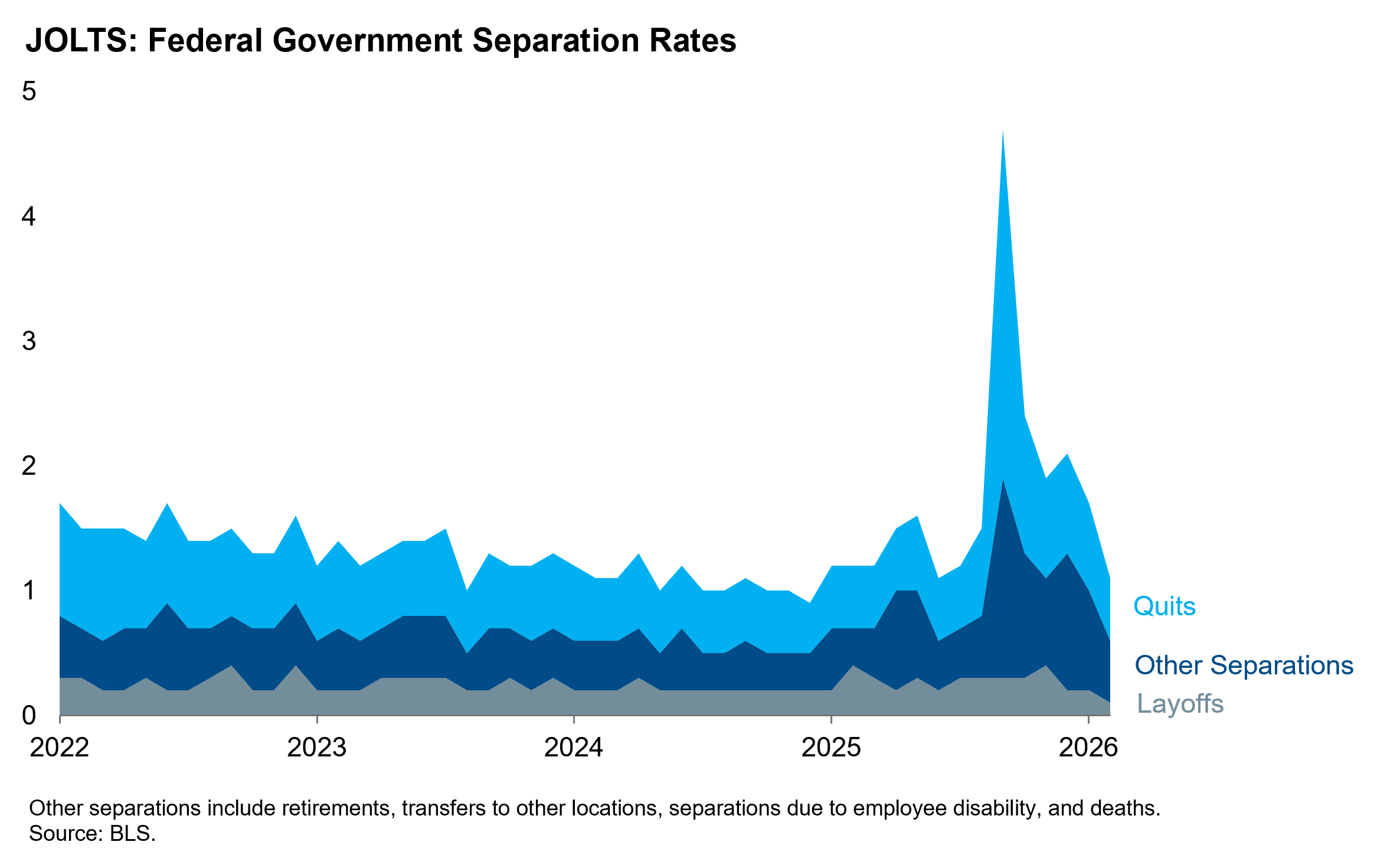

The JOLTS data also show that the DOGE effect, which reduced federal payrolls by 327,000 since inauguration day, has largely passed. The federal government separation rate has normalized to within a tenth of the 2024 average after rising to an all-time high (excluding decennial census-taking flows) in September. The workforce reduction was achieved almost entirely through voluntary quits and retirements, as the layoff rate remained relatively stable throughout 2025. This is the third largest federal workforce reduction in percentage terms of the postwar era (behind the Clinton and Eisenhower administrations), a meaningful change that will nevertheless have limited effect on the deficit, as payroll represents just 6-7% of the federal budget.