The results of the March FOMC meeting were mostly as expected. The policy rate was left unchanged by an 11-1 vote with the lone dissent from Governor Miran. The median dots for 2026 and 2027 were unchanged. Powell fielded many questions about the energy price shock but expressed the appropriate lack of conviction about the future course of the war. Powell reiterated the pre-war reaction function where the conclusion of tariff inflation passthrough would allow for a couple more cuts into firmly neutral territory. It’s true that the energy price shock could delay or complicate the implementation of that reaction function, but it’s just not possible for a central bank to have any conviction about the magnitude and duration of the shock. The Fed is in the fortunate position of being on hold for an extended period anyway, in contrast to some other central banks, so they have the luxury of waiting to see how the war plays out.

Though the 2026 median dot was unchanged, the revisions since December leaned slightly hawkish. Three participants who had offered soft dissents at the December meeting lowered their dots to 3.5625. This was just a marking-to-market and not a change in their policy stance. Three other 2026 dots were raised 25 bps and one (presumably Governor Miran) was raised 50 bps. The 2026 average increased very slightly, but would have risen by more if we threw out the three mark-to-market reductions. The slightly hawkish revisions to the dots are attributable both to a stronger growth and employment outlook as well as the impact of the energy price shock.

Market participants keyed on Powell’s answer that the Committee had discussed the possibility that the next move might be a rate hike, just as they had at the January meeting. This comment led to a 7-bp intraday increase in the 2y Treasury yield and contributed to the bear flattening in the curve today. Though Powell reiterated that “the vast majority” of the Committee did not expect a hike, a vocal minority clearly wants to keep that option on the table. Chairman Warsh will have his hands full balancing this wing of the FOMC against President Trump’s desire for lower rates.

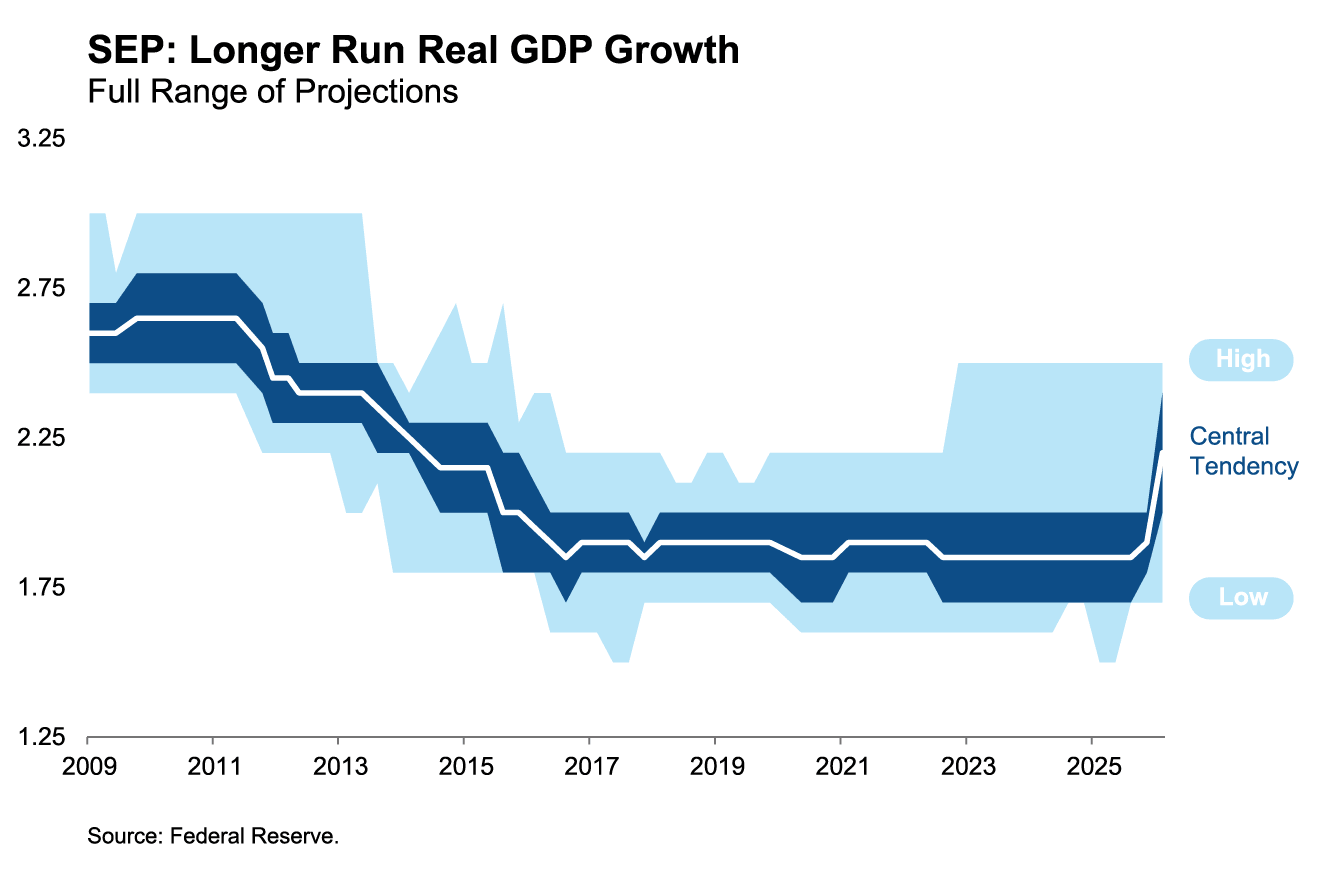

Aside from the near-term path, our other big takeaway from today’s events was the supply side optimism expressed in the Summary of Economic Projections (SEP). Many participants’ estimates of longer-run GDP growth rose to their highest levels since 2013. While these revisions are partly an acknowledgment that productivity growth has remained at 2% or higher for the past nine quarters, it also seems that the Fed is buying into the AI productivity hype. Fixed income investors should be mindful that higher productivity growth will eventually lead to a higher neutral policy rate, all else equal.

Finally, Powell read some prepared remarks stating that he has “no intention of leaving the Board until the investigation is well and truly over with transparency and finality.” Senator Tillis also reaffirmed his position this morning, that he will not advance Warsh’s nomination until the investigation is resolved. At this point, it seems that the conclusion of that investigation is a necessary condition both for the confirmation of Warsh and the opening of Powell’s Governor seat for another appointment by President Trump.