The war in Iran will have significant impacts on the combatants involved, the people in the region, and global geopolitics. The impact on the U.S. economy, however, will be limited under most scenarios other than the tail risk of a wider conflagration. Defense spending will increase to replace munitions used in the attack, which will further strain our fiscal capacity. The global oil market might be disrupted by the loss of Iranian production, but the vast majority of Iranian oil exports go to China, so the supply disruption would be felt most acutely there. U.S. oil production may increase as a result of higher prices or moral suasion by the Trump administration.

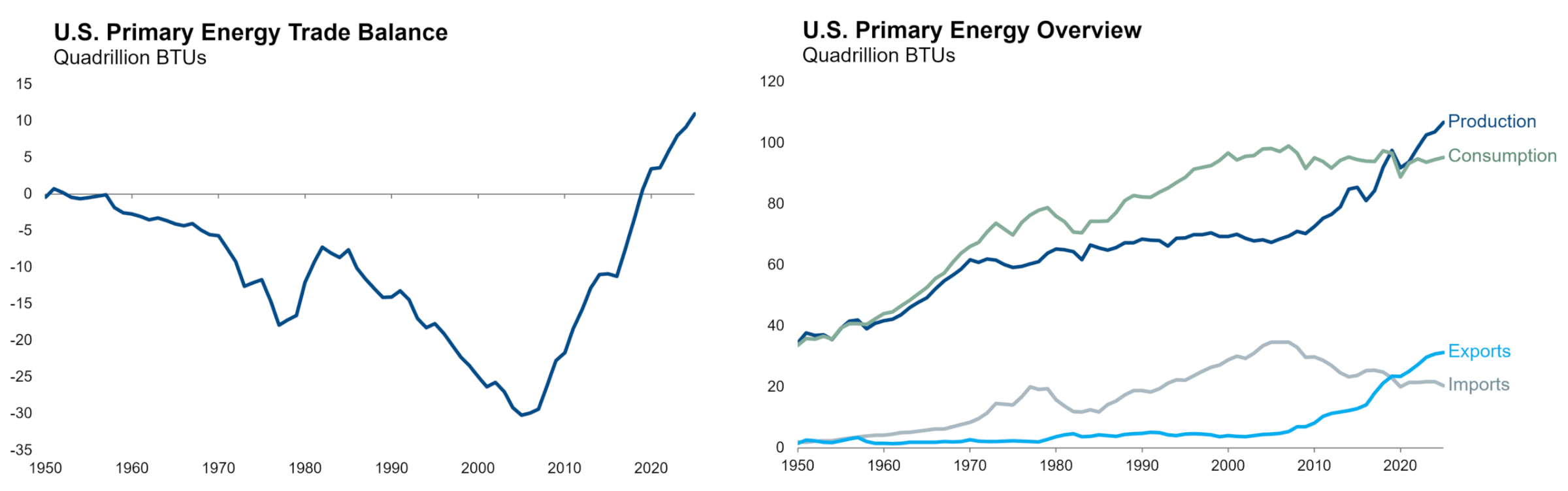

Readers of a certain age will recall that the primary transmission channel to the U.S. economy from the Middle East conflicts of the 1970s through the 2000s was the stagflationary impulse from oil price shocks. That old framework no longer applies in the era of U.S. energy independence. The shale revolution has led to a 55% increase in U.S. energy production in the last 20 years and allowed the U.S. to become a net energy exporter since 2019. The charts below include energy from all sources, but fossil fuels account for nearly all of America’s foreign trade in energy.

Source: U.S. Energy Information Administration

Assuming the tail risks of this war are avoided, it does not significantly change our outlook for the U.S. economy or monetary policy. We have been a bit surprised at the magnitude of the increase in Treasury yields today, but we think there are several confounding factors. A $5-$8 increase in oil prices, if sustained, will translate to slightly higher energy inflation and should cause TIPS breakeven inflation rates to increase by a few basis points. Most of the increase in nominal Treasury yields today is explained by higher real yields, consistent with the typical beta between TIPS and nominals. The higher defense spending needs must compete with all the other demands on U.S. tax revenue (mostly entitlements and interest expense these days), so it’s possible that the fiscal risk premium increased slightly.

But it’s also worth noting that the outbreak of war arrives after a 30-bp rally in the 10-year yield in February, and perfectly coincides with the month-end turn that often sees selling pressure on the first of the month. Separately, about one-third of the increase in yields arrived after the mid-morning stronger-than-expected ISM manufacturing print, which suggested continued resilience and inflationary pressure in the goods economy. While we always want to see Treasuries rally in a flight-to-quality environment, we would note that risk assets and gold have retraced all or nearly all of their initial price response. One thing we do not see is evidence of a “sell America” dynamic. The rise in Treasury yields today has been largely synchronized with foreign advanced economy government bond markets. And the dollar has continued to appreciate against major currencies throughout Sunday and Monday. We will continue to monitor the asset price response to the ongoing conflict, but we continue to expect limited impact on the U.S. economy under most scenarios.