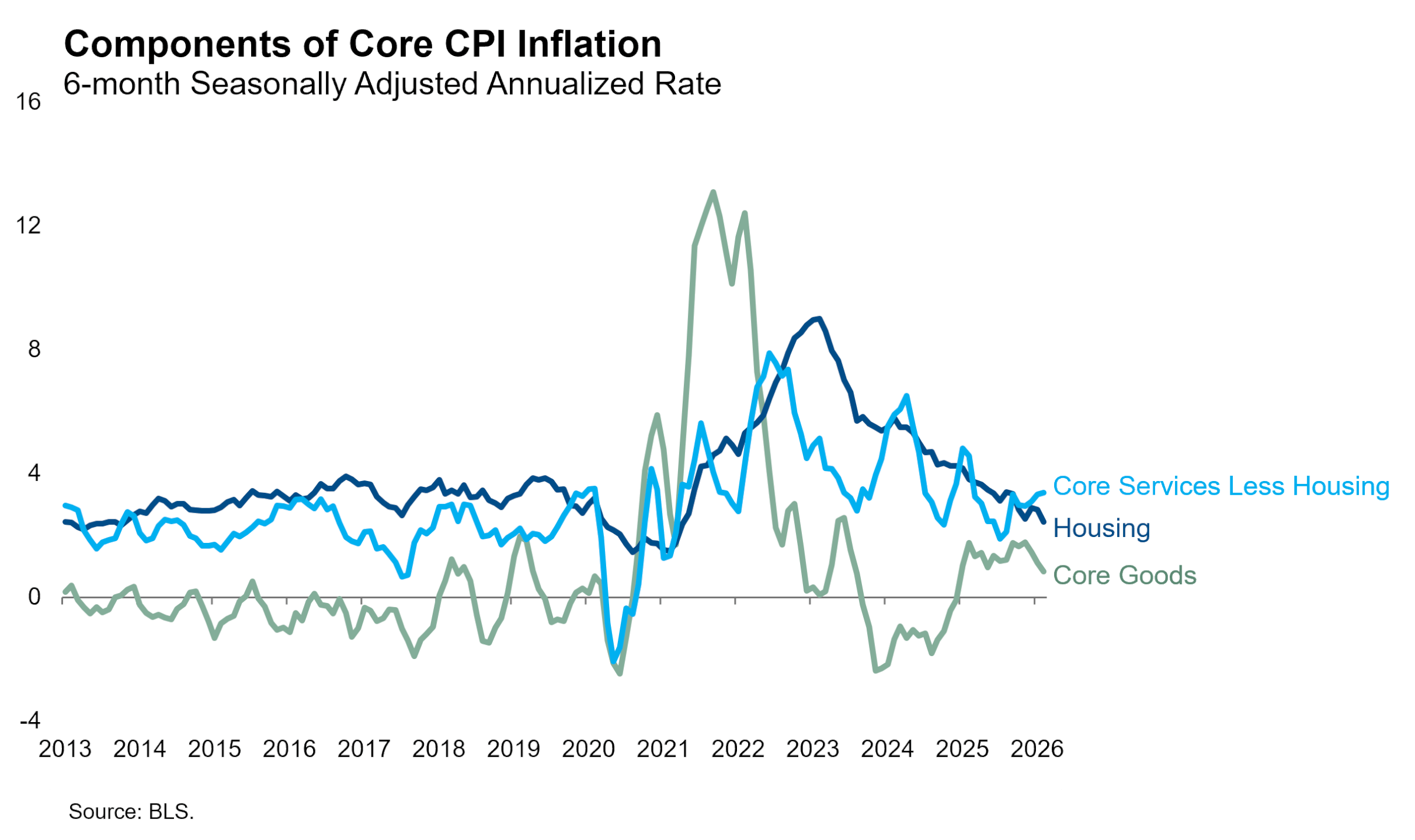

Core CPI increased at an annualized rate of 2.62% in February, in line with consensus expectations and nearly a full percentage point below January’s pace. Housing inflation continued to decelerate, reaching the lowest monthly pace of the cycle, 2.26% annualized. Core goods prices rose at an annualized rate of 0.98% in February. Core goods inflation has accelerated slightly in each of the three months since the shutdown distortions, but is still running at less than half of the Q3 pace. We remain optimistic that the last remnants of tariff-induced goods inflation will pass through in the next few months.

Non-housing services inflation remained elevated at a 4.29% annualized rate. This component has exhibited higher volatility than those other two categories, so we don’t think it will cause serious concern for the Fed at the moment. Labor is a higher share of production costs in the services industry than in the goods industry, and it appears unlikely that the labor market is on the verge of tightening enough to re-ignite concerns about a wage-price spiral. That said, hawks like President Goolsbee will want to see non-housing services inflation decelerate meaningfully before they’ll agree to resume cutting rates.

These are the inflation dynamics the Fed has been watching since the government shutdown, which canceled the CPI release for October and heavily distorted the November release. The Fed must also now assess the economic impact of the war that began on the last day of February. We figure they’ll have several months to let the dust settle. We believe the Fed is firmly on hold for the next two meetings, and likely for the following two meetings in June and July as well. Today’s print appears consistent with this outlook for disinflation later this year and does not change our outlook for the path of monetary policy in 2026.

Based on the energy price movements we have seen so far, the stagflationary shock from the war would not be large enough to change our modal expectations for the U.S. economy or monetary policy. But the war clearly increases the upside risk to headline inflation through energy and food prices, and that uncertainty will linger as long as the war continues.