With an average funded status of 107% and over 50% seeing a surplus, corporate defined benefit (DB) plans enter 2026 as well-funded as they have been since before the Great Financial Crisis of 2008.[1] For many plan sponsors, the strategic focus has shifted from designing glidepaths to designing strategies that seek to grow the surplus. Given this evolution, we thought this is an appropriate time to reflect on the benefits of having a plan surplus both now and in the future.

Additional Surplus

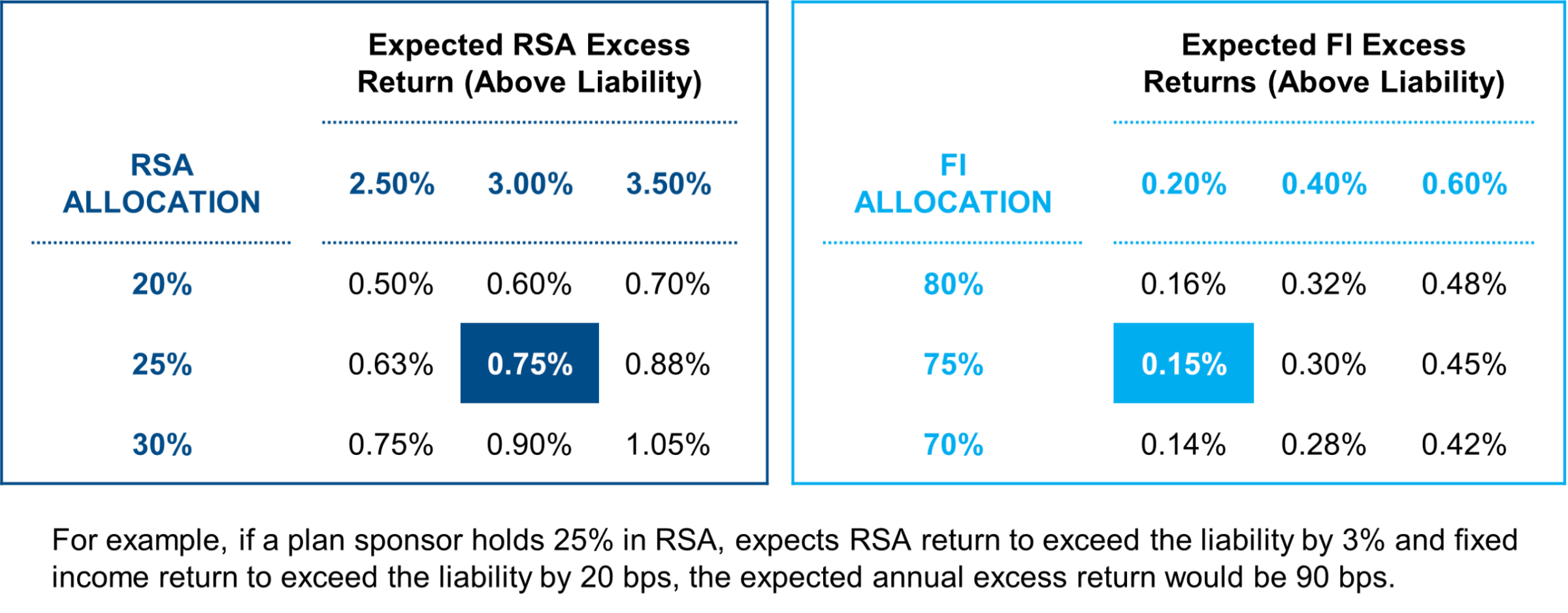

A fully funded DB pension offers the sponsor the ability to potentially out-earn the liability’s return while still accepting only a modest amount of funded status volatility. As documented in a previous NISA Perspectives post, Your Pension: More Than a Liability, a fully funded plan with a risk-controlled asset allocation with 70-80% allocated to LDI strategies could be expected to out-earn the liability by 50-100 bps with an annual tracking error of 3-4%.[2] The return by which a plan out-earns the liability will be a function of the asset allocation, return-seeking asset (RSA) excess returns and fixed income (FI) manager alpha. Figure 1 provides a simplified table of excess return and alpha expectations for different asset allocations.

Figure 1

The callout above shows an annual expected excess return of 90 bps, which may not feel like much, but for a 10-duration liability, that suggests 9% additional surplus over the life of the plan.

Importantly, any actions taken by plan sponsors to reduce the size of the liability (PRT, lump sum offerings, etc.) reduce the dollars of surplus that can be generated. A $1b plan that earns 90 bps of excess return will grow the surplus by $9mm annually, but a $500mm plan will only grow the surplus by $4.5mm. In the Midwest, we call that “selling your seed corn,” as sponsors are sacrificing long-term surplus growth for short-term considerations.

The story is even more compelling for over-funded plans as the surplus compounds on itself. A 5% over-funded plan that has an expected return on assets of 6% will be expected to out-earn the liability by an additional 30 bps (5% x 6%) on top of the estimates from the table above. A 10% surplus would be an additional 60 bps of annual excess returns.

Furthermore, when plans are greater than 5% over-funded, a natural question to ask is whether re-risking a modest amount is appropriate. Naturally, a larger return-seeking allocation would have a higher expected return and allow for even larger expected surplus growth.

Is “Trapped Surplus” Really Trapped

Unless a plan sponsor can use the surplus in some way, does it make sense to take additional risk trying to grow the surplus? The thought process is that if a plan sponsor can’t access the surplus, it is of no real use. To be sure, it is still true that a dollar of deficit feels more painful than a dollar of surplus feels beneficial, but that difference has decreased as funding requirements for deficits have been relaxed and greater latitude has been granted for surplus use. Below, we will outline potential surplus use cases for plan sponsors.

Continuation of Ongoing Service

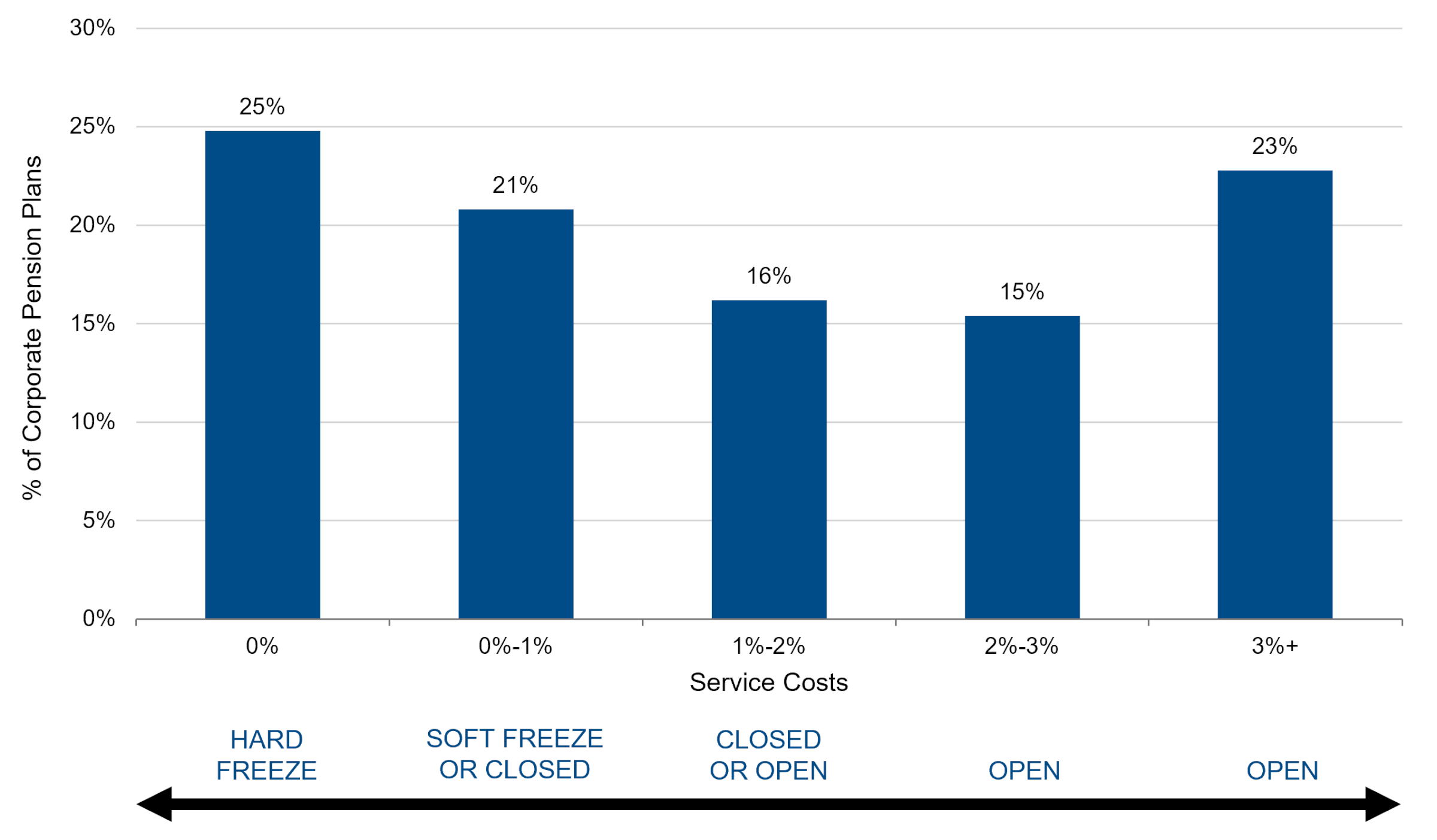

We estimate that over 50% of the 500 largest DB plans have annual service costs that exceed 1% of their pension liability, and only 25% of plans are fully frozen (i.e., 0% service costs). Figure 2 below reflects service costs as a percentage of the liability for the 500 largest corporate defined benefit pension plans based on Form 5500 data as of 2024.

Figure 2

For any plan still accruing service, and certainly for plans accruing service of 1% or more annually, a larger surplus can directly offset future service costs. For closed but accruing plans, a larger surplus reduces the need to do a “hard freeze” that risks upsetting existing employees.

For plans with ongoing service, we suggest they evaluate their funded status against the expected benefit obligation (EBO) version of their cash flows rather than the more traditional projected benefit obligation (PBO). The EBO includes all expected future benefits for existing participants, including salary increases and future years of service. This measure of the liability can help design glidepaths and attain an understanding of how much surplus could be consumed by future benefit growth. This can indicate how much remains for other use cases outlined below.

Reopening

Reopening a plan provides another way to utilize the surplus. When reopening a plan, the design can be constructed to avoid some of the common pitfalls (i.e., overly generous crediting rates) that have plagued plans in the past. Most readers are likely aware that IBM reopened their plan in 2023, but NISA is aware of at least four others that have reopened or created new plans in the past few years. We don’t know if we can call this a trend quite yet, but we like the direction that it’s heading.

When reopening a plan, sponsors can choose to change the DC benefits they offer to participants. When IBM reopened their plan, they turned off a similarly sized defined contribution (DC) match, thus saving the sponsor the required cash contributions that need to be made year after year in DC plans. As proponents of DB in general, we believe the flexibility of DB contributions compared to the rigidity of DC contributions is often an overlooked consideration.

A reopening of DB with no change in DC matches would certainly benefit the participants, but presumably, there would be significant goodwill from employees for such an action. And likely there could be a hybrid approach where DC contributions are pared back while participants receive a larger dollar DB benefit, thus benefiting both participants and the sponsor. It can be a win-win situation.

For any plan sponsors seeking additional goodwill from participants or perhaps as part of union negotiations, one-time cost of living adjustments are also a potential use of surplus.

Mergers and Acquisitions

When a company with an over-funded pension plan merges with a company that has an under-funded pension plan, the two plans may be merged to improve the funded status of the under-funded plan.

Workforce Management

Plan assets could be used as both a retention and a severance tool for existing employees. For example, highly valued employees could be offered an increase in service credits. This would be disproportionately valued by older employees. Likewise, to encourage early retirement, additional benefits contingent on accepting an early retirement could be offered.

Transfer to Retiree Medical Benefits

The SECURE 2.0 Act was passed in December 2022, making it significantly easier to transfer assets from your pension plan to a 401(h) account. The funded status necessary to transfer assets was reduced from 120-125% to 110% and a maximum of 1.75% can be transferred in any given year. There are further requirements that must be met to transfer assets, and many of them are outlined in a previous Perspectives piece, Funding Post-Retirement Benefits Made Easier Under SECURE 2.0.

401(k) Contributions?

In what could be a potential game-changer for DB plans, proposed legislation would allow sponsors to transfer surplus in excess of 110% to DC plans. The Strengthening Benefit Plans Act of 2025 (Strengthening Benefit Plans Act of 2025) was introduced in June 2025 and has been referred to the Committee on Finance. While we would have preferred immediate action and approval of this bill, we do believe that eventually some form of this proposal will be approved. A key reason is that reducing the amount of DC contributions from corporate cash accounts, all else equal, increases the tax base for the federal government.

Under the proposed law, there are multiple conditions that must be met, but the most consequential one is that the plan must be 110% funded on the PBGC basis (the same calculations that are used in PBGC variable rate premium calculations). Other requirements include that the DC plan must include at least 95% of active DB participants (i.e., be a qualified replacement plan or QRP) and total DC benefits provided cannot be reduced for five years, including the current year of transfer.

Putting it All Together

Being an over-funded DB plan is an enviable situation for many plan sponsors. These sponsors have an asset that they can reasonably expect to out-earn the liability with only a modest amount of volatility, and the earnings grow on a tax-deferred basis.

For those DB plans that can become over-funded to 110% or more, it’s not hard to imagine a risk-controlled allocation that consists of 70-80% in LDI, targeting a 100% hedge of the interest rate risk of the liability and has an expected excess return above the liability of 1.5-2.0% annually. One can envision a world where every year the additional surplus earned is transferred to 401(h) and/or 401(k) assets, thus saving the plan sponsor a significant amount of annual cash on the barrelhead.

The pension plan should be viewed more as an asset than a liability, with the multitude of uses for future surplus growth. Even if there isn’t perfect foresight into what surplus use could be chosen, maintaining the pension maintains the option for value in future surplus growth.

[1] Funded status is estimated as of 12/31/2025 from NISA’s PSRX. The PSRX is a forward-looking estimate of the funded status volatility of U.S. corporate defined benefit pension plans. For more information on the PSRX, go to: https://www.nisa.com/psrx/.

[2] Data as of 12/31/2025. Return-seeking assets assumed to be 100% MSCI ACWI. Fixed income allocation assumed to be a blend of credit and Treasuries targeting a 100% hedge of the liability. Illustrative cash flows have a 10-duration and are discounted using the FTSE AA Curve. Historical return-seeking volatilities use one-year at-the-money (ATM) implied S&P 500 Index options volatilities. Correlation estimates use five years of monthly data. Historical interest rate volatilities use ATM option-implied volatilities on Treasury bonds and interest rate swaps. Historical credit spread volatilities are calculated by scaling historical volatilities by the prevailing spread level.