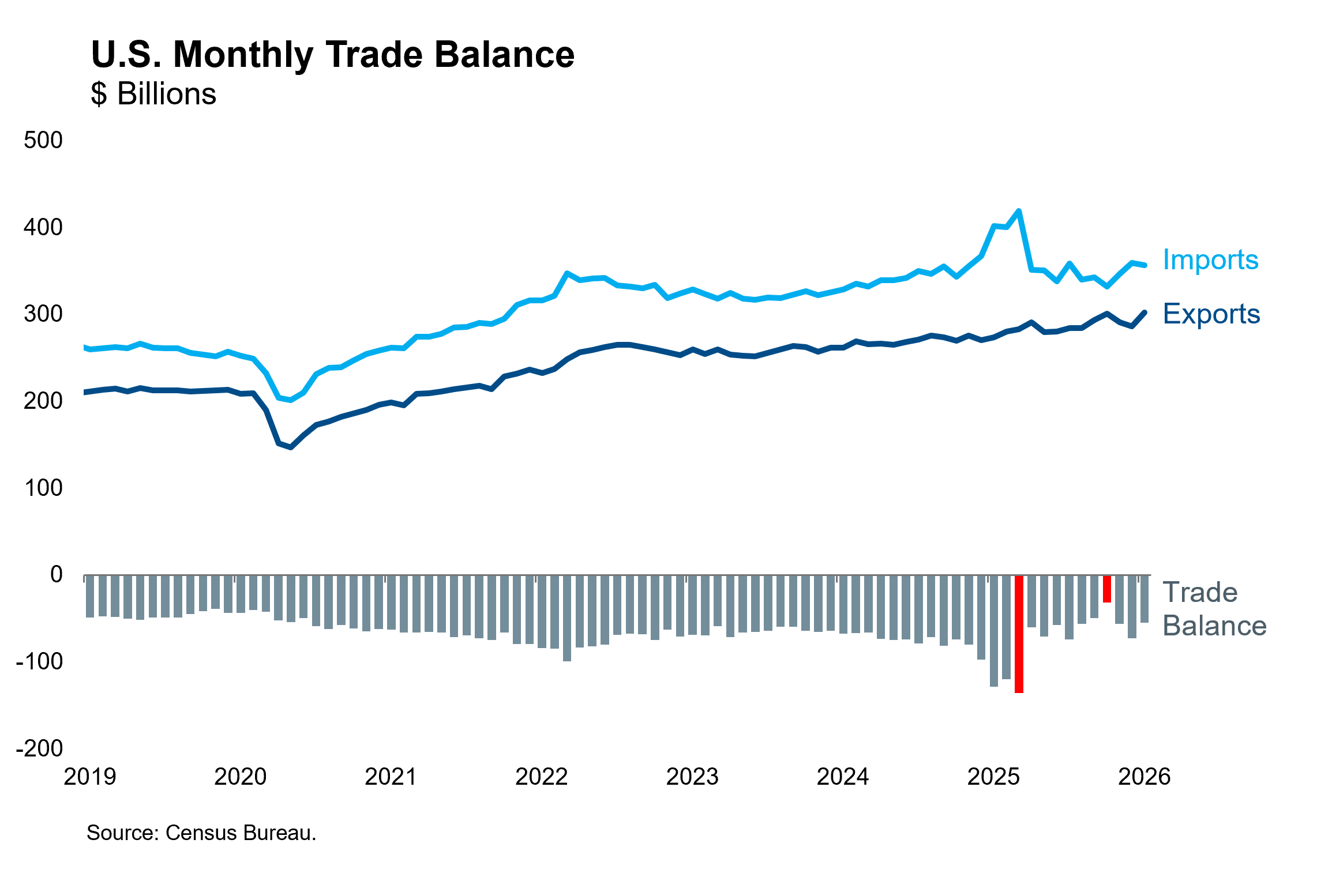

Last year’s historic increase in tariffs, and the shock of uncertainty surrounding their implementation, have roiled America’s foreign trade flows. The monthly trade balance swung from an all-time low to a 14-year high within eight months in 2025 (highlighted in red in the chart below). The initial impact was a surge in imports between the 2024 election and March 2025, as importers rushed to stock inventory before tariffs were imposed in April. Americans imported more than $1.2 trillion in goods and services in Q1 2025, 23% higher than in the prior year. Perhaps the clearest evidence of tariff frontrunning: pharmaceutical imports doubled in Q1 2025 versus the prior year. Imports declined in subsequent months as firms cleared their inventory stockpiles, narrowing the trade deficit.

This volatility in net exports and inventories wreaked havoc on the 2025 GDP data. The contribution to real GDP growth from net exports printed a record low in Q1 and then a record high in Q2 – for the entire history of GDP data since 1947. This volatility was mostly noise, merely shifting flows between quarters rather than signaling a secular change in demand for foreign goods and services. In this environment, we prefer to track real final sales to domestic purchasers, an alternative GDP measure that excludes trade and inventories, as a more accurate reflection of underlying growth trends.

Signals Within the Noise

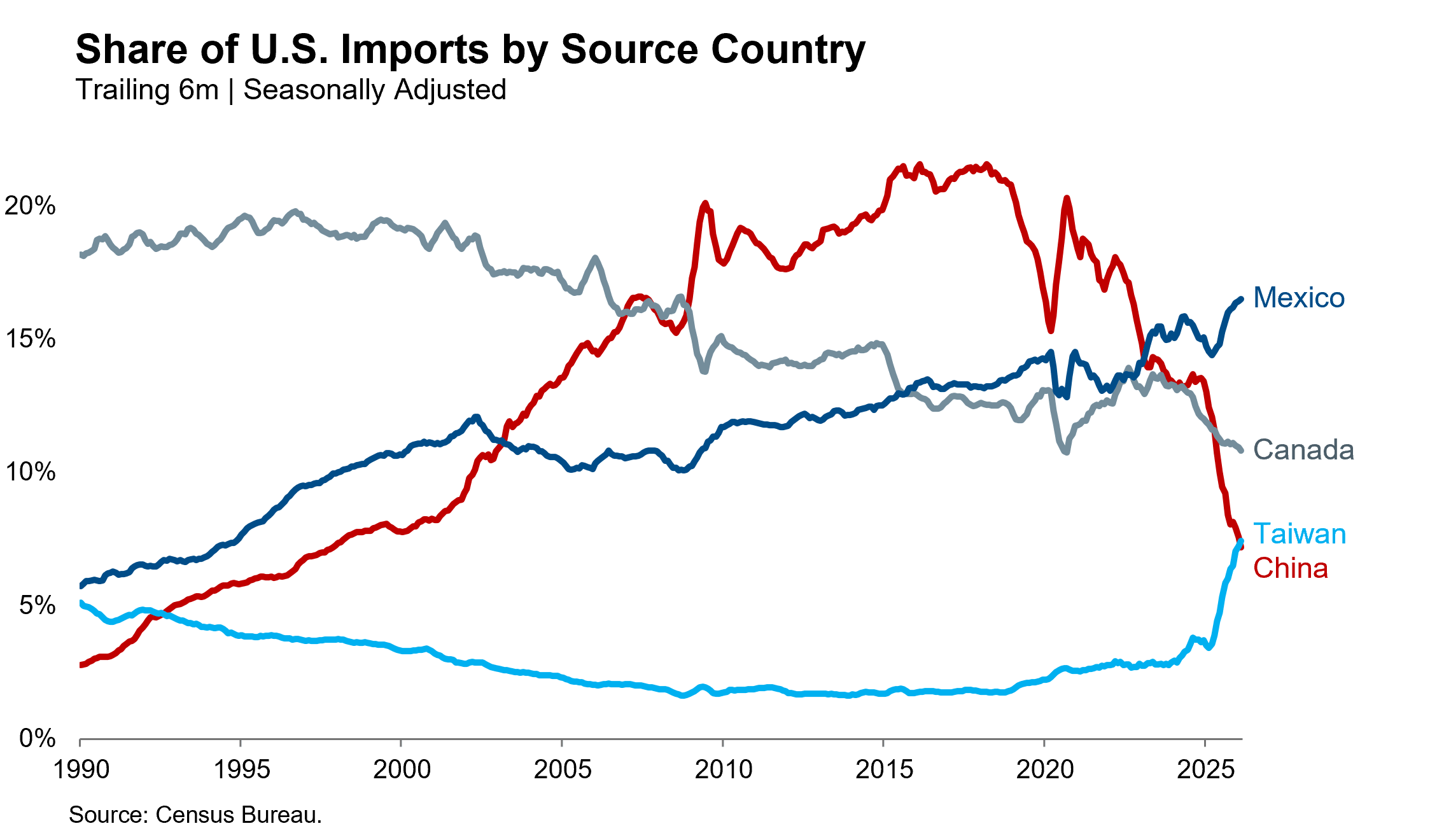

Some fundamental signals are hidden within the noisy trade data. One clear signal is that the gradual decoupling between the U.S. and Chinese economies accelerated sharply in 2025. China’s share of U.S. imports has fallen to just over 7% in the last six months, around the same share as in 1999, before China was welcomed into the global trading system through WTO membership. China has fallen from the #1 supplier of U.S. imports in 2022 to #4 in recent months behind Mexico, Canada and Taiwan. Given this dramatic reversal, one might be tempted to conclude that the decoupling is complete, or that we have reverted to the status quo before the Chinese globalization era. We think that would be an oversimplification. Even if China is exporting significantly less to the U.S., they have cemented their role as a leading supplier of manufactured goods to the global economy, with dramatic consequences for global output and prices. Many Chinese companies have simply moved production or final assembly facilities to other nations that enjoy lower U.S. tariff rates. Indeed, Southeast Asian nations like Vietnam, Thailand, Indonesia, Malaysia and the Philippines have seen a simultaneous surge in imports from China and exports to the U.S. Some of the diverted trade flows could also represent deceptive tariff avoidance practices like transshipment and fraudulent invoicing. Nevertheless, the decoupling in the direct trading relationship between the U.S. and China is real and it gathered steam last year.

Incentives Matter

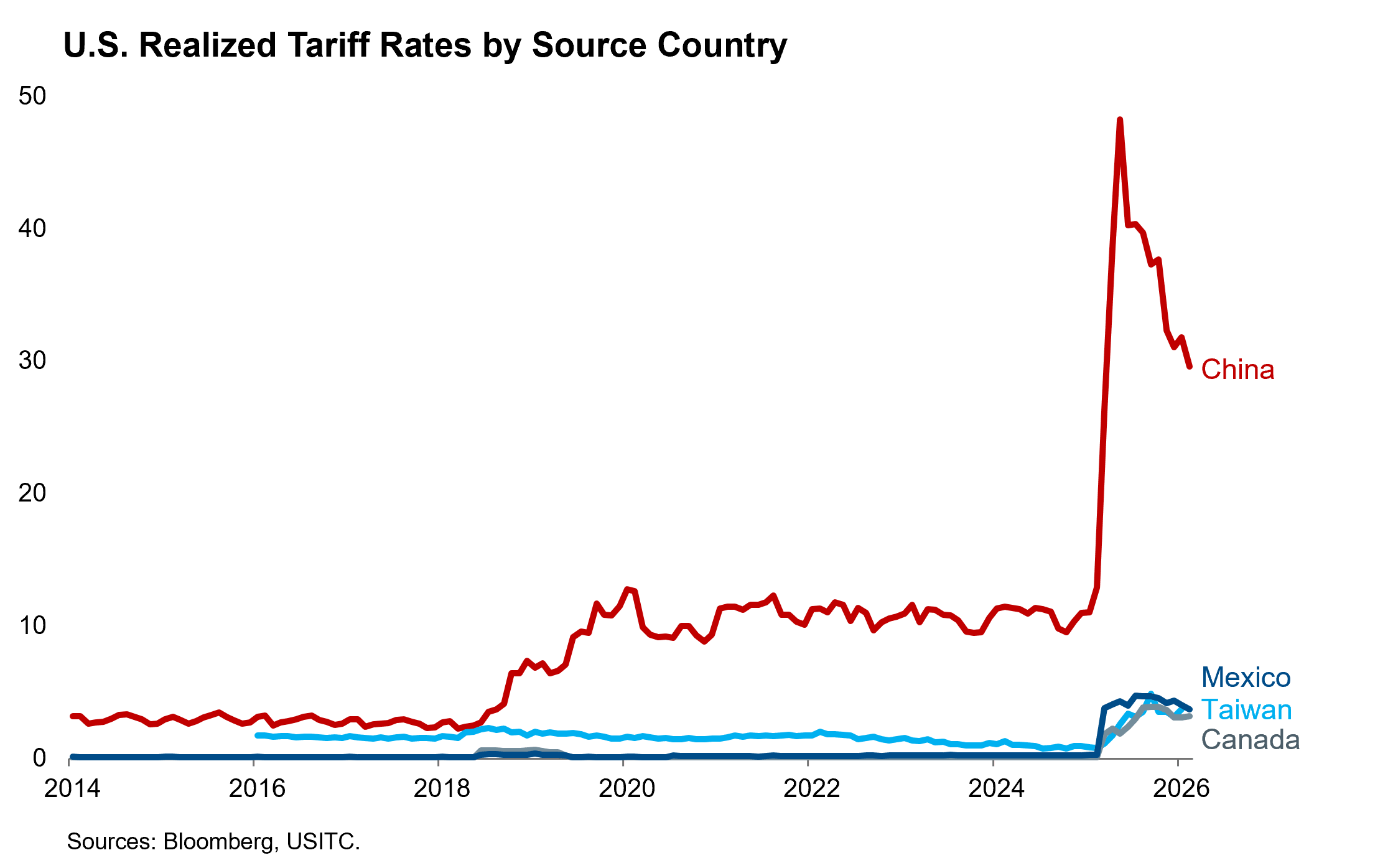

The decoupling is largely a predictable response to the incentives created by tariff policy. The relative decline in Chinese imports began in 2018 when President Trump first raised tariffs on China, then the largest source of U.S. imports. President Biden maintained high Chinese tariffs throughout his term. The realized tariff rate on American imports from China rose from a 2014-2017 average of 2.9% to a 2020-2024 average of 10.7%. This rate rose further to historic highs in 2025, nearly touching 50% in May before falling quickly as President Trump zealously de-escalated through rate reductions and exemptions. Realized tariff rates on America’s other three largest import sources rose by a much smaller magnitude in 2025, and never topped 5%. The realized rate on these three countries has remained low because more than 80% of imports from these countries are exempt from the new tariffs imposed in 2025.

From Hot Wheels to Teslas in One Generation

China decoupling has more recently collided with a new trend: soaring American demand for Taiwanese semiconductors to feed the AI industry’s insatiable demand for computing power. The result is that U.S. imports from Taiwan have surged ahead of those from China in recent months, for the first time since 1993. Computer and electrical equipment account for most of the rise in imports from Taiwan in recent years, and are generally exempted from President Trump’s tariffs. The Taiwan Semiconductor Manufacturing Company (TSMC) has surpassed Intel as the leading manufacturer of the most advanced semiconductors in the last decade. While Taiwan deserves credit for the innovations that have enhanced their export competitiveness, differential tariff rates are also working to reroute America’s trade flows.

A personal anecdote highlights the historical significance of these trade data. My son recently received a toy car for his 5th birthday. As is the case with most toys purchased in America today, the bottom of the car is stamped “Made in China.” To add to his collection, I went over to my parents’ house and unearthed some Hot Wheels from my own childhood in the 1980s. Those antiques feature a “Made in Taiwan” label on the undercarriage. In one generation, Taiwan has climbed the export value chain from toy cars to the world’s most advanced semiconductors that power self-driving cars.