In what was likely the final meeting under Chairman Powell’s leadership, the FOMC left their policy rate unchanged today as expected. In recognition of the extreme uncertainty surrounding the war and energy prices, Powell declined to send any strong signals about the future path of monetary policy. Powell indicated at the press conference that the number of participants favoring a neutral bias had increased between the March and April meetings, which is notable since the ceasefire had temporarily provided some relief in the form of lower oil prices. That interpretation is clouded by the fact that oil prices rose significantly in the final days of the intermeeting period. Regardless of the timing, the hawks are on the ascent as the world waits for oil tankers to start leaving the Strait of Hormuz.

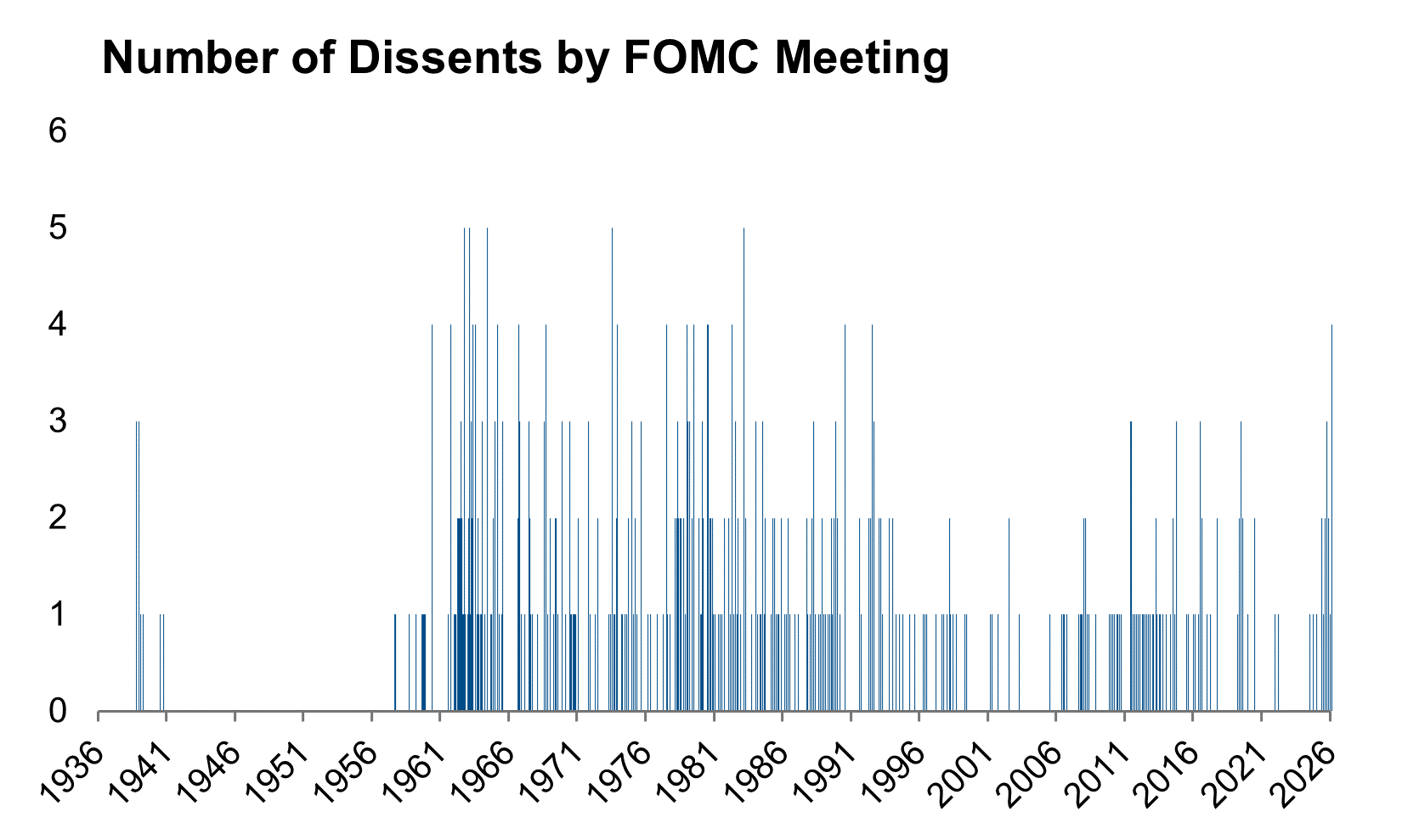

Four voters dissented from today’s decision, an outcome that has not occurred since October 1992. One of the votes was a dovish dissent from Governor Miran, who preferred to cut rates today. The other three were hawkish dissents from Presidents Hammack, Kashkari and Logan, who did not dissent against the policy action but rather against the inclusion of an easing bias in the FOMC Statement language. They preferred to indicate a neutral bias that would signal the next move could be a hike or a cut. The easing bias, therefore, remains in place, but just barely.

These dissents are not a complete surprise because the FOMC minutes reported that the Committee debated the easing bias at the prior two meetings. But raising their arguments to the level of a dissent does send a signal from the hawks to incoming Chairman Warsh that they will not be easily convinced to cut rates. A 34-year high in dissents is not exactly the welcome mat Mr. Warsh was hoping to see upon his arrival. He might want to wear a hard hat at his first meeting, and not only because the Eccles Building is still under construction.

Source: Federal Reserve Bank of St. Louis.

The big news of the day was Chairman Powell’s announcement that he will remain on as a Governor after his term as Chairman ends on May 15, a break with the precedent set by nearly all prior Chairmen. He said that he plans to keep a low profile as Governor and has no intention of being a “shadow chair.” He also complimented his successor several times today, a sentiment that Mr. Warsh has notably declined to reciprocate on numerous occasions in recent months. Powell is an institutionalist and will undoubtedly be rooting for Chairman Warsh to succeed in his pursuit of price stability and maximum employment. We don’t think Powell’s presence will complicate Chairman Warsh’s ability to lead the Committee – Warsh’s own words and the politicized circumstances of his appointment have already done that – but Powell’s decision today does have the effect of delaying President Trump’s next appointment to the Board. Powell’s decision is a political act that he probably took with great reservation. He didn’t start this fight with the administration, but he seems determined to end it on his own terms.

Powell said he is staying to protect the Fed’s independence against the administration’s unprecedented legal attacks and will remain in office until the DOJ investigation “is well and truly over with finality and transparency.” After he is satisfied that the condition is met, he made clear that he will leave at a time of his choosing. We expect that the Supreme Court will soon decide that a president lacks the legal authority to fire a Federal Reserve Governor without cause. Chairman Powell may be trying to establish a further precedent that a president lacks the political power to pressure a Governor to resign.