Comparing De-Risking Strategies from a Contribution Perspective

LDI hibernation strategies may present an opportunity to de-risk at a lower expected cost and on a more flexible contribution schedule than annuity buyouts. Additionally, plans that have not yet de-risked may be surprised by how little their equity allocations reduce expected contributions, and how much contribution volatility they may generate.

Introduction

For more and more defined benefit plans, pension risk has become that rowdy party guest who is ruining the fun for everyone else. The hosts are plotting to get it out the door, and the only question is how they will do so as quickly and quietly as possible.

However, as eager as plan decision-makers may be to push pension volatility out into the cold, they have not forgotten the reason it was invited in the first place. Some of that pension risk brings with it expected excess returns. Sponsors and fiduciaries alike know that selling equities, whether as part of an annuity buyout or an LDI hibernation strategy, means foregoing the expectation that those return-seeking assets may, over time, out-earn the liability. Lowering equity allocations means lower return projections, and lower return means more reliance on sponsor contributions. In other words, de-risking is not without consequences.

And though the risk-return relationship is well understood at an intuitive level, many plans may not feel they have a good way to quantify the impact of various de-risking strategies. How “expensive” is it to sell equities as part of an LDI hibernation solution? How much risk is actually reduced for that price? And how does that compare to the pricing and risk reduction expected from an annuity buyout? While the selection of a de-risking solution will likely be based on many factors,1 the “bang for your buck” of each strategy will undoubtedly be a major consideration.

In this paper, we quantify both the costs and the corresponding risk reduction of two de-risking strategies that can potentially be implemented plan-wide: LDI hibernation and annuity buyouts. Specifically, we focus on how these strategies affect the expected size, volatility, and timing of sponsor contributions. Why contributions? Because eventually, the impact of both hibernation (internally implemented) and buyouts (externally implemented) will flow through the sponsor’s check-book. Hence the contribution perspective provides a way to compare de-risking strategies from a common vantage point.

Establishing a Baseline Prior to De-Risking

Before we compare de-risking strategies, we should start by establishing a baseline. What is the contribution profile of a “traditional” asset allocation of 60% equities and 40% fixed income? What should sponsors and fiduciaries anticipate in terms of total contributions to the plan and, critically, what is the uncertainty (i.e., volatility) of that amount?

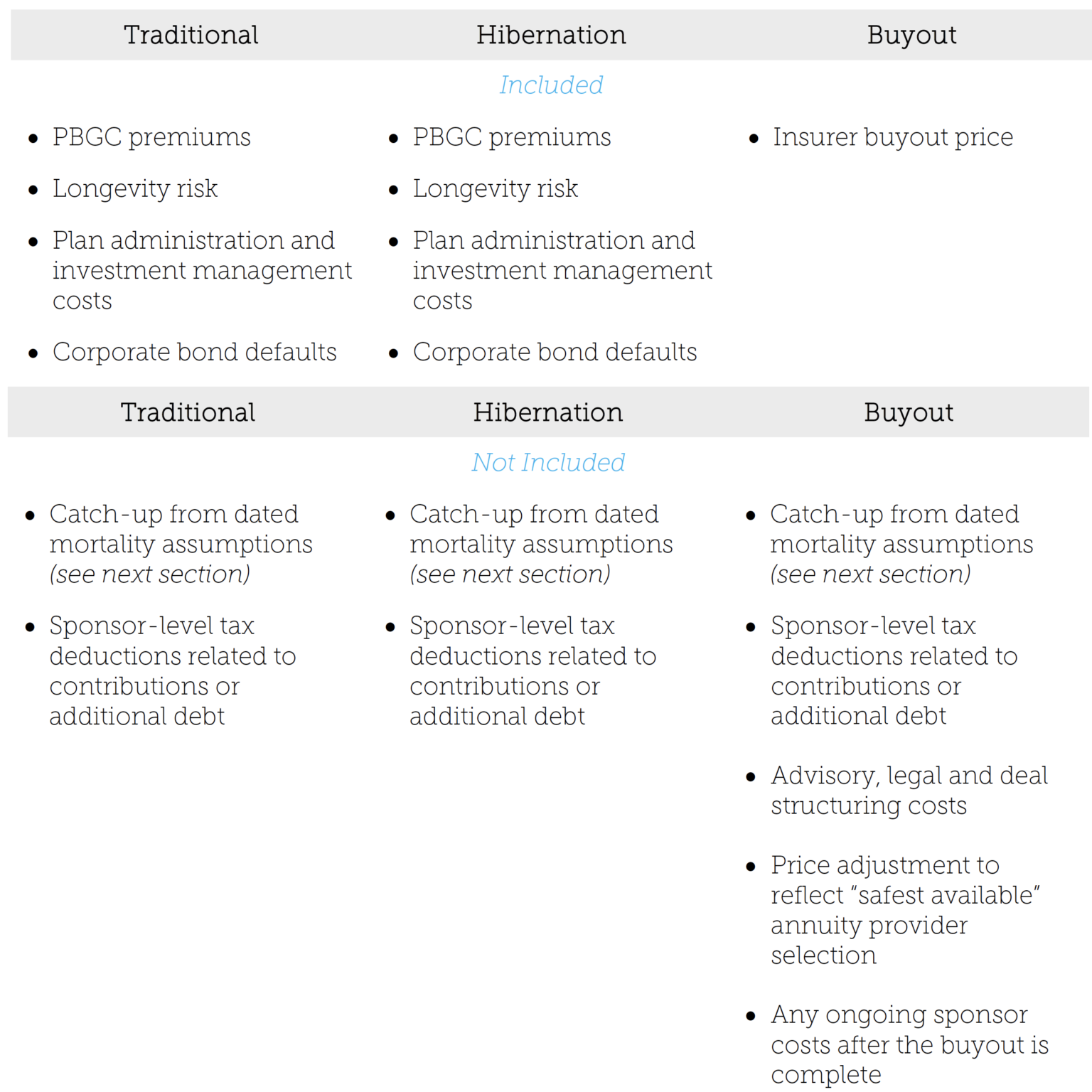

To answer these questions we use a simulation analysis based on a hypothetical pension plan that begins at 90% funded versus a $1 billion PPA liability with a traditional 60/40 allocation. To get a sense of the likely contribution outcomes, we run that plan through 10,000 simulation trials of varying market conditions over a 20-year horizon, during which the sponsor makes the minimum required contributions based on current PPA and MAP-21 funding rules. We also include additional costs to reflect expenses like PBGC premiums2 and plan management fees. As many have noted, the accounting and regulatory (i.e., PPA) valuations exclude several costs that are very real for ongoing plans, and our goal is to capture as many of these as possible in our analysis. Lastly, we include assumptions about additional risk factors like longevity risk and corporate bond defaults that would impact an ongoing plan.3

At the end of the 20-year simulation, we total the present value of each year’s required contribution as well as any final year top-off contribution if the plan is not already fully funded on a PPA basis. Though distinct from a true economic cost,4 we call this 20-year contribution total the “cost”, as a practical measure of the additional cash needed from the sponsor to maintain the plan over a fairly long timeframe.

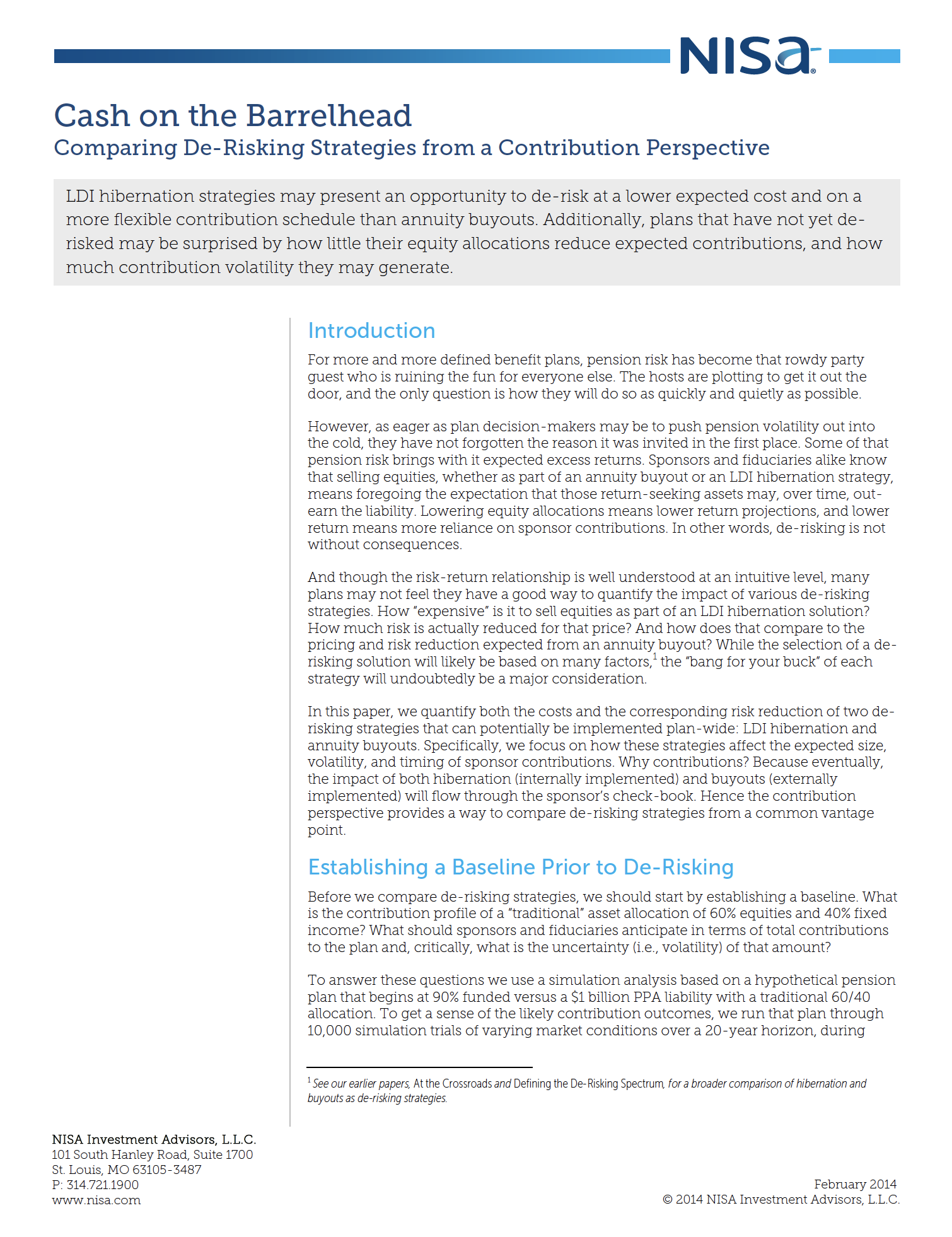

How expensive is it to run our traditional plan over the 20-year period? Exhibit I below shows the “base case” median contribution amount of $237 million based on the 10,000 simulation paths. In addition to the median amount, Exhibit I shows the uncertainty surrounding contributions. The orange bar reflects the 5th-95th percentile range for contributions based on the simulation outcomes. Around the median amount of $237 million, the 5th-95th range indicates that one in twenty paths resulted in a contribution total over $800 million, while one in twenty resulted in contributions less than $10 million.

Two major takeaways are likely to jump out from Exhibit I. First, the base case amount of $237 million is notably higher than the initial $100 million deficit measured on a PPA basis. This difference is largely explained by the fact that the $100 million PPA deficit is calculated using corporate bond yields to discount the liability rather than using Treasury rates. A “risk-free” valuation of the liability based on Treasury rates implies an initial deficit of $322 million, or an initial funded status of only 74% instead of 90%. Meanwhile the corporate discount rate is based on yields that the plan cannot reasonably expect to earn in their entirety when hedging the liability with credit bonds. Over time the portfolio suffers some defaults and downgrades, requiring additional contributions above what the PPA discount rate would have implied. Also, our assumptions of additional costs like PBGC premiums and administrative/management fees add to the cash requirements above and beyond the initial deficit.

The second point of note is that the contribution volatility around the median is substantial. It is probably safe to assume that many plan stakeholders find the idea unpalatable that, in 5% of cases, the plan is projected to need more than three times the base case in additional contributions. Indeed this contribution uncertainty is simply a manifestation of the underlying funded status volatility that so many plans are already eager to rein in with a de-risking program. (Further, the growing popularity of dynamic allocation strategies like glidepaths implies that fewer plans are likely to retain such large equity allocations at higher funded status levels. We discuss glidepaths in the Appendix.)

For pension risk decision-makers the question then becomes, “how much of that uncertainty can I eliminate by de-risking and at what cost?”

De-Risking with Hibernation

We now introduce a de-risking strategy, LDI hibernation, to examine the effects both on contribution amount and the corresponding uncertainty around that amount. How much does a switch to hibernation, in which most or all plan assets are dedicated to liability hedging, increase cash contributions and reduce their volatility?

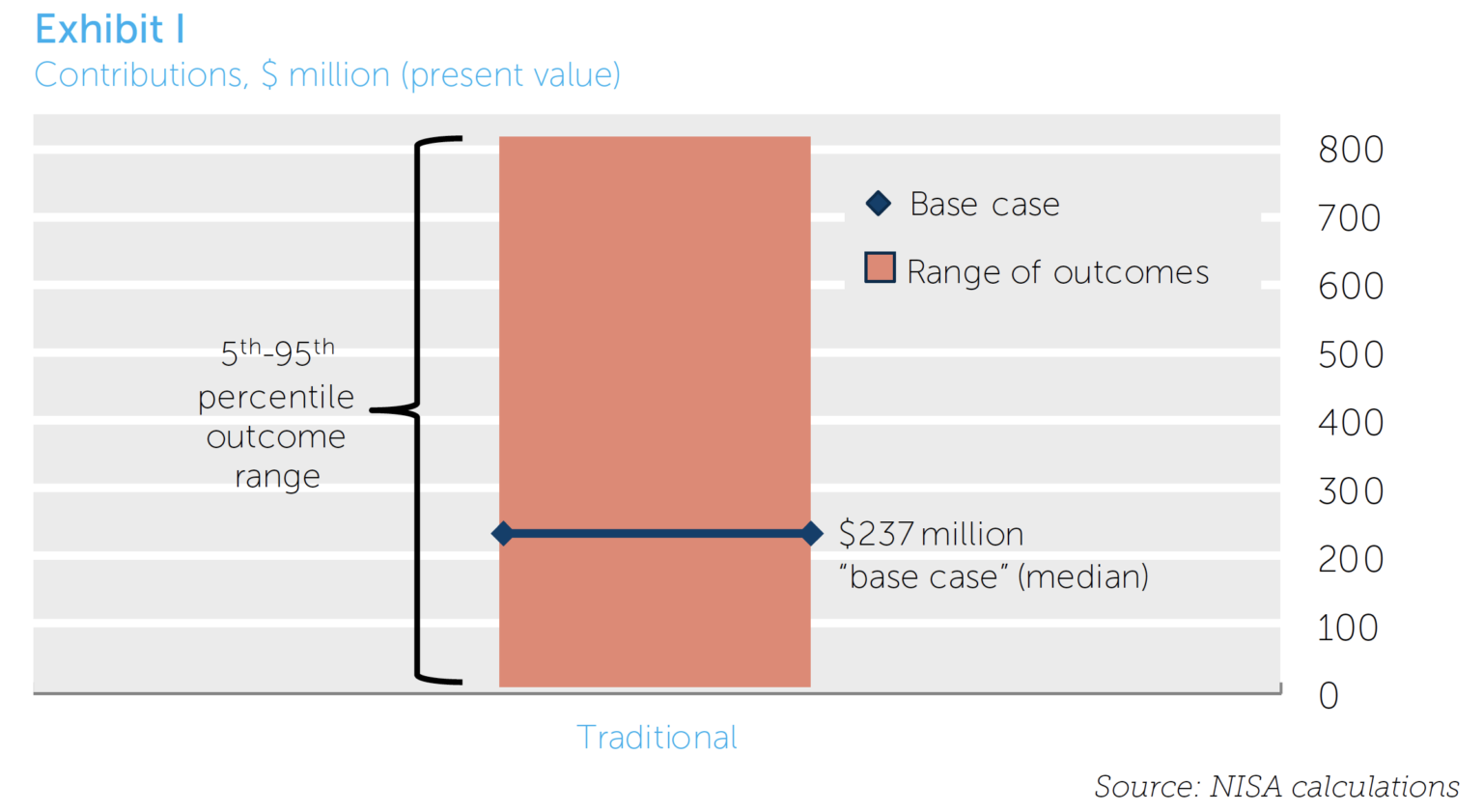

Exhibit II below compares the contribution profile of our traditional plan to a hibernation plan, which differs only in asset allocation. Instead of owning 60% equities, the hibernation plan is based on a 100% allocation to long duration credit bonds. We also assume a modest use of derivatives to hedge the remaining amount of liability interest rate exposure not hedged by the assets themselves. Otherwise, the assumptions are the same, including the assumption of starting at 90% funded (i.e., hibernation need not require a fully funded plan).

Two notable, if not surprising points can be gleaned from Exhibit II. First, the median contribution amount of $273 million seems only marginally higher than the $237 million cost for the traditional plan – an additional cost of only $36 million on a billion dollar plan. How can this be? Where is the supposed benefit to the traditional plan from holding equities and other assets that promise a risk premium?

In large part this missing payoff can be explained by the asymmetrical impact, from a sponsor contribution perspective, of holding return-seeking assets like equities. In bad market scenarios, contribution requirements increase as funded status deteriorates. But in good scenarios, higher funded status has a limited impact on the sponsor, since plan surpluses can only reduce contributions to zero.5 Said differently, once a plan is fully funded from a regulatory perspective (which PPA requires over a 7-year timeframe), leaving the assets invested in equities means they can only do harm by requiring more contributions if markets decline, but can’t reduce contributions if markets rise.

In that sense, it is perhaps less surprising that the hibernation strategy does not require much more cash than the traditional strategy, in which the long-term impact of equity allocations is effectively capped from the sponsor’s perspective.

Second, we note the dramatic reduction in contribution volatility in hibernation. The 5th-95th range of simulation outcomes is much tighter, with roughly $60-70 million of uncertainty in either direction from the median contribution total. While the majority of the market risk has been removed by matching assets to the liability, some residual volatility remains due to remaining risk factors like longevity risk and variation in corporate bond defaults and downgrades. Nonetheless, the risk-return tradeoff of a hibernation strategy seems quite compelling. By comparison, the traditional strategy appears to be risking a lot to gain a little.6

Having seen one de-risking strategy, the question quickly turns to how various strategies stack up against each other. We expect sponsors are most eager to compare hibernation to annuity buyouts. However before doing so, we should acknowledge that any real world decision is likely to consider broader factors beyond the contribution analysis we present here. Decision-makers are likely to include a variety of quantitative and qualitative factors when weighing the pros and cons of hibernation and annuity buyouts, such as the value of a buyout’s longevity hedge, the risks associated with litigation, and so on.

De-Risking with a Buyout

To assess an annuity buyout, we cannot use the same simulation approach used for hibernation and traditional strategies. However, we can instead look to the current market for annuity buyouts to calculate a transaction price for our 90% funded plan. And while a buyout does not have the ongoing contribution volatility of a traditional or hibernation strategy, there is a range of prices from different insurers that results in uncertainty surrounding execution price at any point in time.

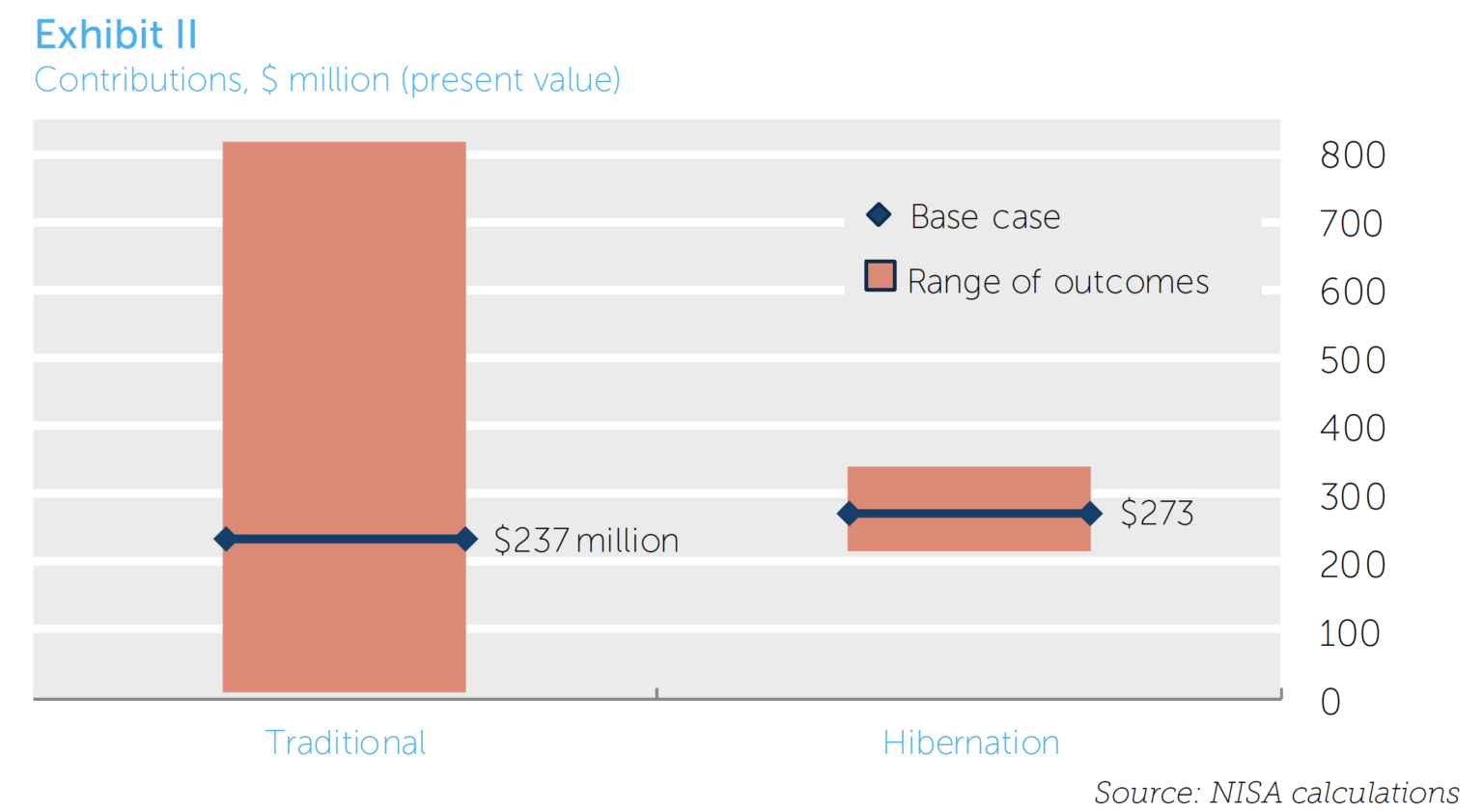

Exhibit III shows the cost of a buyout for our hypothetical plan based on the average of third-party annuity pricing data,7 as well as a one standard deviation range around the average price based on the variation among insurer quotes.

Our hypothetical plan is projected to require $302 million from the sponsor to execute a buyout. Conceptually this can be broken into the $100 million deficit on a PPA basis, plus an additional $202 million to reflect a variety of components like the longevity hedge, the assumption of market risk associated with the corporate bond liability discounting, insurer profit margin, and so on.

A modest amount of uncertainty surrounds this average buyout price estimate, amounting to less than $20 million in either direction. Contribution uncertainty deriving from market risks would obviously be non-existent after the buyout, from the sponsor’s perspective, since that risk has been entirely transferred to the insurer.

In comparing buyouts to hibernation, sponsors may find it intuitive to take a risk/return perspective as they likely would in making other investment decisions – something akin to a Sharpe or information ratio. Compared to a buyout, hibernation is expected to require $29 million less in contributions, with a standard deviation of $40 million over the 20-year horizon. The ratio of return to risk in this decision is 0.7, which is a tradeoff sponsors may find appealing.

Of course, over time the factors affecting these prices can change. For example annuity pricing data relative to a corporate-discounted liability can fluctuate month over month. But based on our analysis, hibernation may strike pension plan decision-makers as the most “cost-effective” way to get the large majority of pension risk off the table.

All in the Timing

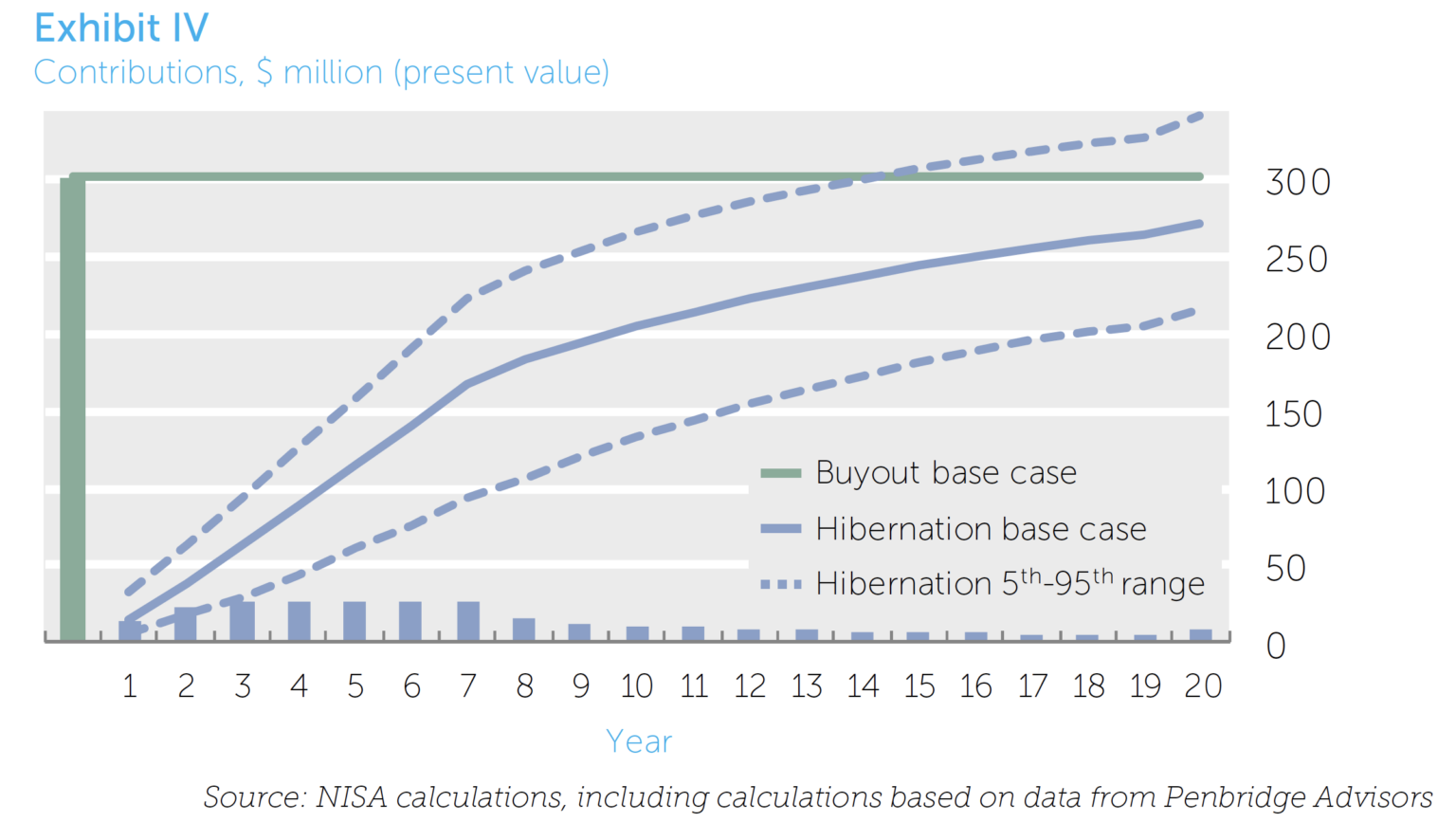

Any discussion of de-risking from a cash infusion perspective would be incomplete without addressing one more dimension: timing. Whether it’s the CFO writing the check or the CIO who is relying on it, the timing of cash contributions is likely to be a factor in the de-risking decision.

Hibernation is projected to require less cash than a buyout for the next 15 years, in 95% of cases.

Exhibit IV compares the timing of required cash flows from the sponsor to support either a hibernation or buyout strategy. The buyout flow is simply the $302 million we calculated above, assumed to be due immediately. The hibernation flows are based on the same data from our simulation analysis, with bars reflecting each year’s contribution and cumulative contributions reflected in the upward-sloping line. The contribution in the final year reflects any remaining deficit on a PPA basis. Lastly, the dotted lines indicate the 5th-95th ranges of cumulative contributions.

For those plans whose corporate sponsors are not flush with cash or willing to tap capital markets to borrow on behalf of the pension, the appeal of the hibernation strategy is evident. Rather than a single up-front expense, the sponsor can plan to make contributions on a distributed schedule over the long term, and with most of the contribution uncertainty removed. Except in the worst case scenarios, the hibernation plan is projected to require less cash than the buyout for the next 15 years (when the 5th percentile hibernation line crosses the buyout line).

Conclusion

Pension plans seeking to de-risk are naturally going to be selective shoppers when picking a risk reduction strategy. They will want to ensure they get plenty of bang for their de-risking buck. However, an accurate price comparison between strategies can be hard to come by. While a cost estimate for an annuity buyout is readily available from insurers’ quotes, how should sponsors compare that to the cash needed to keep the plan on the balance sheet to allow the fiduciary to de-risk with an LDI hibernation strategy?

One common vantage point from which to compare strategies is sponsor contributions. Different de-risking strategies have notably different contribution profiles in terms of the size, timing, and volatility of the cash infusions required by the sponsor. Our analysis

examines contributions over a 20-year horizon to establish these profiles – first for a traditional 60/40 allocation, then for an LDI hibernation strategy, and ultimately for an annuity buyout.

For a plan with a traditional allocation, we find that hibernation only implies a marginally higher cost over the 20-year horizon, which may surprise those who expect equities to “make the plan cheaper” in a material way. Meanwhile the large majority of the uncertainty around contributions is eliminated with the assets dedicated to liability hedging.

Further, the contribution profile of hibernation may be very appealing in comparison to annuity buyouts. In hibernation the sponsor can expect to contribute less, and on a distributed schedule during the 20-year horizon, versus an annuity approach.

Ultimately, some sponsors may prefer annuity buyouts and for some very good reasons. However, we expect many will choose to keep the defined benefit plan hibernating on the balance sheet, unlikely to deliver any unpleasant surprises when it comes time to cut the annual contribution check.

APPENDIX

Assumptions and Data Sources

Data sources (as of 09/30/2013):

- Annuity pricing reflects NISA calculations of a liability discount rate and corresponding buyout price based on an interpolation of liability discount rate data from Penbridge Advisors

- MSCI ACWI data from Bloomberg

- Barclays Long Credit Index data from Barclays

- Hypothetical liability assumed to be frozen with no new benefit accruals; assumed to have a duration of 12 years

- Present value calculations based on Treasury rate discounting

- Correlations between asset classes based on 5 years of monthly historical data ending 09/30/2013

- Assumes longevity risk of 0.4% annually in funded status terms that is uncorrelated with asset classes

- Additional 0.4% annual cost is assumed to capture ongoing plan costs like administrative and manager fees, etc.

- Equity allocations assumed to be MSCI ACWI with a 3% annual risk premium

- Fixed income allocations assumed to be Barclays Long Credit Index. The option adjusted spread (“OAS”) is assumed to average 1.9% with 0.72% annual volatility. Each year we assume that on average the portfolio loses half of the OAS due to defaults and downgrades, and with an annual volatility of 0.75% around that amount.

- Assumes all relevant PPA and MAP-21 funding regulations as of 09/30/13, as well as PBGC premium changes resulting from December 2013 federal budget legislation.

- Contributions for years 1 through 19 reflect the required contributions for the respective year. Contribution in year 20 reflects any remaining deficit on a PPA basis.

A note about the new mortality assumptions

Many are aware that the Society of Actuaries is expected to release updated mortality tables and has already released an interim update to the earlier mortality improvement scale. For the hypothetical plan used in our analysis of buyouts, hibernation and traditional strategies, we assume that the most current mortality assumptions are used to value the liability in all cases. Effectively that means that, to the extent any given plan’s liability projections are based on older mortality estimates, additional contributions will be expected regardless of the de-risking strategy it selects.

For example, insurers are already likely to revalue the liability based on the latest mortality assumptions available. Therefore, our buyout cost projection underestimates the actual pricing for a plan that is valuing the liability using the dated mortality assumptions, perhaps by as much as 5-10% of funded status.

If the de-risking strategy results in the sponsor retaining the plan (e.g., hibernation, traditional), we expect the new mortality assumptions will eventually work their way into the accounting and regulatory liability calculations, and thus into contributions, though on a less immediate timeframe compared to a buyout.

In either case, it is safe to say that plan funded status industry-wide likely overestimates the economic reality to the extent they are using “stale” mortality assumptions – regardless of when the latest assumptions are formally released and integrated into official liability valuations.

Considering dynamic glidepath strategies

Many readers may note that an important alternative exists to the various static asset allocations that we discuss in this paper – namely, dynamic glidepath strategies. A glidepath is a dynamic asset allocation strategy in which equities are sold and liability hedging assets bought as funded status rises, often beginning at a traditional allocation and ending with a hibernation allocation. One of the primary benefits of these dynamic strategies is to avoid the asymmetric risk-return tradeoff of holding equities as the plan nears a target funded status level, as discussed earlier.

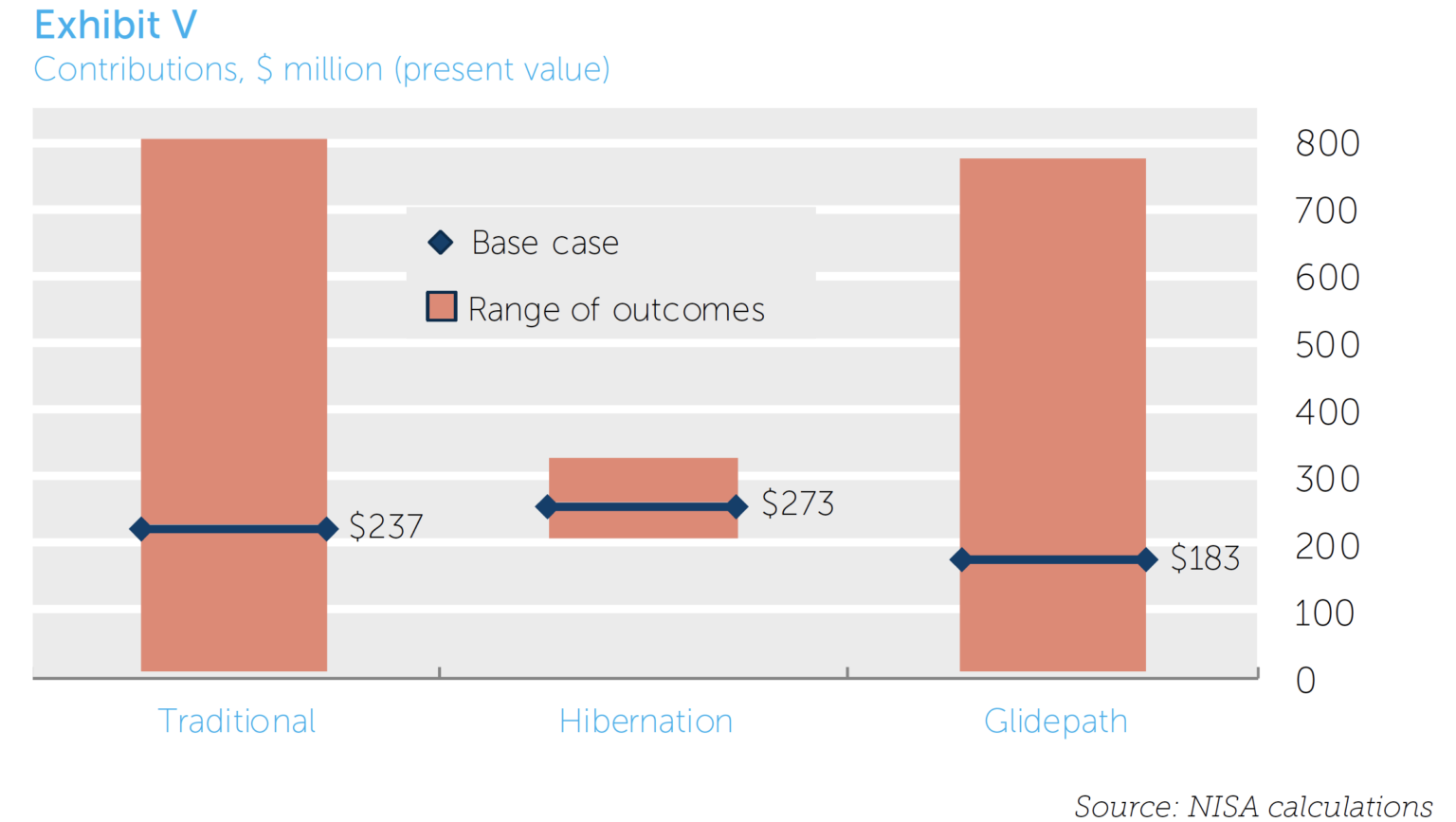

Exhibit V includes the simulation results for a simplified glidepath strategy compared to the traditional and hibernation allocations (for simplicity our “glidepath” is based on the60/40 allocation until the plan reaches 100% funded on a PPA basis, at which point it converts to hibernation):

With the glidepath strategy the sponsor contributes notably less over the twenty years – only $183 million – than in either the traditional or hibernation cases. For the intuition behind why the median total is lower, picture the scenarios with the traditional allocation in which the plan reaches fully funded. At that point the plan has a lot to lose and little to gain from a contribution perspective from continuing to hold equities. In some cases, subsequent bad market outcomes will lead to a deterioration of funded status and require additional contributions. Those contributions could have been avoided by “locking in” the fully funded status with liability hedging assets, which is exactly what occurs with the glidepath strategy. (It’s worth reiterating that our calculations do not assign any value to plan surpluses from the sponsor’s perspective, which effectively penalizes the traditional allocation for holding equities at higher funded status levels).

Perhaps noteworthy is that contribution volatility is not much lower with the glidepath compared to the traditional allocation. This makes sense given that most of the scenarios that lead to material additional contributions are scenarios in which equities do poorly and funded status drops. In other words, scenarios in which there is effectively no difference between the strategies since the glidepath’s de-risking trigger is never reached, or is reached later when the impact is diminished.

In any case, the comparison presents an interesting choice for fiduciaries looking to de-risk via asset allocation choices. Hibernation may present an opportunity to eliminate most of the contribution volatility, but with the expectation of more reliance on the sponsor’s contributions in the base case. Meanwhile the glidepath strategy still introduces a lot of contribution volatility, but with a base case contribution amount that is less than either of the static strategies.