This article broadens investment skill beyond market forecasting to include structuring skill—encompassing engineering, market-making, operational and access capabilities. Learn how allocators can evaluate managers using both qualitative and quantitative frameworks.

Key Takeaways:

- Investment skill extends beyond market forecasting to include structuring skill

- The four key components of structuring skill include: engineering, market-making, operational and access

- Managers with higher structuring skill can demonstrate more robust alpha

- Quantitative evaluation using the Fundamental Law of Active Management helps assess manager skill

- Allocators demonstrate structuring skill through portfolio design and governance

Introduction: The Evolution of Investment Skill

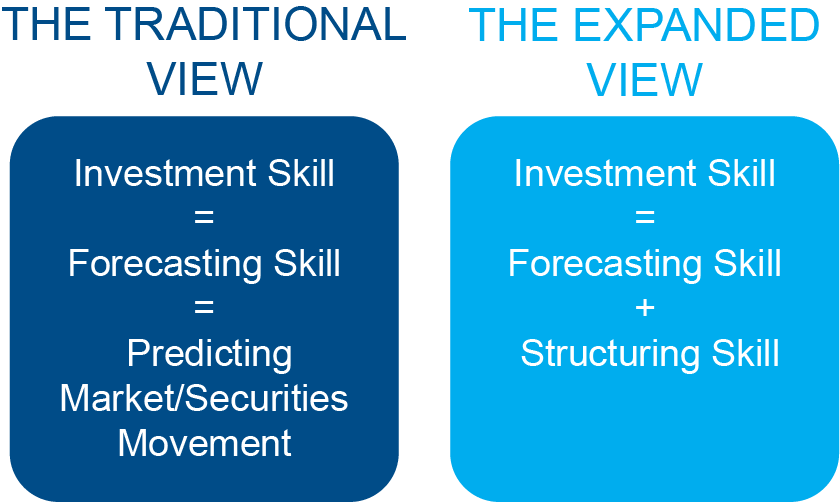

Prior to the 1960s, performance was measured simply by total return, with no distinction between alpha and beta. The distinction began with the Capital Asset Pricing Model (CAPM) and was later expanded by concepts such as Jensen’s Alpha and factor investing. Strategies once viewed as solely alpha, such as value investing, trend-following and volatility harvesting, now sit along the beta-alpha continuum. An underexplored but important question is: What is investment skill? While alpha is a way to measure a manager’s skill,[1] investment skill is commonly defined with a limited breadth.

Too often, investment skill is reduced to whether a manager has a crystal ball for predicting the path of markets or broad sectors. Skill is much more and is not reserved solely for the brilliant. In this article, we expand the definition of investment skill and give allocators quantitative and qualitative tools for its evaluation.

Defining Structuring Skill: The Four Components

What is Structuring Skill?

Structuring skill is the ability to design, source and implement exposures efficiently and intelligently.

Efficiently = minimizing transaction costs, financing costs and market impact

Intelligently = implementing exposures that best reflect the underlying market view

Beyond forecasting skill, the broader investment skill set we focus on is structuring skill. While similar concepts have been suggested in the past, we believe structuring skill requires a broader, more precise definition. We define “structuring skill” as the ability to design, source and implement exposures efficiently and intelligently.

Efficiently means implementing a strategy in a way that minimizes transaction and financing costs, and market impact. Intelligently refers to implementing exposures that best reflect the underlying market view. While we focus on asset manager structuring skill, asset allocators can demonstrate substantial structuring skill through portfolio design and governance processes.

We break structuring skill into four sub-skills:

1. Engineering: Designing Strategies That Reflect Your Actual Market Views

Engineering skill indicates the ability to design and build complex trading strategies that reflect your actual market view. When trades take on ancillary risk positions, this “trade baggage” pollutes the manager’s market view. In many cases, trade baggage manifests as a higher tracking error, resulting in a lower information ratio. We provide an example from equity and fixed income below.

Example 1: U.S. Credit Manager—Treasury Yield Curve Positioning

Scenario: A U.S. credit manager has a view on the Treasury yield curve. In particular, they believe the 2s10s part of the yield curve will steepen. They need to implement a 2-year overweight and a 10-year underweight. In order to facilitate this trade, they have a few implementation choices:

Good: Underweight 10-year credit securities and overweight 2-year credit securities. Importantly, the manager’s view is on the shape of the Treasury curve, not the spread curve. In addition, the manager would be unable to maintain duration neutrality, introducing additional risk to the portfolio.

Better: Underweight 10-year credit securities and overweight 2-year credit securities, but use U.S. Treasury futures to maintain the appropriate duration. The manager still has a spread steepener, but has avoided the duration mismatch.

Best: Invest in their optimal credit portfolio but overlay a 10-year U.S. Treasury futures short position and a 2-year U.S. Treasury futures long position. Now the manager can reflect only their intended view, and effectively materially reduce the trade baggage associated with the position.

Example 2: U.S. Equity Manager—Sector Allocation View

Scenario: A U.S. equity manager has a strong view on being overweight (+6%) in consumer staples and underweight (-6%) in REITs. Assume consumer staples account for 5% of the manager’s benchmark and REITs for 2%. They also have a few implementation choices:

Good: Sell the 2% in REITs and add 2% to consumer staples. The manager is only able to achieve one-third of their target, 6% overweight.

Better: Sell the 2% in REITs and 4% in, say, technology in order to add 6% to consumer staples. The manager is able to reach the full long position sizing but failed to implement their underweights and, in the process, impacted other parts of the portfolio. In our experience, a technology underweight is a common incidental position given the current market structure, not an intentional or desired allocation.

Best: Sell the 2% in REITs and institute a 4% REIT short position by either directly shorting securities or using synthetic markets. Then institute the 6% consumer staples long position. Once again, the manager reduced the trade baggage associated with the position.

These examples provide somewhat obvious ways for managers to apply engineering skill to reduce unintended risks in each position and thus raise their information ratio. In practice, many active views are more nuanced, materially increasing the required engineering skill.

Allocators play a key role in both examples. Either derivatives and/or shorting of individual securities was required to isolate the intended view. A governance process that allows these tools with the appropriate oversight is a way to better access a manager’s engineering skill. Engineering skill doesn’t stop at the manager level. These concepts can be deployed portfolio-wide, enabling allocators to better manage both beta and alpha at the total portfolio level.

2. Market-making: Creating Returns Through Liquidity Provision

Market-making skill reflects how a manager creates return opportunities by providing market liquidity. This skill is not reserved just for broker/dealers who continually make two-way markets across the globe. Arguably, managers can participate in this market as well. Those who can harvest liquidity premia by effectively lending their available balance sheet and intermediating markets can be especially lucrative during stressful periods, demonstrating market-making skill.

Examples of Market-making Skill

- In over-the-counter (OTC) markets, like investment-grade corporate bonds, this includes making a portfolio always available for sale at or above the fair market offered-side price.

- In equity portfolios, this reflects the ability to lend your stocks to help facilitate other investors’ short positions.

- Providing liquidity during market dislocations like the downgrade of corporate bonds from investment grade to high yield or supporting price convergence between London and New York silver markets are all market-making functions.

Sometimes the “skill” is being ready with a deployable risk budget. Market opportunities can be fleeting. Investors who stand ready with the toolkit, willingness and know-how are best suited to earn alpha. At the allocator level, having an allocation in the Strategic Asset Allocation (SAA) that promotes the opportunistic deployment of capital provides a better way to access this investment skill.

3. Operational: Processing and Handling Complex Strategies

Operational skill indicates a manager’s ability to appropriately process and handle complex strategies. We refer to this as having a high pain threshold, as these practices require great attention to detail and are not the most glamorous throughout an organization. For this skill to be effective, the mindset must be pervasive across the organization. This means having an operations and technology team that can book and value complex trades, a legal team to assist with highly bespoke instruments often across multiple jurisdictions, and trading teams that handle cross-asset multi-instrument trading. Operational investment skill spans all areas of an organization.

Examples of Operational Skill

- Accessing physical commodities markets—Taking delivery of physical commodities requires attention to detail that is critically important. After all, no one wants 100 lean hogs showing up at the office door.

- Legal document details—When trading OTC derivatives, the ability to negotiate unique terms (e.g., delivery options or special termination rights) to protect against potential risks is critical.

- Multi-instrument derivative implementation—Having the wherewithal to implement exposures across different derivative markets introduces operational and legal complexities that can be quite daunting.

Allocators who can deploy derivatives for direct leverage or risk management while still maintaining proper oversight and accounting for the performance and custodial headaches that come with these strategies are demonstrating operational skill.

4. Access: Leveraging Network Effects and Market Presence

Access skill represents a larger network or access effect that a manager has in a particular market. Continual presence, reputation and size bring unique opportunities. Given the nature of this investment skill, it is often enduring, hard to lose once established, and hard to establish for new market participants.

Examples of Access Skill

- Better private equity opportunities—Large established firms may have portfolio companies wanting to work with the manager, and managers, by extension, can choose the companies with which they work.

- New issues—Trading activity and reliable participation in the new issue markets result in better access going forward.

- Broker/Dealer access—A broader and more established stable of counterparties provides better market access and execution across a wide set of global markets.

Sub-skill Overlap in Practice

Engineering, market-making, operational and access sub-skills collectively make up what we refer to as structuring skill. While the examples were assigned specific categories for clarity, in practice, they frequently overlap. For example, fixed-income new issues relate to both market-making and access, while harvesting the volatility risk premium relates to engineering, operational, and market-making. Structuring skill is often embedded in the firm, not the individual, which allows for:

- Greater persistence over time

- Transferability across strategies

- Less dependence on individual forecasting brilliance

While a manager’s structuring skills are important, allocators are critical and can amplify structuring skills through portfolio design, governance and opportunistic capital deployment.[2]

Defining Robust Alpha: Key Characteristics

To appreciate the value of these investment skills, we need to define “robust” alpha. In doing so, we find that robust alpha characteristics occur more frequently from structuring than from forecasting skill. Repeatability, frequency and replication barriers are often driven by structuring, rather than by forecasting.

Four Characteristics of Robust Alpha

- Repeatable—This does not mean the specific view needs to be repeatable, but rather that the process of generating and implementing portfolio views is repeatable. An equity manager who identifies a market dislocation they never expect to see again could have robust alpha if they have a repeatable process for identifying similar opportunities in the future.

- Frequent—The collection of underlying opportunities must occur often enough to be meaningful to the portfolio. Said differently, a repeatable process can be used, but if it identifies an opportunity once every 10 years, it is likely not very valuable.

- Hard to replicate—For an alpha source to persist, there should be some barrier to entry. Contrary to popular belief, the barrier is often the effort required and dealing with complexity, not just proprietary insight.

- “Not beta in a trench coat”—This is perhaps the most important, and our biggest concern about active manager performance.[3] Beta is repeatable and frequent, but it is not alpha. It’s an attractive nuisance for managers who can easily add beta to a portfolio. It is then commonly mistaken for alpha and can masquerade as such for an extended period. Beta disguised as alpha works—until it doesn’t. As 2008 recedes further into managers’ rearview mirrors, the temptation to use beta in a portfolio grows.

Quantitative Framework: Evaluating Investment Skill

With our refined definition of skill and characteristics of robust alpha, we see themes emerge. Specifically, the emphasis on process, models, and attention to detail, rather than broad discretionary market calls.

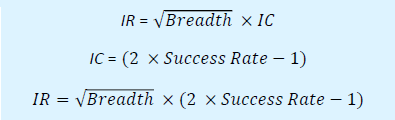

To this point, we have relied on qualitative methods to assess investment skill, which leads to robust alpha. Undoubtedly, the broader definition of investment skill requires a qualitative assessment to understand what active managers bring to the table and whether that translates into robust and therefore reliable alpha. However, quantitative measures can be useful for evaluating the internal consistency and believability of a manager’s strategy. We pose two questions for managers:

- How many independent views are expressed in the portfolio (e.g., how wide is the manager’s breadth)?

- What is the success rate per decision?

These questions reconstruct the Fundamental Law of Active Management.[4] All else equal, managers with greater breadth and higher success rates produce higher information ratios. Those who rely exclusively on forecasting skill, rather than a combination of structuring and forecasting, will find it more difficult to maintain success rates or will need to materially increase the breadth of their forecasts. The formulas are outlined below:[5]

In practice, adding a transfer coefficient reflects how effectively a manager’s view can be translated to portfolio positions. Constraints such as transaction costs, investor restrictions, and, often, manager limitations, reduce the transfer coefficient below one, as depicted in the formula below:

In practice, allocators should care about their resulting information ratio and the manager’s success rate, while recognizing the real-world limitations. However, we make the distinction between the transfer and information coefficient because components of structuring skill, engineering and operational, directly impact the transfer coefficient. While market-making and access skills disproportionately influence the information coefficient through opportunities and trade access, as well as capital deployment during periods of market stress (e.g., high risk premiums), thereby raising the probability that views are successful.

We have focused on success rate thus far; however, breadth is equally important. Breadth refers to the number of independent views in the portfolio. Independence is key. A view on the level and shape of the yield curve is unlikely to be truly independent, as they are related by common macroeconomic factors. They represent more than a single view but certainly not two truly independent views. Alternatively, the idiosyncratic risk of a single stock in one industry is much less correlated to that of a single stock in another industry, bringing the breadth closer to two.

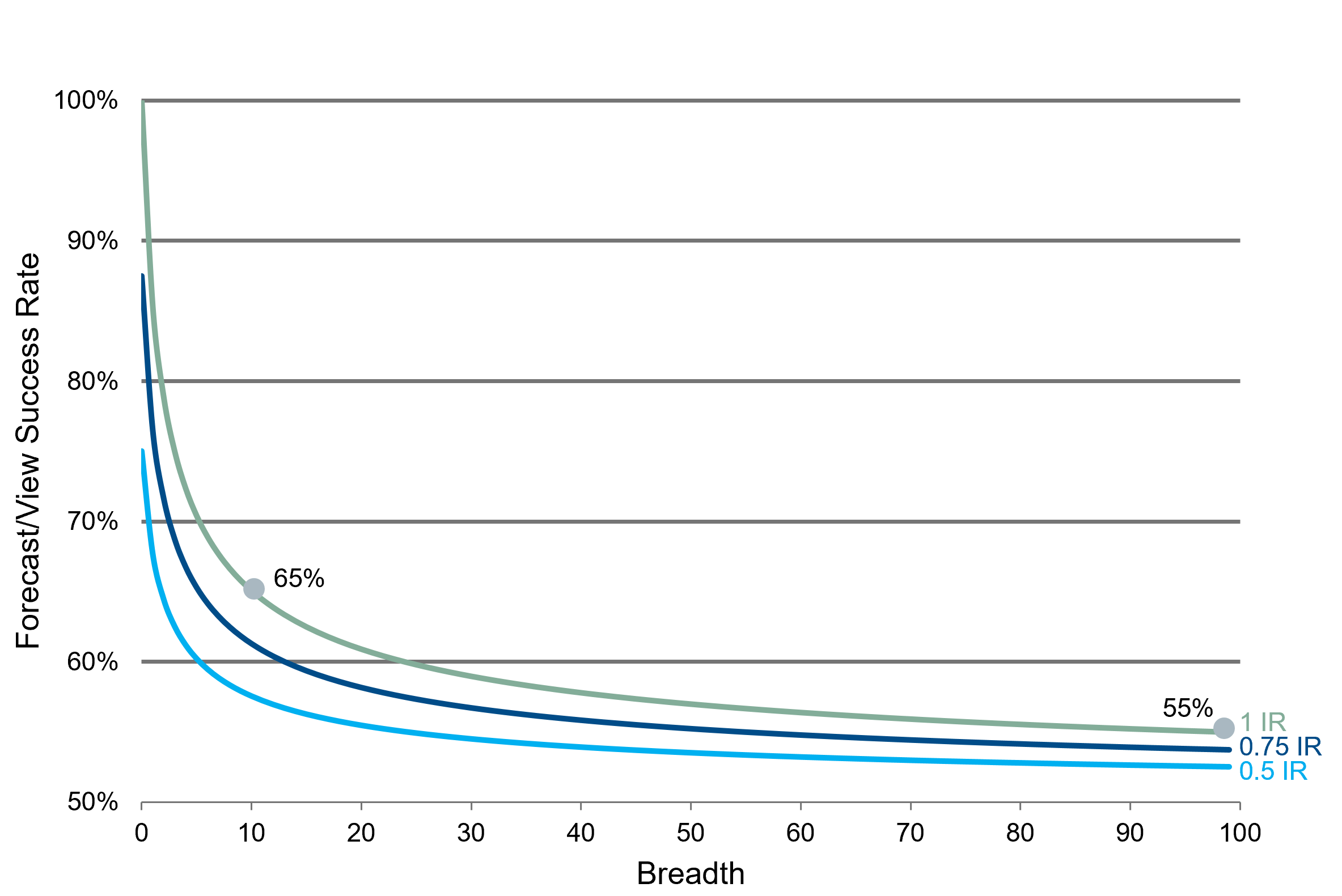

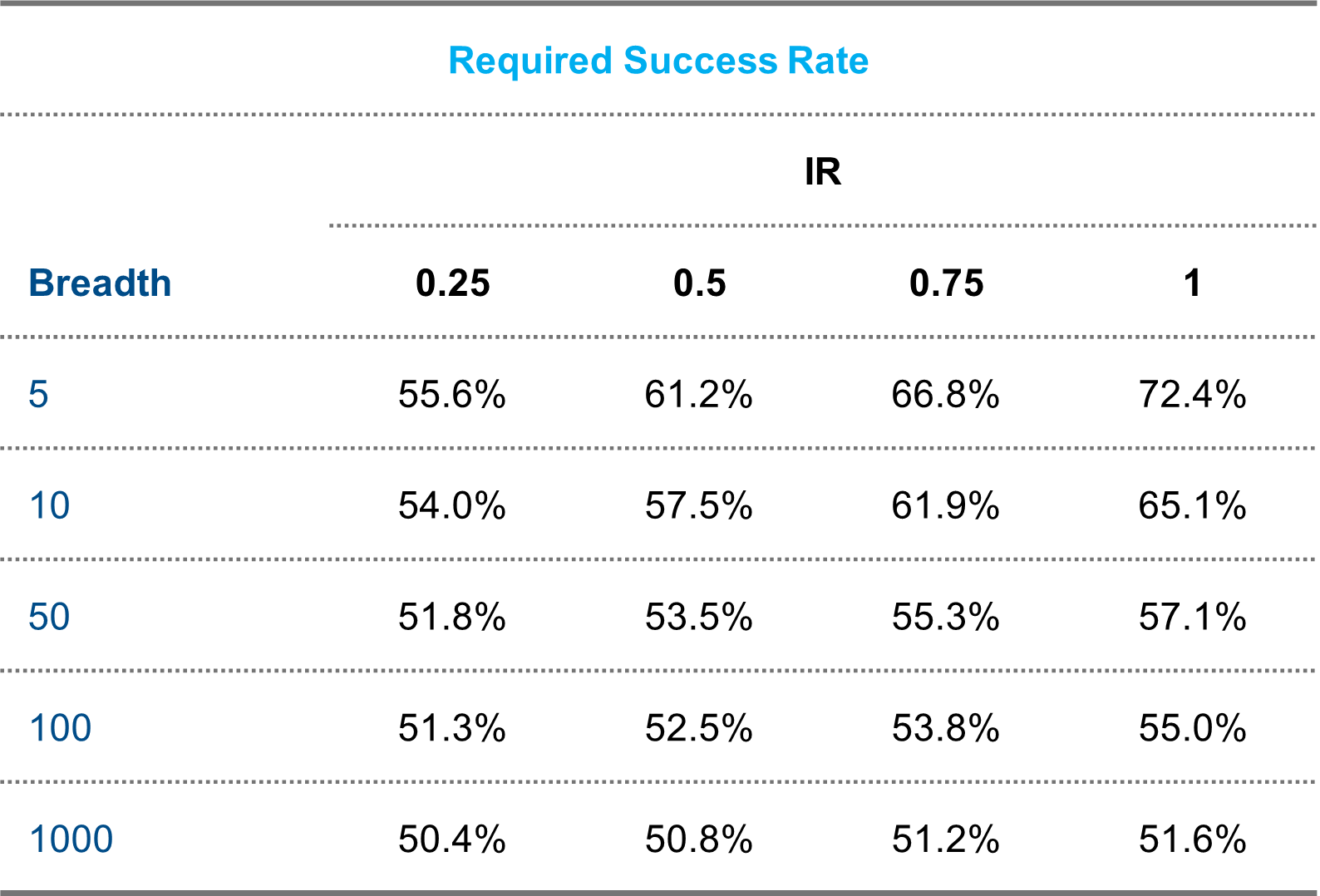

Tying this back to manager evaluation, Figure 1 highlights the breadth and success rate required to maintain a given information ratio.

Figure 1: Manager Breadth vs. Success Rate

A manager with a breadth of 10 requires a 65% success rate to support an information ratio of 1. Achieving this level of accuracy is difficult, especially in 10 uncorrelated ways. Expanding to 100 independent bets lowers the necessary win rate to 55%. While still challenging, hitting 55% with substantial breadth is more attainable for bottom-up strategies, which typically focus on individual securities where structuring skill is essential for isolating views and uncovering additional opportunities to expand the number of independent bets.

Conclusion: A Broader Definition of Investment Skill

Investment skill has been misdefined. Forecasting skill has played, and will continue to play, a role in portfolios. Yet strategies driven more by structuring skill translate to higher transfer coefficients, greater effective breadth, and more plausible success rates. In turn, these traits translate into robust alpha that is repeatable and frequent, and less likely to fall into the trap of beta masquerading as alpha. While this framework is useful for evaluating managers and distinguishing between forecasting- and structuring-driven strategies, it is most powerful when allocators use this approach to impact governance and portfolio design to deliver their own version of structuring skill at the total portfolio level.

The goal is better portfolio outcomes that rely less on crystal balls and more on disciplined implementation and hard work.

Frequently Asked Questions

Q: What is the difference between forecasting skill and structuring skill?

A: Forecasting skill generally involves predicting broad market or sector movements, while structuring skill encompasses the ability to design, source, and implement exposures efficiently and intelligently through engineering, market-making, operational, and access capabilities.

Q: Why is structuring skill more persistent than forecasting skill?

A: Structuring skill is often embedded in a firm rather than the individual, allowing for greater persistence, transferability across strategies, and less dependence on predicting markets based on an individual’s view. The broader the market forecast, the harder it can be for forecasting skill to persist.

Q: What is “beta in a trench coat”?

A: This refers to when an active manager injects beta (systematic market exposure) versus their benchmark. This can often look like alpha, but doesn’t reflect manager skill. An example would be a U.S. Aggregate fixed income manager that is systematically overweight credit.

Q: How does the Fundamental Law of Active Management relate to structuring skill?

A: Structuring skill improves the information ratio by increasing both the information and transfer coefficient. The various sub-skills have differing impacts on each of these components. In addition, structuring skill is repeatable, which increases breadth. For example, a manager that routinely provides liquidity to the market through market-making will have numerous, substantially uncorrelated, trading opportunities which will drive breadth higher.

[1] Assuming you have a way to reasonably measure the manager, like an investable benchmark.

[2] While allocators who utilize internal management can directly benefit from the structuring skill set, we are also referencing allocators that only use external management. With the right portfolio design, they amplify structuring skill, which then creates alpha.

[3] When allocators are made aware that the strategy has effective beta (e.g., being overweight corporate bonds against a broad market fixed income benchmark), it is acceptable so long as managers (a) fully disclose to the allocator and (b) don’t take credit for the alpha.

[4] The paper titled “Fundamental Law of Active Management” was introduced by Richard Grinold in 1989 and published in the Journal of Financial Management.

[5] IC = Information coefficient, TC = Transfer coefficient.